Don't buy a home in 2022

The anatomy of a bad idea

Buying a house is considered one of the best financial decisions for any household decision to make. It’s what most families save up for, and it’s a major step towards safety, security, and wealth-building. Yet there’s another side to the coin - Buying a house is a long-term move and it could tie up your finances for up to 15 years or more. Locking in a house at the wrong time is something that could as easily set back your wealth-building as it could help it!

And now is the worst possible time. Seriously, I’m not going to be mincing my words or taking a diplomatic stance here. 75% of home buyers regretted their decision to buy in a rush. Home affordability is near an all-time low, and even though sellers are reducing their asking prices, you should not be buying a home in 2022. I’ll give you a five-point framework to explain why and if you have a home deal lined up anyway, make sure that you tick all the boxes in this checklist! Let’s get started.

1. Don’t rush

Mortgage rates are heading up, and sellers are bringing down their asking prices. If you lock in cheap rates before they go up and get a home for a lower price, you should jump at the chance, right? Not really. Unlike paying rent on a property and letting your landlord take care of everything else to do with the house, becoming a home-owner comes with a lot of extra expenses and responsibilities. Here are some:

The kicker here is that all of these could have been prevented with some extra research and taking some time before locking in a deal.

Another tip is to engage the experts. An inspection beforehand could save you a lot on maintenance down the line. Hiring a mortgage broker might cost you some money upfront, but considering that the mortgage is the largest chunk of your expenses, getting a good deal is very important. Never take the first deal that you are offered!

2. What is the opportunity cost?

Instead of “wasting money on rent”, it’s always a far better idea to buy a home that appreciates in value, right? Not always.

Buying a home is an investment that generally pays off in 5 to 7 years, but that also means you will not be able to invest the funds you are tying up in any other option. Unlike stocks or bonds, the liquidity in the real estate market is an issue - But that’s not the only problem. The additional costs that go into a house also increase your expenses, like:

Transaction costs - How much will you have to shell out in commissions, escrow charges, transfer taxes, etc.?

What will you be spending every month on property insurance, maintenance, repairs, etc?

A house in itself is rarely a bad investment, but these are expenses for which you will not be getting a return. You should consider these factors to understand how much capital you are truly tying up in your venture, money that you could have invested somewhere else instead, for a better return. This brings us to our next topic…

3. Make a realistic budget

Going a little deeper into the expenses part, let’s take a look at how much owning a house will actually cost you. The most obvious expense is your mortgage. This is pretty straightforward to calculate on any mortgage calculator that lets you plug in your home price and mortgage rates, to get a quick estimate of how much your monthly payments are going to be. You can take this a step further, and see how much of your payment is going towards interest and home equity every month.

