End of an era at the Fed

Jerome Powell is leaving

Something just happened to the Fed that will influence the economy for at least the next four years. Jerome Powell just spoke at his final meeting as Fed Chair.

For years, the financial world had been primed for a policy of lower interest rates and easy money. Even the high rates over the last couple of years were seen as temporary measures setting the stage for a course-correction this year. That era is now over. During his final meeting, Jerome Powell decided to pause all interest rate cuts for the foreseeable future. However, the real story is in who’s about to take the helm next.

Donald Trump has selected Kevin Warsh to replace Jerome Powell as the Chair of the Federal Reserve. While Trump has been pushing for rate cuts, Kevin Warsh has a track record of opposing stimulus measures during the 2008 Financial Crisis, and he even fought to keep interest rates higher for longer in 2010. Warsh is seen as a hard money hawk who’d rather risk slow economic growth and falling prices than overprint money and devalue it.

So everyone is waiting to see what he’ll do. But why does this matter right now?

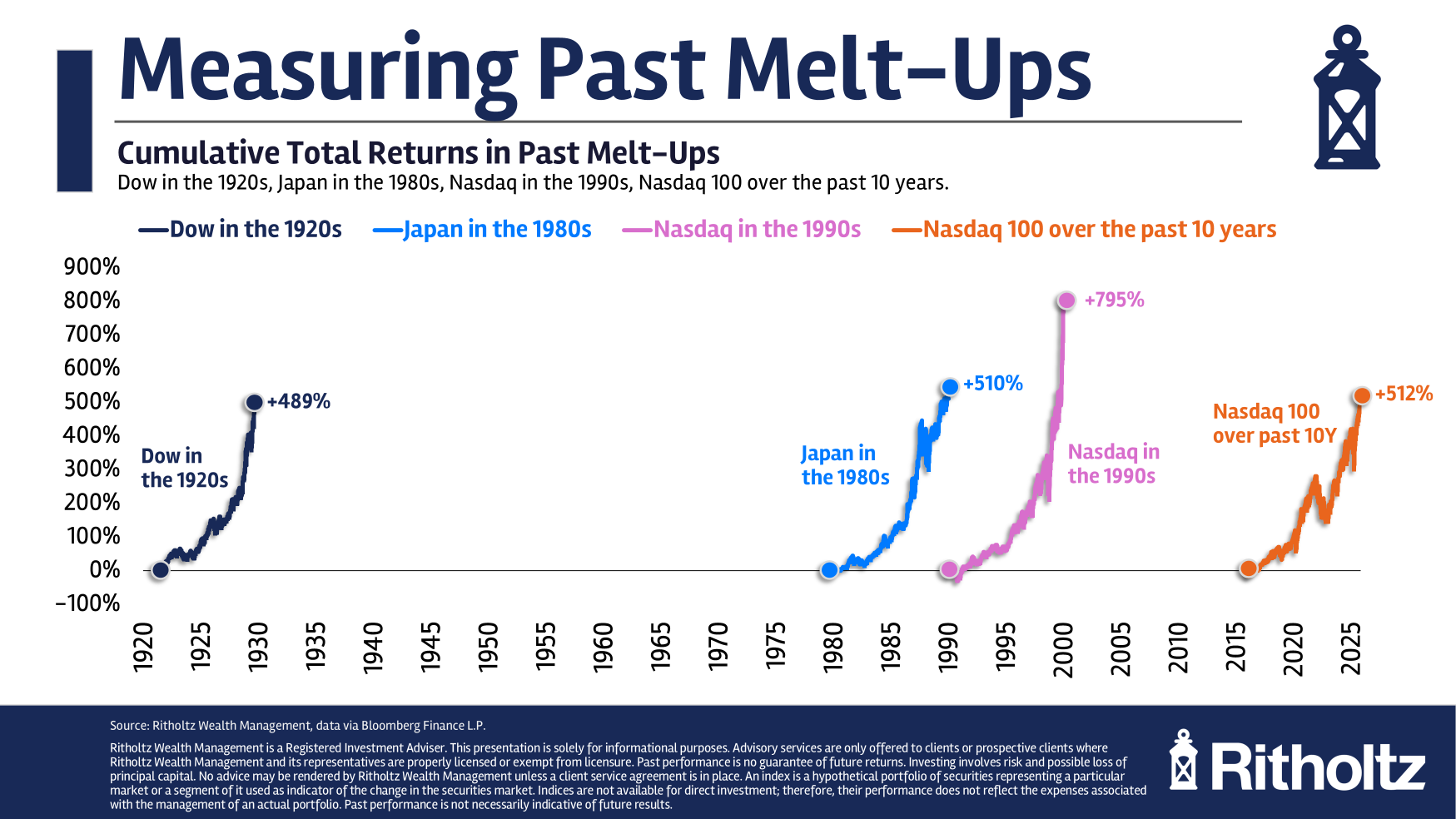

You only need to look at the market to understand. Despite warnings of speculation, the markets are back at new all-time highs, Bitcoin is trading near $80,000, and even home purchases are starting to increase. Some analysts are calling this a melt-up in which asset prices are ballooning to unreal levels.

While the party looks like it’s never going to stop, the bill is about to come due. The appointment of a hawk like Kevin Warsh could remove the safety net that investors have relied on for over a decade. This period of transition, when there is a change in Fed leadership, is historically volatile – Since 1930, the stock market has seen an average decline of 16% whenever a new chair takes office at the Fed.

How did this play out in the past, and how should you invest to weather out this transition? That’s what I’ll cover today. But before that, if you’re new here, hit the like button for free and join 40,000+ investors who never miss one of these timely updates.

The Return of the Hawk

In the late 1980s, there was a major pivot in America’s philosophy. Inflation had been spiraling out of control, and the Federal Reserve needed a leader who was willing to look unpopular doing the hard thing. Along came Paul Volcker, who raised interest rates to unprecedented levels (up to 20%!) in an attempt to break stagflation – and it worked, despite causing a painful recession in the short term.

Kevin Warsh seems to belong to the same school of thought. His history at Morgan Stanley and his previous tenure on the Board of Governors suggest he values the central bank’s independence over everything else – he has stated that monetary policy independence is essential, and that the Federal Reserve must act in the interest of the nation with unclouded decision-making.

