Black Swan

A developing risk in Forex markets

What’s up Graham, it’s guys here :-) If you want to join 27,665+ smart investors and never miss an update on the market, hit the subscribe button below. It only takes a second and is completely free.

In 1696, William de Vlamigh, a Dutch sea captain set out on a rescue mission to search for the survivors of a ship that had gone missing for nearly two years. They sailed through the coast of Scotland, South Africa, and Indonesia and eventually reached modern-day Perth in Australia. On January 10, 1697, they sailed up a river and in a shallow estuary saw what was considered to be an unimaginable sight for many Europeans back then: A black swan.

You see, for nearly 1500 years, the prevailing belief in Europe had been that all swans were white and there was no such thing as a black swan. In fact, a ‘black swan’ was often used as a metaphor in 16th-century London for something that could not exist. The finding of a black swan changed this metaphor and it became a symbol of an unknown or unexpected event that changes everything completely. A rather morbid example would be life from the perspective of a Thanksgiving turkey, which has been well-fed and pampered till Thanksgiving day and assumes that life is great - only for everything to change in an instant.

Nassim Nicholas Taleb developed the black swan theory in finance to describe the role of unexpected, large-scale events in shaping the economic landscape. Essentially, a black swan is an outlier, low-probability event that makes predicting and planning for it extremely difficult. The recurrence and consequentiality of these events have spawned an entire financial industry, known as tail-risk hedging. According to Taleb, examples of black swan events are the rise of the personal computer, the 9/11 attacks, and the 2008 housing crisis.

There was a startling announcement by the Bank of International Settlements (BIS) recently and I think we should view it within the framework of the Black Swan theory. The BIS is essentially the central bank to central banks and they revealed that pension funds and other non-bank financial firms have more than $80 trillion in hidden, off-balance foreign exchange swaps. This could be a blind spot that risks leaving policy-makers in the fog. At this point, we should remember that trying to predict a black swan event is in itself paradoxical: by definition, a black swan event is unpredictable. Nevertheless, due to the sheer scale of this story which forced the BIS to make this statement, it deserves a closer look.

So this week, let’s take a look at why currency swaps are necessary, what is the root cause behind the recent issue and whether this has the potential to become a black swan event that we should be mindful of.

Currency Swaps

“The central idea in The Black Swan is that: rare events cannot be estimated from empirical observation since they are rare.” - Nassim Nicholas Taleb

All of this begins with what are known as foreign exchange swaps or currency swaps. This is something that companies engage in when they want to conduct business in different parts of the world and need to acquire capital for that. For example, American companies will need access to Euros to conduct business in Europe, and EU companies will need access to dollars for projects in the USA.

Now, the straightforward option would be to borrow this from a bank in the country you are doing business in: if you are doing business in the United Kingdom, say, then you would borrow from a British bank. Unfortunately, banks often demand higher interest rates if the borrower is from a different country. Due to this, creative financial organizations have come up with foreign exchange swaps. Essentially, the US company that wants to do business in the EU borrows from US banks (at favorable rates) and swaps that for Euros with a foreign company that needs to conduct business in the United States, with a promise that both companies will return the money in the receiver’s currency.

{kind=link}

Sounds good right? So what's the issue?

Well, the first reason which prompted the BIS to make this statement is that currency swaps are not required to be reported in company balance sheets, and they recently estimated this amount to be nearly $80 Trillion. To put that in perspective, that is twice the size of the US stock market, three times larger than the national debt, and six times larger than the mortgage market.

In a perfect world, currency swaps would be a non-issue. Each party pays back the original amount and everyone is able to save some money on interest rates. However, anyone who has been following financial news knows that we are far from an ideal scenario right now.