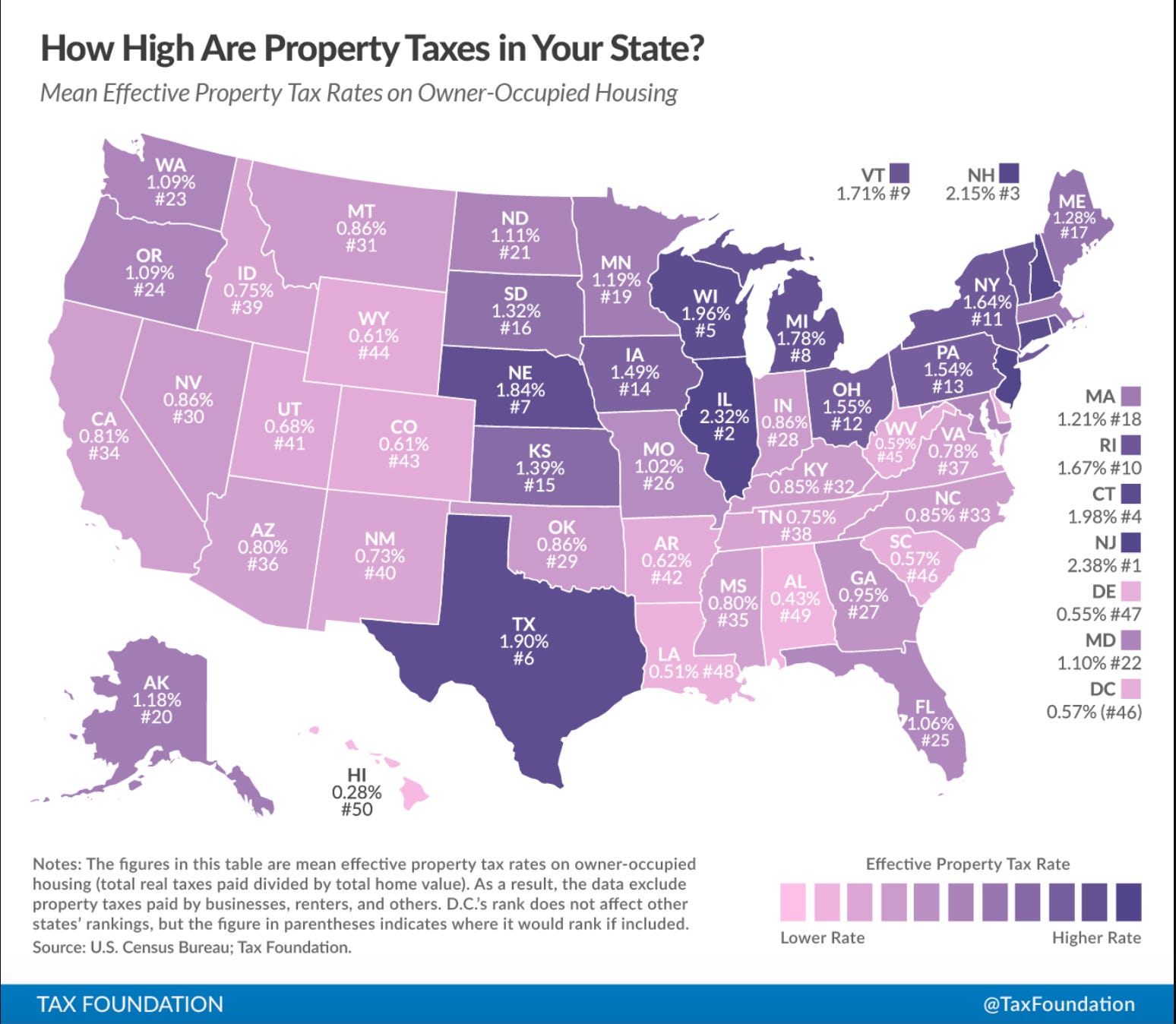

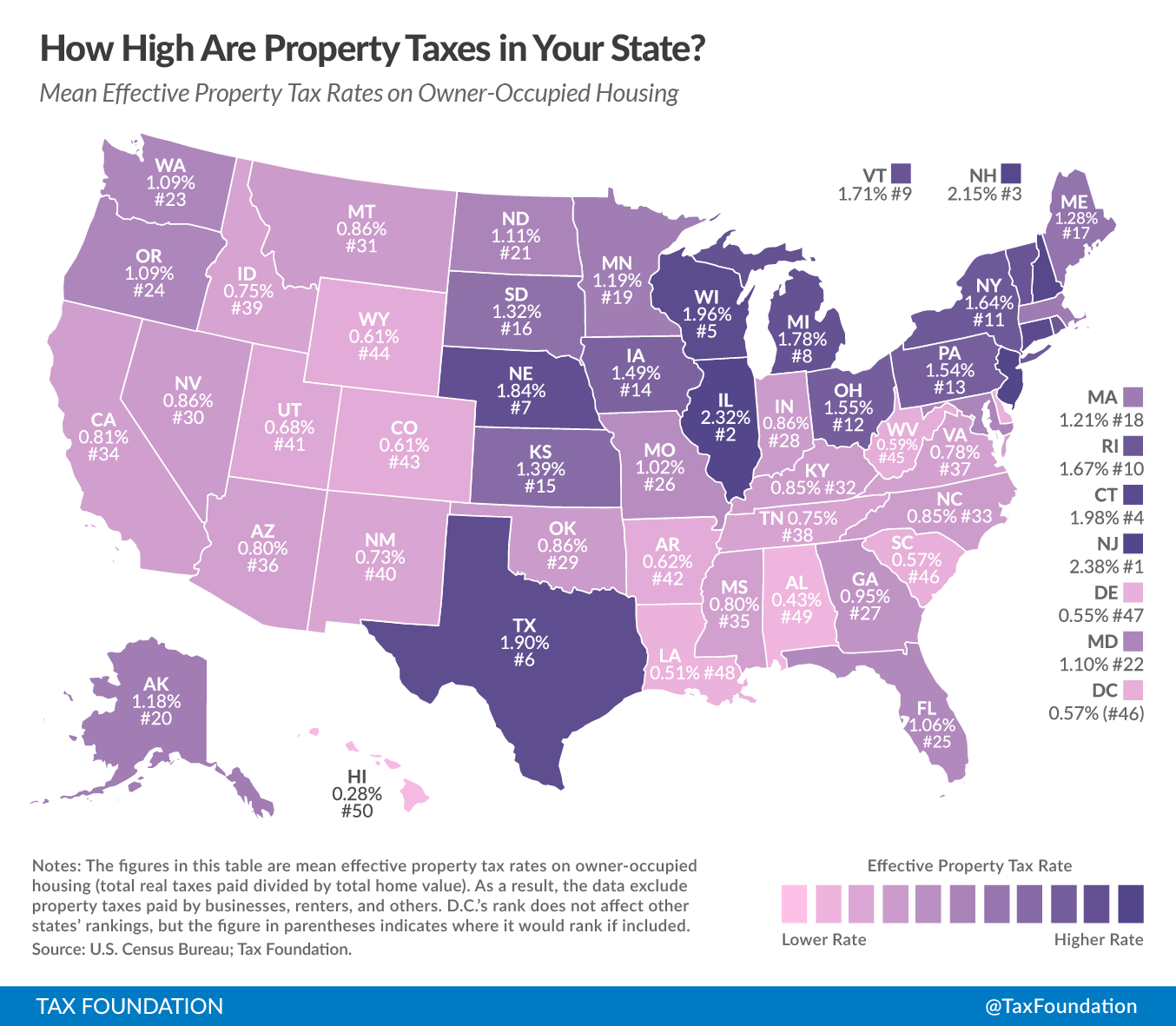

Next comes property tax. This is one of the most expensive overheads when it comes to owning a house, and with even a 1% tax on a $400,000 house, you end up paying $4,000 a year, or an additional $334 a month. This is money you can’t invest, and property taxes only go up with time.

{kind=link}

Insurance is the next expense, and it also depends on the area of residence. Areas that are more prone to fire, floods, earthquakes, etc. have a higher monthly payment, and you could end up paying $60-$200 for this.

In addition to this, you have regular maintenance and niggling home repairs - Murphy’s law always kicks in as soon as you buy a home, and that faucet that was working fine yesterday suddenly starts dripping, and before you know it, you’re driving to Home Depot when gas is $5 a gallon just to make sure your home isn’t falling apart.

All of these can easily take up your mortgage of $1,500 to monthly payments of $2,500 - So make sure that you’re budgeting for these. But all this is just the cost after you make the transaction - What about the transaction cost itself? Which brings us to…

4. Can you flip it?

No, you can’t. The last two years have been crazy, with supply chain blockages and labor shortages, and lack of housing inventory pumping up home prices to extraordinary levels, meaning that anyone who had bought a home before the COVID crisis would have made huge profits by flipping their houses two years later. But this rapid increase in rates is not sustainable, and we’re not even talking about the real cost of buying a house which is in the transaction itself.

The mindset of a home-buyer is usually something like “I’ll buy it, live in it for a few years, and hey, I can always sell it a few years later!” But it’s not so easy. When you buy a house, you would end up paying anywhere from 5-7% of the home’s worth in just transaction fees - home inspections, escrow charges, loan origination charges, appraisal fees, and a bunch of other miscellaneous charges. You never pay for the home alone (Home alone, get it? Never mind).

Selling a home is even more expensive, and from buying to selling, a $400,000 home could accumulate an overhead of $47,400 over 3 years - that’s 11.75% extra! You would need to sell it at a higher rate than that to just break even. Counting on the current rate of home appreciation to continue is dangerous, and it’s a bad idea to buy a home unless you plan to live in it for at least 5 to 7 years and let the value appreciate.

5. Have an emergency fund

