The silent plan to erase the national debt

You're paying the price

The $39 trillion national debt is a ticking time-bomb waiting to explode.

It’s no secret. This has been on everyone’s radar for a very long time. But the Federal Reserve’s plan to quietly make the national debt disappear is something most people don’t know about.

This isn’t a conspiracy theory. The Fed has literally told people what they plan to do. It’s usually put into such dull language that most people don’t understand what’s happening right under their noses. Back in the 1940s, the Fed used the exact same tactics, and it worked. They didn’t erase the debt. They just transferred it.

How does this new plan work? Who wins and who gets left behind when the Fed pulls the plug this time?

Today, let’s dive into exactly what you need to be prepared for so that your hard-earned wealth doesn’t get eroded by something entirely outside your control. But before you forget, hit subscribe and join 40,000 investors so that these weekly emails on how to keep your wealth safe land right in your inbox – for free:

How bad is the debt situation?

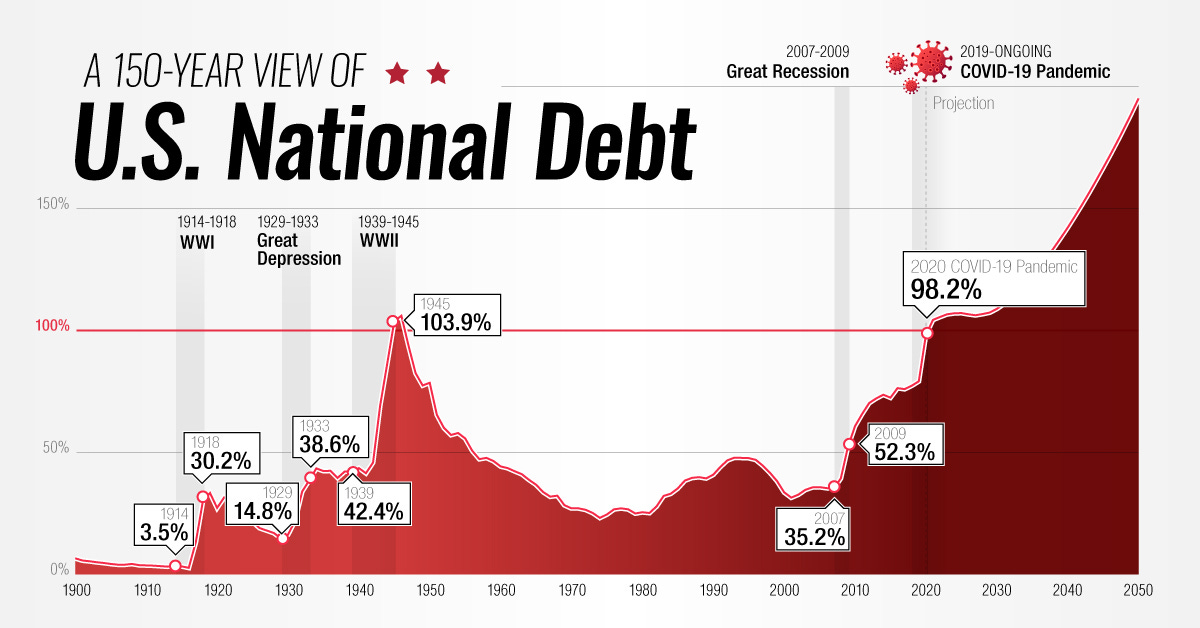

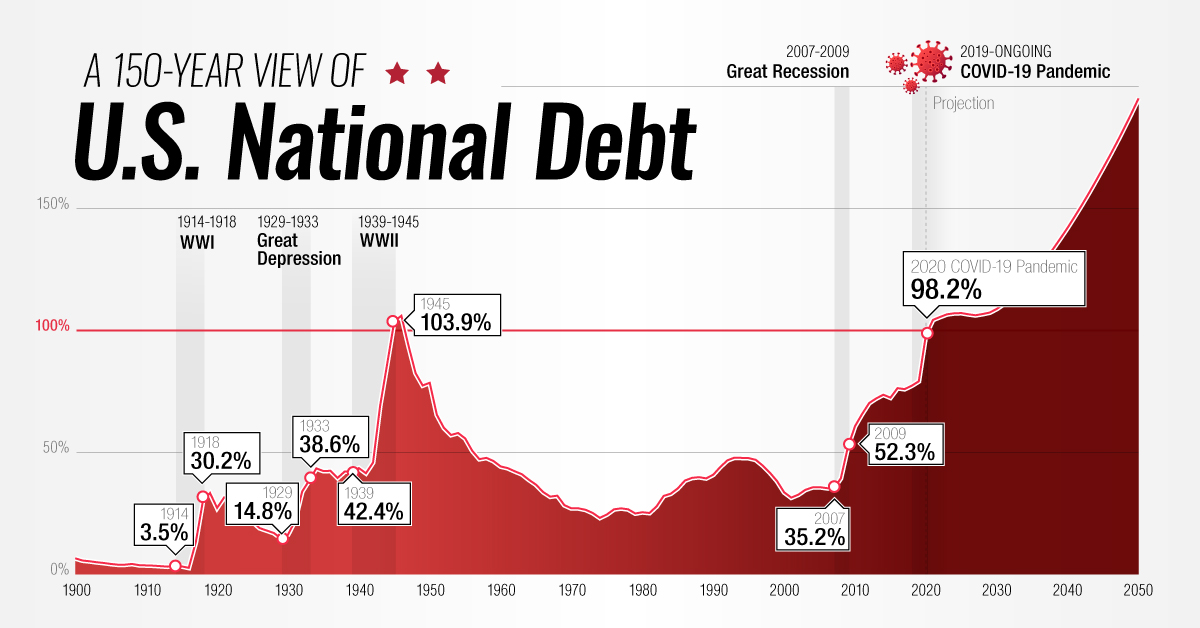

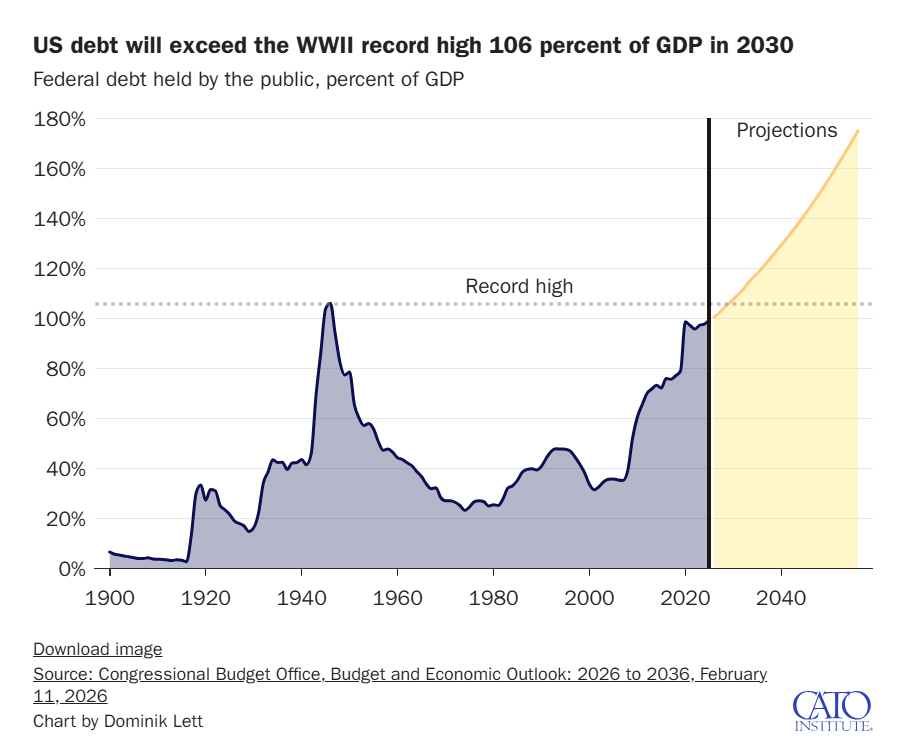

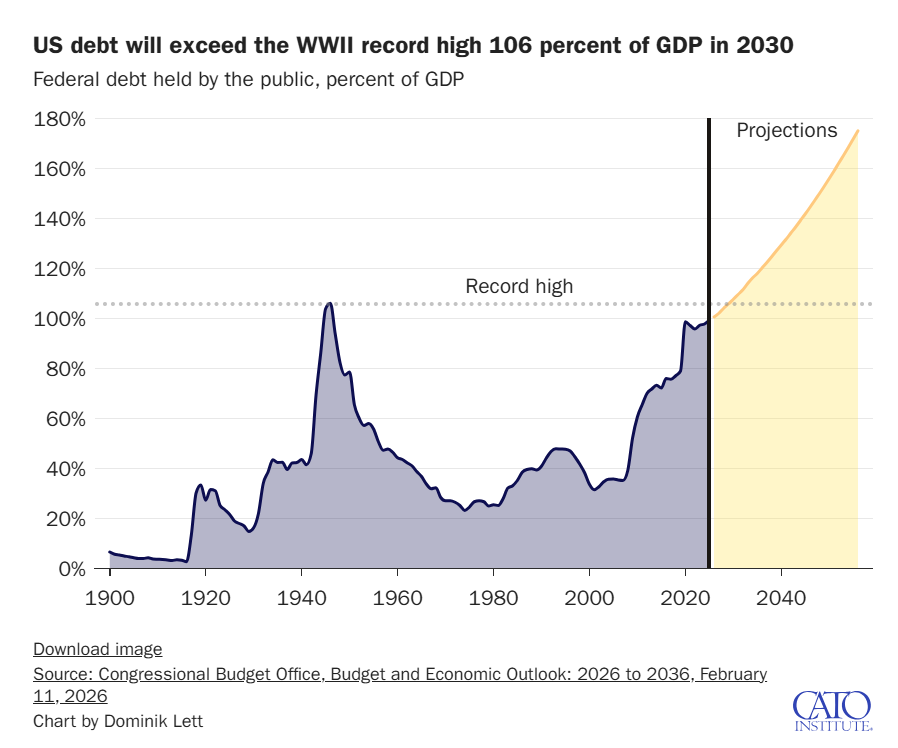

The US National Debt is in really bad shape. The last time we were doing this badly was during World War II and our survival was on the line:

{kind=link}

Let’s look at the numbers:

The US currently owes nearly $40 trillion.

It’s on pace to reach $50 trillion by 2030.

Every single day, the debt increases by $6 billion.

