A dollar reset and a stock market bubble

Why the Fed's rate cut projections are rocking the markets

Investors were preparing for a stock market collapse not too long ago. Less than 90 days later, they now think we are in “bubble territory.” The market is rallying. And yet, the new highs are dropping in value – because the dollar is decaying.

I don’t mean to be the bringer of bad news, but there’s no point in beating around the bush. The dominant US dollar is not looking so good any more. It’s had its worst start to the year since 1973. Every day, more money is being created and debt is being accumulated. We’re headed for the biggest decline since 1986.

In the early 1970s, the US dollar was pegged to gold which was set at a fixed price of $35 an ounce. At the time, the minimum wage was $52 per week, nearly 1.5 ounces of gold. Now, gold is trading above $3,300 an ounce while the dollar has lost a huge chunk of its purchasing power. The US dollar is still the reserve currency of the world, but the same worker would need to make $4,884 per week to match the minimum wage. The currency is being devalued. Why, and where is this headed?

Let’s understand this in three steps:

What’s the Fed’s roadmap for the rest of the year

How this affects stock prices and your investments

What this means for the real estate market, and you as a buyer

We’re in for a wild ride, and preparing in advance will let you make the best moves when opportunities are at hand, and turn it into profits.

The Fed’s roadmap

Like I’ve been writing about in earlier issues, we’re caught in the middle of a tussle between two of the most powerful people in this economy: Jerome Powell and President Trump. Trump has one priority, and that’s to lower interest rates. He’s been throwing some choice words at Powell for resisting this plan (“Stupid”, “Numbskull”, “Dumb”, “Fool”, “Mule”, “Major Loser”, etc.) while Powell has stuck to his plan of holding rates steady to not trigger another inflation.

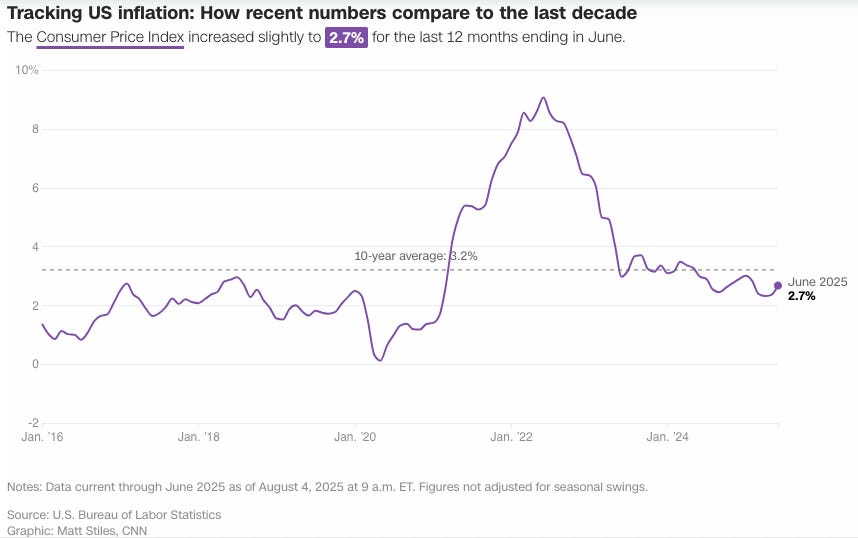

So far, his plan seems to be working. Despite tariffs, consumer prices have just risen by 2.4% last month, lesser than what economists expected, and only slightly higher than the 2.3% rate in April. This was the lowest inflation in the US economy since February 2021.

Jerome Powell is approaching this cautiously though – while he admitted that only a few items are growing in price as a result of tariffs, he thinks that it’s because stores are still working through the inventory that they had stocked up on before tariffs kicked into effect. So prices will go up eventually.

No CEO wants to be the first out of the gate. If they are the first to raise prices, they risk offending customers, so they’d rather eat their margins and sit tight for a few months. As a result of this improvement, Trump is no longer pushing to fire Powell, but this doesn’t take away from the fact that the dollar is falling.

Why is the dollar falling?

We have three main reasons:

Money printing is flooding the market with money. Our national debt surpassed $37 trillion. Even at the point of no return, our only option is to continue printing more.

Political instability is scaring away other countries. 70% of investors no longer want to invest because of geopolitical risk, up from 31% last year.

Which means, the money is going elsewhere. Since the US dropped the gold standard, the dollar has lost 85% of its purchasing power while gold prices have increased 85x.