This is particularly interesting because Donald Trump has been vocal about his desire for lower interest rates. By appointing Warsh, Trump is choosing someone who might actually defy those wishes in favor of sound money. But Warsh faces an additional challenge as well.

Oil woes

Warsh is being handed the persistent issue of inflation when he steps in. But now this is being driven by a powerful force that he can’t really control: The price of oil. You probably feel the direct effect of oil prices going up when you fill up your car, but it’s also the lifeblood of the global supply chain. Everything from the cargo ship that transports goods to the tractors that bring food to the shelves is affected by oil. When oil goes up, so does everything else.

Every ten dollar increase in the price of crude oil raises inflation by 0.2%.

It also sets back economic growth by 0.1%. So how are we doing?

Earlier this year, oil was trading at $57 per barrel. Today, it sits at close to $102. This spike alone implies that inflation could rise by 0.7% in the coming months, undoing all the progress of the last few years. We are already seeing the effects of this trend – inflation recently ticked back up to 3.3%. If Kevin Warsh wants to focus on long-term stability and bring inflation under control, he is unlikely to lower rates and add fuel to the fire.

The rising cost of resources is a risk to every business, but as an investor, your most valuable resource is your own personal information. If you have ever bought a property, you might be surprised to learn just how much of your transaction history – like your home address and loan amount – ends up as a matter of public record. While this is a normal part of the real estate process, it is important to know how you can shield your financial life from prying eyes.

Unfortunately, data brokers legally collect and sell this public information – along with your past addresses and phone numbers – to anyone with a credit card. As an investor, this paper trail can leave your hard earned wealth at risk for targeted financial scams, phishing, and identity theft.

That is where DeleteMe can help you. It’s a hands free subscription service that removes your personal information from hundreds of data broker websites. Their privacy experts do the heavy lifting, continuously monitoring and removing your data all year long so those records do not just pop right back up.

Today’s post is Sponsored by DeleteMe

Take control of your data. Protect your digital presence and investments.

Get 20% off your DeleteMe consumer plan by clicking the button and using promo code GRAHAM at checkout:

Now let’s look at one of the most baffling puzzles in the economy – the gap between the market performance and consumer sentiment.

The market-consumer paradox

The stock market recently saw a 10% rally in just ten days. This is one of the strongest surges we have ever witnessed. The NASDAQ even went on a thirteen day win streak, which is the longest seen in over thirteen years. On paper, everything looks incredible.