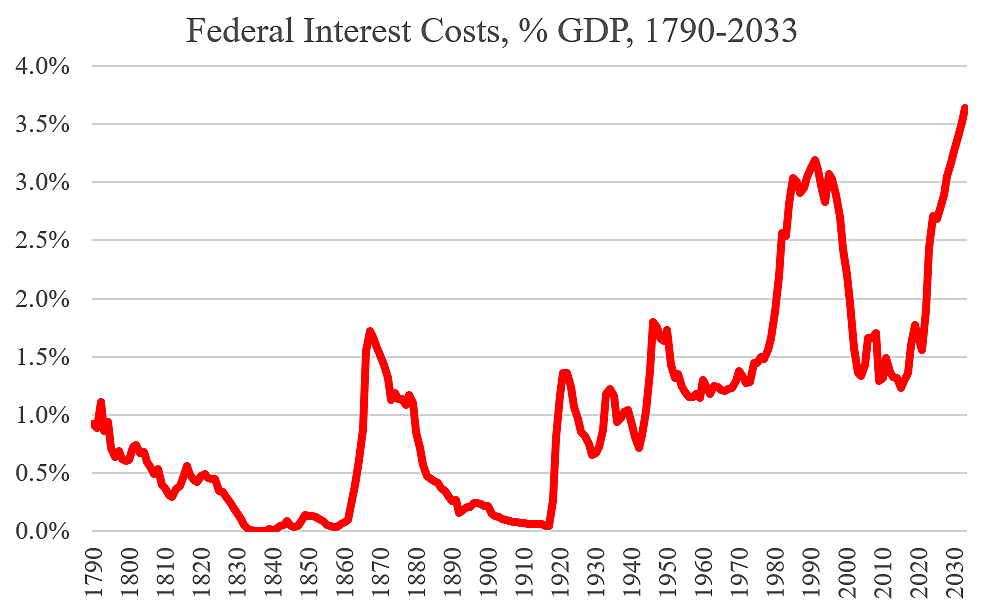

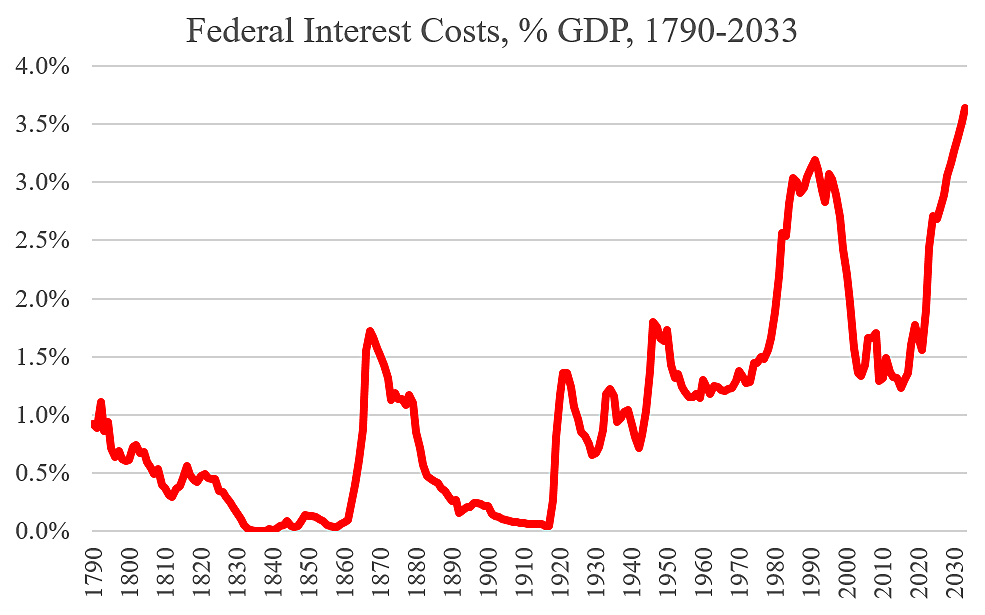

However, the debt itself isn’t actually the biggest problem. It’s the interest we pay. As long as interest rates were low, the cost of carrying the debt was manageable. With inflation kicking in and rates going up to 5%, the interest on trillions of dollars is causing a debt spiral.

{kind=link}

Here’s how it works: The more we borrow, the higher the interest payments. This leads to a bigger deficit that forces us to borrow more, leading to higher interest payments the next year. It’s a constant game of passing the hot potato. By 2036, interest costs will reach $2.1 trillion – a number so large that fixing it needs cuts equal to the entire defense budget to stop it from getting worse.

For the first time in US history, we are spending more on interest than on on our entire military, every single year. To combat this, Trump recently called for the Fed to lower rates immediately. Lowering rates might allow us to refinance our debt, saving us a lot of money, but it hasn’t happened so far because Jerome Powell’s first priority was to prevent runaway inflation. The new Fed Chair Kevin Warsh could take an entirely different approach.

But while interest rates can slowly eat away your hard-earned wealth, there are things that could change your life in seconds: Like leaving your information up on the Internet where anybody can find it.

Data brokers legally collect and sell your personal information – including your name, home address, and phone number – to anyone with a credit card. This exposure isn’t just a nuisance. It can lead to risks like identity theft, phishing, and doxing.

That’s why I trust DeleteMe.