Structural Risk

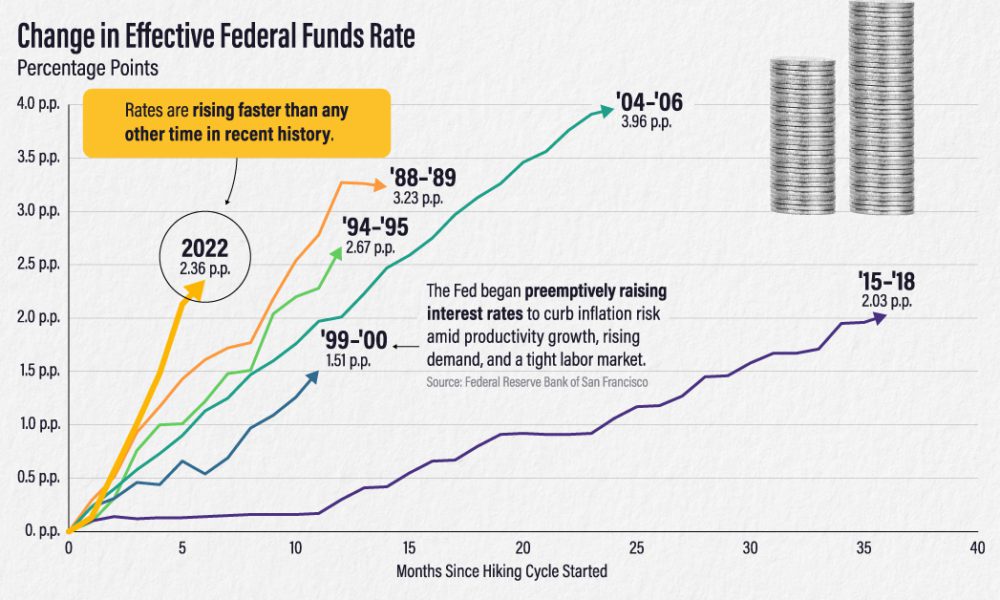

The present concerns are primarily caused by the dominance of the US Dollar in the currency markets. With the Fed raising interest rates and nearly every other currency falling compared to the dollar, other countries see the USD as a safe haven that can hedge against their own currency and are loading up on it. Quite often, short-term swaps are used by companies to purchase long-term assets. As these swaps come due, in a landscape where the dollar is more expensive than ever, there might not be enough dollars to repay the debt.

The BIS report states that “$80 trillion-plus in outstanding obligations to pay US dollars in FX swaps/forwards and currency swaps, mostly very short-term, exceeds the stocks of dollar Treasury bills, repo, and commercial paper combined.” This could force countries/organizations to print more of their currency as the demand for the Dollar increases and it becomes more expensive, which causes higher inflation, or worse, force them to sell their assets to raise capital.

Reuters recently reported that $2.2 Trillion worth of currency trades are at risk due to issues between lenders and if these borrowers fail, there could be a dollar shortage. An even bigger issue is that because these swaps are not reported in company balance sheets, there is an estimated $30 Trillion dollars of swaps that were not accounted for until recently. Now, for most of us back home, this does not present an immediate risk, since swaps are primarily happening overseas. However, the overall issue is that a rising dollar could hamper worldwide growth and create a liquidity crisis similar to what happened in 2000 and 2008.

Finally, there are also international factors such as a developing oil crisis and concerns about the Chinese manufacturing sector that could compound the issues caused by these long-tail events.

Just recently, the international institute of Finance went on record to say that worldwide growth is expected to be weaker than the global financial crisis of 2009 and points to a critical issue in this: energy. Just recently, in an effort to counter Russia’s war efforts, sanctions have been imposed capping Russian Oil at a maximum of $60 Dollars a barrel. It remains to be seen how this would affect the already strained energy markets in Europe and whether it will affect production in a negative manner. Further, China is also facing a collapse in its manufacturing sector as orders have declined by 40% due to lockdowns in effect.

Action Plan

So, given this turbulent scenario, what would be your best bet as an investor? With interest rates rising at the fastest pace in history, government bonds have had the highest performance across asset classes, averaging as much as 6.6% throughout the last 4 recessions. Even though this pales in comparison to the average return from stocks, if you have cash sitting on the sidelines, bonds could provide a cushion against volatility as they typically go up by 5% in the first half of a recession. Given that the international institute of Finance went on record to say that worldwide growth is expected to be weak and equities typically decline in this environment, it might be worth your time to look at some bond offerings.

{kind=link}

At the end of the day, the currency swap issue could end up being a black swan event: i.e it’s highly unlikely but deeply consequential if it happens. In my opinion, it is unlikely that this will evolve into a larger crisis, unless we are hit with an economic disaster such as the 2008 or 2020 crisis, in which case the swaps would be the least of our concerns. With inflation data also looking promising, we can expect the Fed to be reasonable with their rate hikes in the future.

So, stay safe, stay invested and I will see you guys next week - Graham Stephan.

A lot of effort and research went into making this article, so if you found it insightful, please help me out by clicking the like button and sharing this article.

Great read! JDimon has warned about this and put the total of unsettled global swaps of all instruments at about triple the currency derivatives. What could go wrong?? And why does GAAP allow this off-balance sheet? Where can investors find this data for any specific company! Is there an SEC filing requirement?

I really appreciate the information you provide through these newsletters. As an active investor you often shine light on some aspect of the financial industry or the state of the world economies that isn't typically covered by other publications. Thank you and I hope you have a fantastic Christmas and New Year!