This is leading to the emergence of some interesting alternatives, with one of them being Bitcoin. Billionaire Tim Draper argued that Bitcoin is becoming a global safe haven for people escaping flawed systems. According to him, software-based money is better technology than government-issued currency, and the tipping point could be as early as 2035.

I can’t say that he’s totally wrong on this – 65% of investors say they plan to buy or invest in digital assets in the future, compared to the 16% who currently own it. Half of all advisors also plan to recommend crypto investments to their clients within the next 12 months. With inflation averaging 2.65%, the dollar has lost 26% of its value. Home prices are up 100%, gold has risen 181%, the S&P500 increased more than 200%. And Bitcoin is up more than 35,000% ! Of course, critics argue that past performance doesn’t guarantee future returns, and Bitcoin is very volatile too. On top of this, the dollar is backed by the full faith and force of the US government, while there are no such external guarantees for Bitcoin.

Falling interest rates affect more than just the dollar. Even if you invest in stocks and real estate, you need to be prepared for what comes next so that you can turn a profit:

The stock market

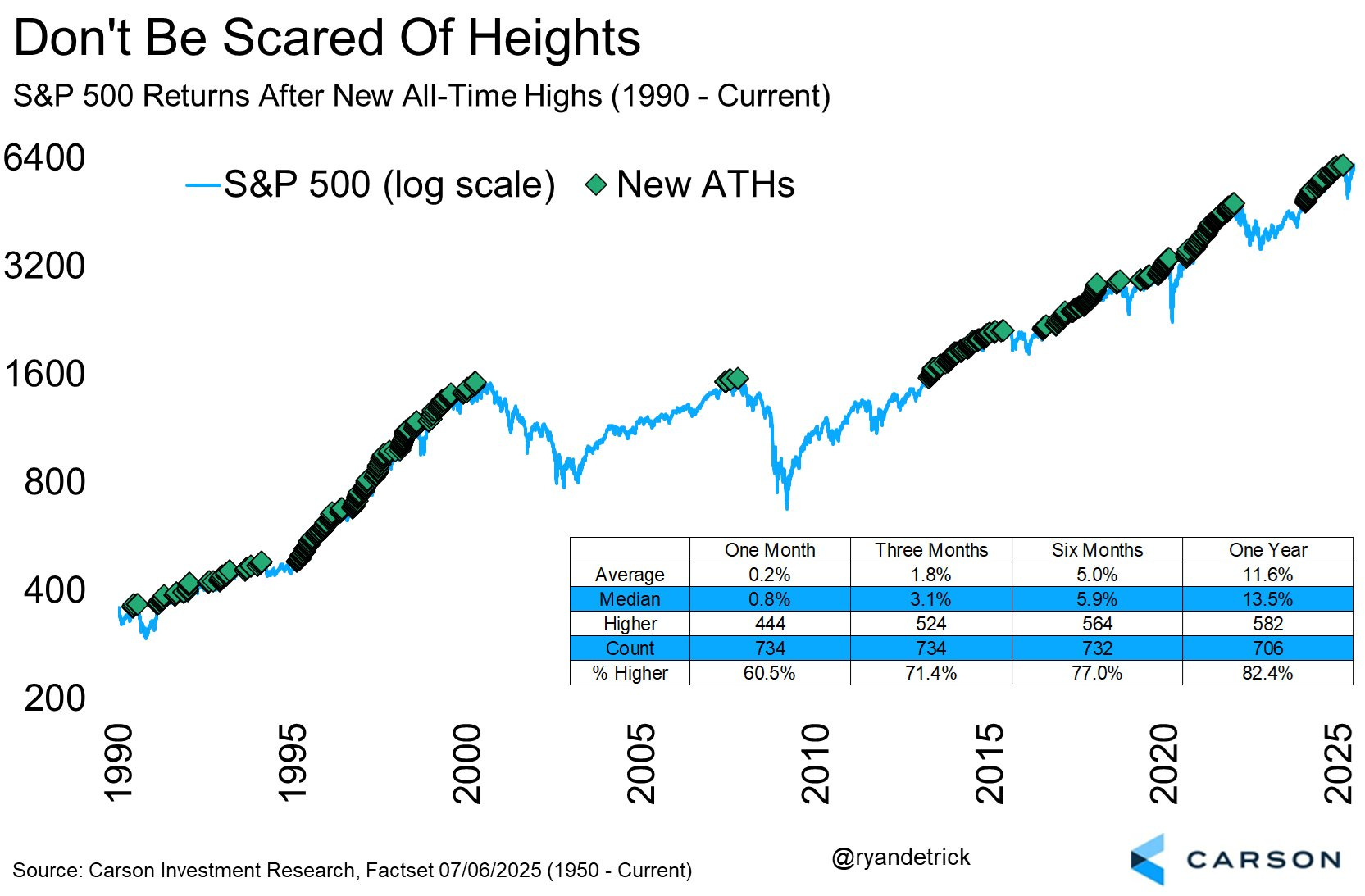

At first glance, stocks have done extremely well this year. The S&P500 is already up over 7% and we’ve consistently hit brand new all-time highs. So when people believe we’re back in a bubble, what are they worried about?

Well, for one, the market is consistently moving up every single day. The NASDAQ has gone 60 trading days without closing below its 20-day moving average. This is the second-longest streak in its history – the first was in 1999, and it ended in the Dot-Com Crash. The S&P 500 is also trading right now at 26x forward evenings which is much higher than the historic average of 18. So with meme stocks trending, this might be something to worry about.