DeleteMe is a hands-free subscription service that removes your personal information from hundreds of data broker websites. They use their own technology and real privacy experts to continuously monitor and remove your data all year long, never outsourcing to third parties. After signing up, you receive a detailed, transparent privacy report showing exactly what information they found, where it was, and what they removed.

Signing up to DeleteMe is the simplest way to help protect yourself – and your business – from scams and identity theft. Instead of scrolling away, just take a second to click here:

You get an additional 20% off when you use the code GRAHAM.

Now let’s understand what Kevin Warsh plans to do.

The three options

When a government has a debt problem this large, there are only three ways out.

1. Austerity:

This is the “responsible adult” solution. You raise taxes, slash spending, run surpluses, and pay the debt down over time. On paper, it works. A Cato Institute report found that the US would need to implement spending cuts or tax increases of about $827 billion a year to make a difference. This sounds sensible, but it’s politically impossible. Raising taxes while cutting Social Security, Medicare, and defense in the same bill is the fastest way to end a political career.

2. Default:

The US government could just say, “Hey, sorry guys. We’re bankrupt and we can’t really pay back what we borrowed.” Though this sounds insane, 14 countries have defaulted on their sovereign debt in some form since 2000 – including Argentina, Greece, Sri Lanka, and Lebanon. However, it’s different for us because the dollar is the world reserve currency. Everything is traded in US dollars and we are the safe haven. A US default would be such a disaster that it would trigger a global depression sending us into the dark ages. So, it’s definitely not happening.