The last point is just an emphasis on preparing for the unknown. Just like you should have an emergency fund for yourself and your family, you should have one for your home too. After all, not many foresaw the supply bottlenecks and labor shortage over the last two years - but faucets break all the time, lights stop working, and when you get the repair bill, don’t let it give you a heart attack. Plan ahead and save enough so that it doesn’t become a financial burden.

Conclusion - with a twist

Alright, I said I am taking a hard stance. Buying a home that you live in and get to call your own is a great idea, but it just isn’t a good time now, with more than two dozen cities being “overvalued”. But there’s a catch here. I’m talking only about homes, that you buy because you want to live in them.

The truth is, this situation has now opened up a lot of opportunities to negotiate and cut down prices, and if your intention is to buy a house, renovate it, and then flip it, or rent it out, then that’s a totally different scenario - because in that case, you won’t be paying mortgages for years on end. You could get great deals if you know where to look - and if you have experts to guide you in the process.

Consider the entire picture and determine whether it makes sense for you to go ahead with your plan given the times we are in.

See you next week with another deep dive!

If you enjoyed this piece, smash that like button and share it! Thank you.

Thank you, Graham, but this isn't good for my blood pressure.

Thank you Graham for the valuable content and advise. I live in the Charlotte, NC area and the housing market over here has been wild for a while 😆. In the past few months I was motivated by buy but I refused to pay extra for a house that I knew did not have the value and was obviously overpriced. At one point I was putting at risk $25K just to get through an offer that I though was reasonable. Thankfully my offer was not accepted, so I was relieved in the end because I was not happy about the whole process and extreme competition. People around here were making offers of $50K above the asking price, or buying without viewing the house in person..... good luck to them. Ultimately, I've chosen to invest outside of the U.S. (my home country). I took my down payment and purchased a rental vacation condo in front of the beach for a fraction of what I would have paid in Charlotte. My investment is already producing income and I am happy paying rent in Charlotte until the time is right to explore buying a house again. I watch your weekly YouTube videos for the valuable content. Thank you!