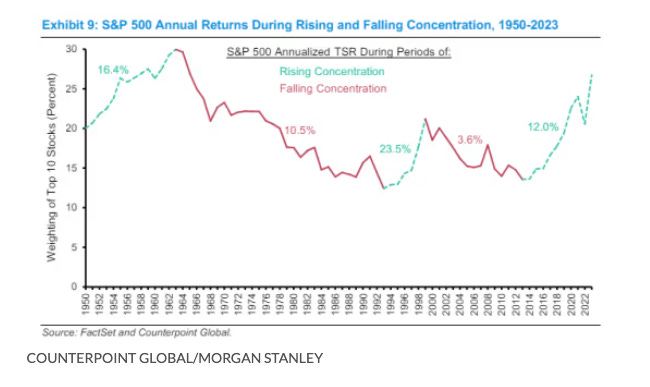

But on the flip side, even though the S&P500 is growing especially concentrated, keep in mind that Cisco traded at 200 times earnings in 1999 while Nvidia trades at “only 40x” earnings today – suggesting that things are not as bad as they were once. There’s even the possibility that concentration could be good – according to a study, it was found that because the leading companies generate the most revenue, higher concentration leads to higher returns on average. If that’s the case, then this is a bullish signal.

In terms of what will actually happen over the next 12 months, it’s anyone’s guess. Blackrock noted there’s several trillion dollars worth of cash sitting on the sidelines, invested in short term treasuries, waiting to be deployed. Morgan Stanley reset their price target for the S&P500 to 7,000 in 2026. Goldman Sachs predicts 6,600, and several others think it’ll surpass 7,000.

Historical data shows that all-time highs aren’t something to be feared because highs go on to create new all-time highs in the future.

The housing market

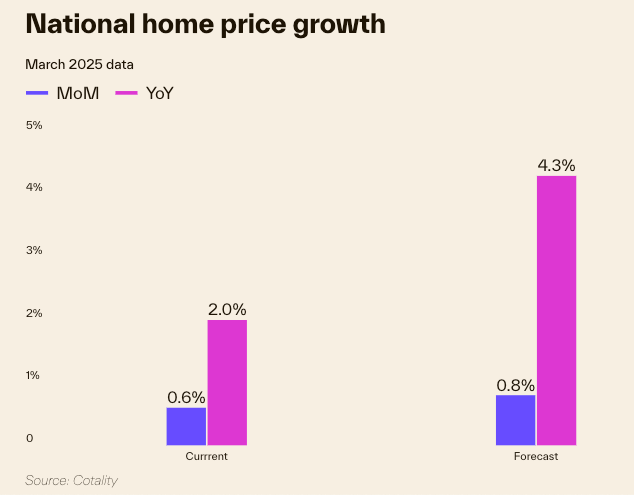

While stocks have some uneasiness around them, the housing market has some good news for buyers: Despite mortgages at the highest we’ve seen in over two decades, home prices have started to flatline throughout 2025. National home prices are up just 1-2% compared to last year, according to CoreLogic – considering inflation, that’s actually a decline.

One thing to keep in mind is that not every market is reacting the same way:

Cities like Cleveland, Louisville, and Hartford are seeing year-over-year price gains of about 4% due to steady demand and being relatively affordable.

However, areas like Austin, Tampa, Miami, and Dallas have fallen anywhere from 3-6% due to piling inventory after pandemic booms. Cape Coral was one of the hottest markets just two years ago, but it’s now priced below the national median.