And yet, consumer sentiment is hitting its lowest point ever in the seventy year history of the survey.

How do you explain this disconnect? Here’s what’s going on:

The market is forward-looking, pricing in what investors expect to happen in 6-12 months. Consumers, however, live in the present. Wall Street is betting on a bright future, while Main Street is struggling to pay for groceries and gas today.

Historically, high fear correlates with low market performance. But today, sentiment is low even as prices remain high – this is a very fragile situation, where the market is held together by optimism and liquidity. If the Fed moves forward with its plan to shrink the balance sheet, the liquidity supporting this rally will drain away and cause panic.

Are you finding your sentiment as a consumer different from your sentiment as an investor?

The Stalemate in Real Estate

The stock market won’t be the only place affected. The transition to a Warsh-led Federal Reserve also has major implications for the housing market. Currently, we are seeing a national stalemate. Home prices have risen another 1.4% YoY, yet organizations like Zillow have downgraded their forecasts across four hundred different markets. They now predict that over the next 12 months, prices in many areas will remain completely flat.

We can see the cracks forming in specific regions, particularly in markets like Las Vegas. During the boom of the last few years, many investors purchased properties with the expectation that values would never stop rising. Now, inventory is piling up as buyers are priced out by high mortgage rates while sellers are getting desperate. It’s becoming common to see properties selling at a 5-15% loss compared to their purchase prices from 2021 or 2022. Sellers are refusing to lower their prices, and buyers are waiting it out. It’s a game of chicken where nobody wants to blink first.

The hope for many has been that the Federal Reserve would cut rates and make homes affordable again. That’s doubtful. But even if it does happen and inflation cools enough to allow for a slight dip in mortgage rates, some analysts believe they will only fall to 5.7% by the year 2030. A drop of that size only increases the purchasing power of a buyer by about 5%. It won’t solve the affordability crisis.

The Digital Hedge

As investors look for ways to protect themselves, many are turning to Bitcoin. While the S&P 500 is up 8% this month, Bitcoin has surged by 13%. More institutional money is flowing into Bitcoin exchange traded funds than ever before, and companies like Strategy now hold more Bitcoin than the United States government.

The narrative around Bitcoin is shifting. It’s no longer just a speculative asset for retail traders, and is becoming a hedge against the rising national debt. Even though Bitcoin is still down from its all time highs, the renewed interest from banks like Goldman Sachs and Citi suggests that the digital asset is here to stay.

I have personally used the recent volatility as an opportunity to lower my average cost. When it fell to $60,000 and the general sentiment was that it would never recover, I saw it as a buying opportunity. In my experience, the best time to buy is often when the rest of the market is the most terrified. However, I maintain a balanced approach, with less than 15% of my portfolio in crypto. This allows me to participate in the upside without risking my entire financial future on a single asset class.

The arrival of Kevin Warsh marks the beginning of a new chapter in American finance. We could be moving toward an era of discipline and hard money, or we could see the independence of the Fed being tested. This transition will not be smooth. There will be moments where the market feels like it is about to collapse, and there will be moments where it feels like it will never stop rising.

The lesson we should take from the recent rally is that the market rarely behaves rationally in the short term. The people who sold everything in April to wait for clarity missed out on one of the fastest recoveries in history. The people who waited for Bitcoin to hit $50,000 missed a twenty percent gain in two months. Trying to outthink the collective wisdom of every hedge fund and algorithm on the planet is a losing game.

The only strategy that has consistently worked is to have a plan and stick to it regardless of the headlines. Decide how much you can afford to invest each month, choose a diversified allocation that allows you to sleep at night even during a major drawdown, and let time do the work. No matter who is sitting in the chair at the Federal Reserve, the power of consistent investing remains the same.

As you look at the headlines over the next few weeks, remember that volatility is the price of admission for long term gains. Keep your head cool, ignore the panic, and continue to build your future one month at a time.

If you found these insights helpful, like this post, restack it, and consider sharing this with someone who is trying to make sense of the current chaos. It helps a lot!

I’ll see you next week.

–– Graham

Warsh is not a monetary hawk, he’s a partisan hack that’s always for high rates with a Dem in the WH and easy money for Repubs. Just wait for the rationalizations to come as he argues for rate cuts from day one.

Nice one. I’m writing my about the fed at the moment. Episode coming out next week