Index Fund Bubble

Is passive investing inflating the stock market?

Could Index Funds Be ‘Worse Than Marxism’? – The Atlantic

“Index Funds Are Like Subprime CDOs” - Michael Burry

There has been a growing chorus recently that the index funds we all love and cherish might just be one big bubble. According to Michael Burry (You know, the guy who called the 2008 financial crisis) index funds are driving stock prices to unsustainable levels and he has warned that the longer it goes on, the worse the crash would be! Finally, even Jack Bogle, the creator of index funds was concerned with the rising concentration just before his passing.

I do not believe that such concentration would serve the national interest - Jack Bogle (2018)

As a self-proclaimed index fund connoisseur, I feel it’s very important that we deep-dive into this issue to determine if index funds are actually creating a stock market bubble - and more importantly, what that means for your money!

What is an Index Fund?

In order to break this down and discuss what exactly is going on, we need to start from the very beginning! An index fund is basically just a big basket of stocks that you can invest your money into. Instead of owning stocks of one single company, you own a small piece of all the companies in that basket.

For example, if you have $1k to invest, instead of betting it all on one company, what you can do is invest it in the S&P 500. That way, you are diversifying your holdings across the top 500 companies in the U.S instead of going all-in on one stock that you found intriguing on WallStreetBets.

The fun part is that index funds are so popular right now that you can literally find one for any type of investment that you can think of! Don’t believe me? Here is a list of some interesting index funds:

MILN - Tracks the spending habits of millennial consumers and invests in companies that are expected to gain from them

GAMR - Invests in gaming companies

COW - Provides exposure to farm machinery, packaged meats, etc.

SLIM - Exposure to companies positioned to profit from servicing the obese (Fund has been liquidated)

The benefit of the index funds isn’t just owning a small amount of everything. They have also been very profitable. In fact, so profitable that studies have shown that 95% of professional portfolio managers could not outperform the market index over a 15-year period.

Warren Buffet trusts index funds so much so that he recommends investing in an index fund above his own Berkshire Hathaway stock and went so far as to make a Million dollar bet in 2007 that a collection of hedge fund managers won’t be able to beat the market over a 10-year period. Guess who won in 2017? That’s right: Warren Buffet

The Issue

Given that index funds seem to be the perfect investing instrument, what’s the issue now? Could these simple instruments pose a huge risk to the entire market that we are not seeing? There are two main issues that get highlighted whenever index funds are discussed.

Price Discovery

The main argument against the index fund is a very logical one. The basic premise here is that an index fund affects the price discovery of stocks in the market. When you are investing in an index fund, you are really just investing in a big basket of stocks - This means that anything within that basket automatically gets your money. Herein lies the issue.

If a stock is bid up just based on its presence in an index and not by analyzing the underlying asset, then it can lead to a bubble-like scenario where you are buying more and more just because the asset prices are going up.

In other words, index funds make more money, which causes people to invest more money into them, which then means the demand goes up for those funds - which causes even more people to buy in and repeat the cycle over and over again.

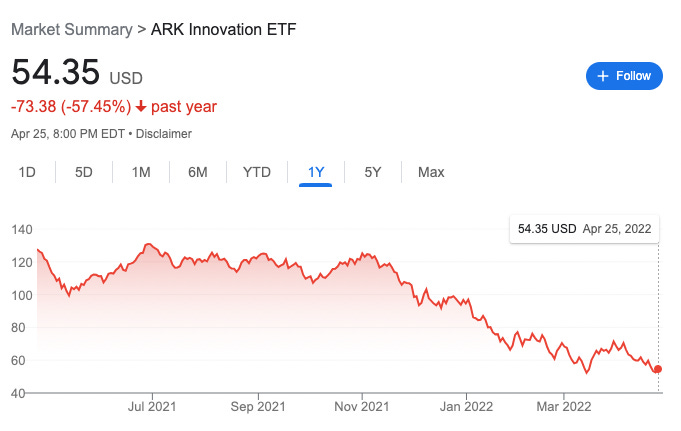

Many criticized ARK ETF for similar reasons: Its innovation fund contained some of the most successful stocks throughout 2020 and as people saw the gains they poured money into the fund. We all know how that turned out.

Low Liquidity

The other concern is, what would happen if a large portion of investors want to liquidate their index fund positions? This would disproportionally affect the smaller stocks held within that index fund.

The reasoning here is that there is a lot of money that’s being invested in these small companies that don’t have a lot of trading volume. So, if a sell-off occurs, there wouldn’t be any buyers for these smaller companies and this would cause an exacerbated crash.

For example, in the Russel 2000 index fund (which tracks 2,000 small-cap stocks in the U.S), half the stocks have a trading volume of less than $5 million per day and 25% of those stocks have lesser than $1 million per day. A large sell-off would be catastrophic for these small companies.

What does the data say?

Before getting carried away by these predictions and opinions, it’s very important to see what we are observing in the current market. The hypothesis here is that once a stock is in the index, it will automatically have money thrown at it and that it will cause the price to go up.

To check this, we can look at the stocks that were added to the index and the stocks that were removed from the index and see if the price goes up or down based on the index inclusion/exclusion. When it was researched, it was found that stocks do generally see a rise in price once it’s announced that they are going to get added to an index, but once they are added, the pent-up demand slows down and the stocks return to a ‘new normal’.

What’s more interesting is that long term, it was found that adding a stock to the index had no permanent effect on its price. This detailed analysis by Market Sentiment found that index inclusion has its maximum impact in the week leading up to the inclusion and then falls due to profit booking. Overall, it was shown that stocks that got added to an index did not see any superior performance over stocks that were not traded within an index.

Another problem of just looking at the fund-inflow statistics is that stock price is not solely decided by the amount of fund inflow but majorly by trading.

As per this extensive study done by Vanguard, only 5% of the overall trading volume is captured by index funds. The remaining 95% of the trading is made by active traders, pension funds, and institutional investors.

The low liquidity argument is also a moot point because of how an index fund works. Within the S&P 500 (a market-cap-weighted index fund), the top 10 companies make up 28% of the overall holdings. That means that the other 490 companies split the remaining 72% of the investment and would only get a fraction of a percent of the passive investment that flows into the fund. In other words, if you are putting $100 into an S&P 500 index fund, Apple would get around $7 and Ralph Lauren would only get 1.5 cents.

So in the event of a mass sell-off, since each stock is only bought in direct proportion to how large it is by market cap, everything should get affected proportionately.

The only real concern that I have related to Index funds is the same one Jack Bogle was highlighting - Voting Rights. Normally, when you buy a stock, it entitles you to the voting rights of the company and if you get enough stock, you theoretically can do a hostile takeover. When you are buying into an index fund, you own a small piece of the basket and not the stocks themselves. So if the trend continues, 3 fund managers (Vanguard, Blackrock, and State Street) would dominate 81% of the voting control of virtually every large U.S corporation and that’s worrisome.

All the other data from my research shows that we are nowhere near a situation where the index funds can alter the price discovery in any significant way! Even if it could, it would leave some really big opportunities for active fund managers to profit from the stocks that were undervalued and beat the market - something which we are not currently observing.

So given all this, in terms of any immediate danger, I am not losing my sleep over the index fund bubble. Yes, voting rights might be an issue in the future, but assuming they have the best interest of investors in mind, they should be voting in your favor. Plus, what’s the last time you ever actually cast a vote for the stock you owned?!

If you enjoyed this piece, smash that like button and share it! Thank you.

Thank you Graham, as always, we appreciate you and the value you provide to us with your financial insights.

A related post on that subject: https://www.asiancenturystocks.com/p/etf?s=w