3. The magical third option:

Shrink the debt with inflation. This is how governments quietly reduce debt without admitting they defaulted. All they do is keep interest rates below inflation. As prices rise, they repay yesterday’s debt with today’s dollars that are worth less. On paper, the debt is still there… but inflation is slowly eroding it.

For example, a $10,000 mortgage in 1960 could buy you an entire house. Today it can barely cover a few months of rent. Inflation ate away the value of that mortgage. Similarly, if the government is paying 2.5% interest on $40 trillion of debt, but inflation is at 6%, the debt is actually shrinking by 3.5% per year. The government is slowly reducing its burden – but the people are absorbing the cost.

But this isn’t the first time this is happening. And to know why it’s scary, you need to know who paid the price for it the last time:

World War II and Financial Repression

Debt takes a back seat during war when the first priority is winning. During World War II, we took on more debt than ever, because it was an existential crisis. The hope was that we could win and pay it back later. If we didn’t win, it wouldn’t matter anyway. US debt hit roughly 106% of GDP back then, just a little more than where we are today.

{kind=link}

Once the war ended, the question was: How on earth are we going to pay it back?

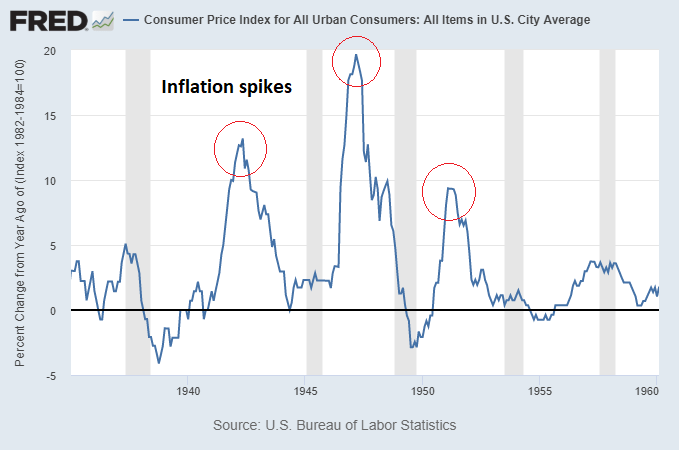

Here’s what they did: Under direct pressure from the Treasury department, the Fed pegged interest rates at artificially low levels: Treasury bills at 0.375 percent and long-term Treasury bonds at 2.5 percent. Those rates were fixed from 1942, all the way until the Fed-Treasury accord in 1951. This wasn’t because the economy needed it – the government had no choice other than this to stay afloat.

Of course, fixing rates artificially low for a decade meant runaway inflation. While interest rates remained at 2.5%, some points even saw 10% price increases.

In real terms, after accounting for inflation, savers and bondholders were earning negative returns on their money. Buying a treasury technically made you 2.5%, but with inflation at 8.5%, you lost 6% in reality. While savers got poorer, the national debt slowly got healthier. This strategy was financial repression – denying the public the ability to build wealth through savings, so that government debt could be managed.

But it worked. An IMF paper found that without this combination of low rates and “surprise inflation,” the Debt-to-GDP ratio would have fallen to just 74% by 1974. In reality, it reached 23%. The math is undeniable. It wasn’t growth or responsible budgeting that solved the post-war debt problem – it was financial repression.

Why is this relevant now?

Financial repression has been used before, it worked. The conditions to use it again are showing up in almost exactly the same way. So you need to understand what the Fed plans to do:

Shrinking the balance sheet

On May 15th, Kevin Warsh was appointed as the new chair of the Fed, and his entire thesis is this: The best way to get interest rates down is to shrink the Fed’s balance sheet. That might sound completely backwards. If the Fed sells bonds, supply goes up, and prices fall – which usually means rates rise. So why is Warsh saying the opposite?

His argument is that the current system is distorted. The Fed’s own balance sheet is now part of the problem. After years of buying bonds and printing money, the Fed is sitting on roughly $6.6 trillion in assets, and banks are holding a huge amount of extra reserves. If the Fed didn’t do anything now, banks would undercut each other to loan that money out through the financial system. So the Fed actually pays them interest to do nothing.

In other words, the Fed printed more money than the system could handle and has to “bribe” the banks to sit still. On top of that, a massive balance sheet makes outside investors nervous – if the government just keeps printing money to pay its own bills, it creates an “inflation risk premium” where long-term rates stay high because nobody trusts the Fed to bring inflation under control. A smaller balance sheet signals discipline, and long-term rates could start drifting lower naturally.