Sales volume is beginning to slow down across the nation. Redfin reported that we’re on track for 4.1 million home sales this year, one of the slowest in a decade. At the same time inventory is also climbing. Zillow noted a 17% increase from a year ago. Those homes have also been on the market for longer, taking an average of 19 days to go pending, versus just 11 during the 2023 peak.

What does this mean? We’re actually beginning to “somewhat normalize,” with 22 of the top 50 metros now being considered “neutral” – which means neither buyers nor sellers have the upper hand. Where does it go from here? Zillow predicts that throughout 2026, average home values will fall by 2% through the next 6 months, giving back a small portion of last year’s increase. CoreLogic takes the opposite stance – they say that home values will continue to climb from excess demand, with a 4% increase over the next 12 months. In the big picture, experts think that once mortgage rates dip into the 5% range, we could see a dramatic pickup in activity. Until that happens, be prepared for sluggish sales, higher inventory, and plenty of price reductions. When it comes to rents though, the picture is completely different.

Single family rents are up 3% from a year ago, nationwide.

New York and Chicago are leading the way with 6% gains (looks like a lot of would-be buyers are stuck renting until rates come down).

Miami and Dallas are essentially flat from a surplus of inventory.

As someone who’s been professionally involved in real estate since 2008, here’s my take: A lot of sellers are testing the market with unrealistic prices and holding out for a bidding war that just isn’t happening. You also have a lot of sellers who have locked in a 2.8% mortgage – they’ve placed their home on the market at a price where if it sells, great, but if not, they don’t mind holding.

If you’re in the market to purchase a home, this is the first time in years when you can negotiate without being up against a dozen other buyers with competitive prices. Sellers are more open to taking a hit and price cuts are happening throughout nearly a quarter of all listings. Nearly 1 in 7 are falling out of escrow, and sellers might be more willing to make a deal. So take advantage of that, and be patient to find a deal that suits you before buying.

Rate cut prediction

The Federal Reserve has once again decided to postpone rate cuts and hold firm for at least the next two months, until their September meeting. They’re still concerned about tariffs, rising costs, and a strong labor market all keeping prices high. There’s no reason for them to lower rates if it’s not absolutely required to keep the economy afloat. But will a rate cut happen in September? It might.

The market is beginning to price in the chance of a 25 basis point reduction when they next meet on September 17th. But take that with a grain of salt – the market has priced in these possibilities in the past, and they didn’t exactly come true. In case the Fed does decide to cut, they’ll probably signal their intentions in advance of their meeting, probably a week before the meeting. This way, the market has time to digest the information and price it in.

So what’s the takeaway from all this? Here’s what I feel. I’m a little concerned with all the Memestocks and Altcoins pumping out of nowhere. It usually signals that many people are getting a little ahead of themselves by throwing more money they can afford into things they are hopeful about without doing the research. At the same time, the rest of the year is sort of looking optimistic for me, with more trade deals and those elusive rate cuts in the picture.

But next year, we’d see a completely different scene altogether, with Powell’s term ending in May 2026. Trump will probably appoint someone who’s likely to do whatever he wants, which is most likely: a lot more free money. Is that already priced in? That’s anyone’s guess. But my thoughts are still the same about my personal investing strategy – I dollar cost average into the overall market without timing it or analyzing the price, and the studies show that this produces the highest returns.

I don’t believe in timing the market. Guessing the market’s movements is like calling heads or tails on a coin flip. Sometimes you might get it right, but in the long run it averages out, and the people who chase the markets end up losing more than they win. On the other hand, if you kept buying through the dips in March and April, congratulations!

I’ll check in with you again next week. If you read this far, let me know how you found the update in the comments – I read every single one. Also, like and share with at least one friend who’ll find this useful. It’s a small thing but it really helps. Thanks!

I have seen some very bearish sentiment in the Market, AI is useful but heavily industry dependent. You can Pump out way more designs and brain storm ideas easier like with TraxNYC. But if you are a hair salon other than with advertisements, AI is not as useful.

With the lag luster launch of GPT 5.0, we have seen some hiring freezes from Meta for more AI talent.

What is your opinion on Government Bonds Gram? Do they have an place in your portfolio or just broad market ETF funds till we die lol?

Hope all is Well!

-Vic

I am a college student and this is my first time reading one of your news letters. I found it easy to follow and understand but also being very informative!