That’s why, Warsh’s argument is simple: Shrink the balance sheet, banks stop getting bribed with high rates, and the Fed actually regains the ability to cut rates without triggering an inflation spiral.

Finally, there’s the AI wildcard. Warsh believes AI could make the economy grow faster without causing as much inflation. If he’s right, it gives the Fed the ability to lower rates while growth and inflation shrink the value of the $39 trillion debt. Do you think AI will actually deliver on its promise and accelerate the economy?

If all of this fails, the government could use a sneaky trick to cut interest rates:

Inflation is whatever they say it is

We like to think that CPI inflation reports are accurately telling us the full picture. But when you get down to it, these are all numbers that could be manipulated to tell you whatever they want you to believe. And yes, this has been done before.

For example, there’s the Substitution bias: In the 1990s, inflation was revised to account for “a change in consumer behavior.” The old inflation number assumed that, if steak gets expensive, you’d still buy steak for a higher cost. But the data showed that people instead save money by buying chicken. Therefore, people spend less, and food inflation goes down all of a sudden. Genius, right?

Here’s the problem: It’s true that people adapt to higher prices by purchasing low-cost substitutes, but you’re measuring the cost of what people can afford to buy, not the cost of what they used to buy.

There’s also Hedonic adjustment. If a car gets more expensive, the government can say part of that price increase isn’t really inflation because the car also got better – maybe it has more safety features, better fuel efficiency, or a nicer interior. So they adjust inflation downward to account for the “improved quality.”

Apart from the optics of controlling inflation, a lower CPI means the government owes less in interest. Every 0.25% reduction in measured inflation saves the government hundreds of billions in automatic payment increases over time. There’s no conspiracy here. It’s a plain incentive to push for lower numbers. The same thing could happen with job numbers as well. Initial reports showed strong job creation, and revisions months later showed real numbers were much weaker. The same person working two jobs is counted twice: So if 100,000 people picked up a second job, it says “100,000+ jobs added” – but it’s misleading because those people need a second job just to stay afloat.

Let’s sum it all up and see what it means for you.

Here’s what the government is most likely to do:

Taxes are going up: It’s common sense. As deficits compound and the interest burden grows, the political math eventually has to find new ways for the government to make money. Things like “The One Big Beautiful Bill” added another $4.6 Trillion to the 10-year deficit. Someone has to pay for that – and that usually comes from raising taxes on higher earners, closing loopholes, and higher capital gains. The math won’t math without more money.

They will print more money and keep rates below inflation for as long as they can. Financial repression won’t be announced in a press conference. It’ll happen through silent pressure on the Fed Chair, until low real interest rates quietly eat into the purchasing power of cash and low-yield savings. The people who will get hurt most are the ones sitting in cash, savings accounts, and fixed-rate bonds.

The data will get harder to trust: When the government has an incentive to show smaller numbers, the methods they use will drift in that direction. CPI substitution, downward jobs revision, and random adjustments will be normalized. Not every number is fake, but if the numbers don’t reflect the actual pain you feel when paying for groceries, rent, and gas – then are they right?

The worst thing you can do right now is to sit on a pile of cash assuming it’ll be worth the same thing in 10 years. It probably won’t.

That doesn’t mean you should panic and go all-in on one crazy bet (this is the other mistake people tend to make). Inflation acts over time, and the way to resist it is to own assets that have a better chance of keeping pace, historically, like stocks, real estate, some gold – and maybe even commodities and some bitcoin. None of these are perfect on their own, but they can help with the real issue, i.e inflation eating your money’s purchasing power.

The system usually finds a way to transfer wealth from savers to borrowers. But once you understand what’s happening, you can avoid getting blindsided by it. So keep investing, stay diversified, and please, if you found this useful, like, restack, and share this post with a friend you don’t want to get left behind.

I’ll see you next week,

– Graham

Today’s post is Sponsored by DeleteMe. Take a moment to check them out if you haven’t already.

The AI editing is so obvious and makes your work unreadable.

While financial repression worked well in the 1940s - 60s, the circumstances facing the U.S. then were far different from today.

The U.S. was the last manufacturing base standing during much of that period. Whatever the U.S. did, they got away with it — they were the only fully functioning financial system in the world.

That is very much not true today.

Hopefully Kevin Warsh understands this.