What’s up guys, it’s Graham here :-) If you want to join 29,420+ smart investors and never miss an update on the market, hit the subscribe button below. It only takes a second and is completely free.

If you haven’t heard the term “Boomer”, you’ve probably been living under a rock. But did you know that this meme-like term is actually the result of one of the most prosperous times in American history? A Boomer was someone born during the Baby Boom from 1946 to 1964 – a period where innovation flourished and we dominated the manufacturing sector. Consumerism was practically invented in this era.

The reason was simple. World war II ended, and the US was lifted by a wave of optimistic servicemen who were returning home. But the Government had its hands full – all economic activity had been paused to aid the war, but now there were millions looking for jobs that didn’t exist. Some even warned that a recession was imminent. The government responded by keeping interest rates low to promote manufacturing. The GI Bill was also introduced to give servicemen access to low-interest, zero down-payment home loans.

The results were beyond anyone’s wildest dreams. As Morgan Housel says:

1.9 million homes were built from 1940 to 1945. Then 7 million were built from 1945 to 1950. Another 8 million were built by 1955.

It was cheaper to pay a mortgage than to pay rent! On top of this, marriage rates peaked between 1941 and 1946 – Americans had won their war, and they were impatient to start their own family. The house was the symbol of the newly started family, and it was the basis around which all economic activity was built (I highly recommend Morgan Housel’s article if you want to learn more).

World War II changed family structure, and families changed the housing market. Demand for housing is based on people’s hopes for the future, and when the structure of society changes, the housing market changes. Well… it’s happening again. There is a fundamental change going on in the fabric of American society now and it has started reflecting in the housing market – but this time, it’s the opposite.

The plates are shifting

Housing prices have dropped for the fourth month in a row. Housing sales were down by 35% in November – The largest drop on record. There are talks of “a real estate reckoning” around the corner. And this time, it’s not the bursting of a bubble or a transient phase that we are going to weather till times change. The underlying economic factors that dictate housing market prices are changing. Let’s look at the most important ones:

Interest rates: We are seeing the most rapid acceleration in mortgage rates in the last 20 years – After a couple of years of cheap interest, we are now hovering at the mid-2000s level. But the catch is that the circumstances are not the same. Median home values in the 2000s were $187,000 but now they are $454,000 – A 143% increase. If you look at median incomes though, they haven’t caught up – They have gone up only 70%. This causes an impact on…

Fastest rise in mortgage rates in the last 20 years | Source: FRED Consumer spending: The intention behind hiking the rates was achieved – When stimulus checks were being YOLOed into the stock market and supply chains were being clogged up, inflation became a real problem and the only solution was to restrict customer spending by making credit more expensive. But with less disposable income at hand, consumers are spending lesser not just on cars, luxuries and holiday expenses, but also on buying houses.

Increasing lay-offs: We haven’t seen the full scope of this yet, because unemployment is typically a lagging indicator that turns up at the end of a recession. But as layoffs are now becoming larger and more frequent, there is less upper pressure on housing – the desire to commit to a mortgage is lesser when your job is at risk.

Source: Reuters Rising inventory: The number of houses for sale went up 15% YoY but the median price increase was only 1.5%. Moreover, 6% of all listings are seeing a drop in price. As listings pile up and mortgages haven’t started falling yet, there are no takers for houses on sale.

It’s the perfect storm in the housing market where all factors seem to be conspiring against sellers. But shelter is a basic need. If there isn’t any traction in the buyers and sellers market, the momentum is transferred elsewhere…

Renting

Generally, rental prices are incredibly stable, and they tend to be a lagging indicator when times get bad. For example, when the housing market crashed in 2008, rents actually increased and stayed that way till about 2010 when the recession ended. They only started to drop after that. The reason was that people were losing their homes, but they could not afford to buy a house – this gave landlords pricing power, and rents started to rise.

Tenants were also locking in 1-2 year leases so that their rents would stay the same. It was only a few years later after tenants started to leave in favor of buying their own homes that the rents began to drop. It seems like the exact same situation is repeating now, with housing sales dropping. Despite that, rents are dropping.

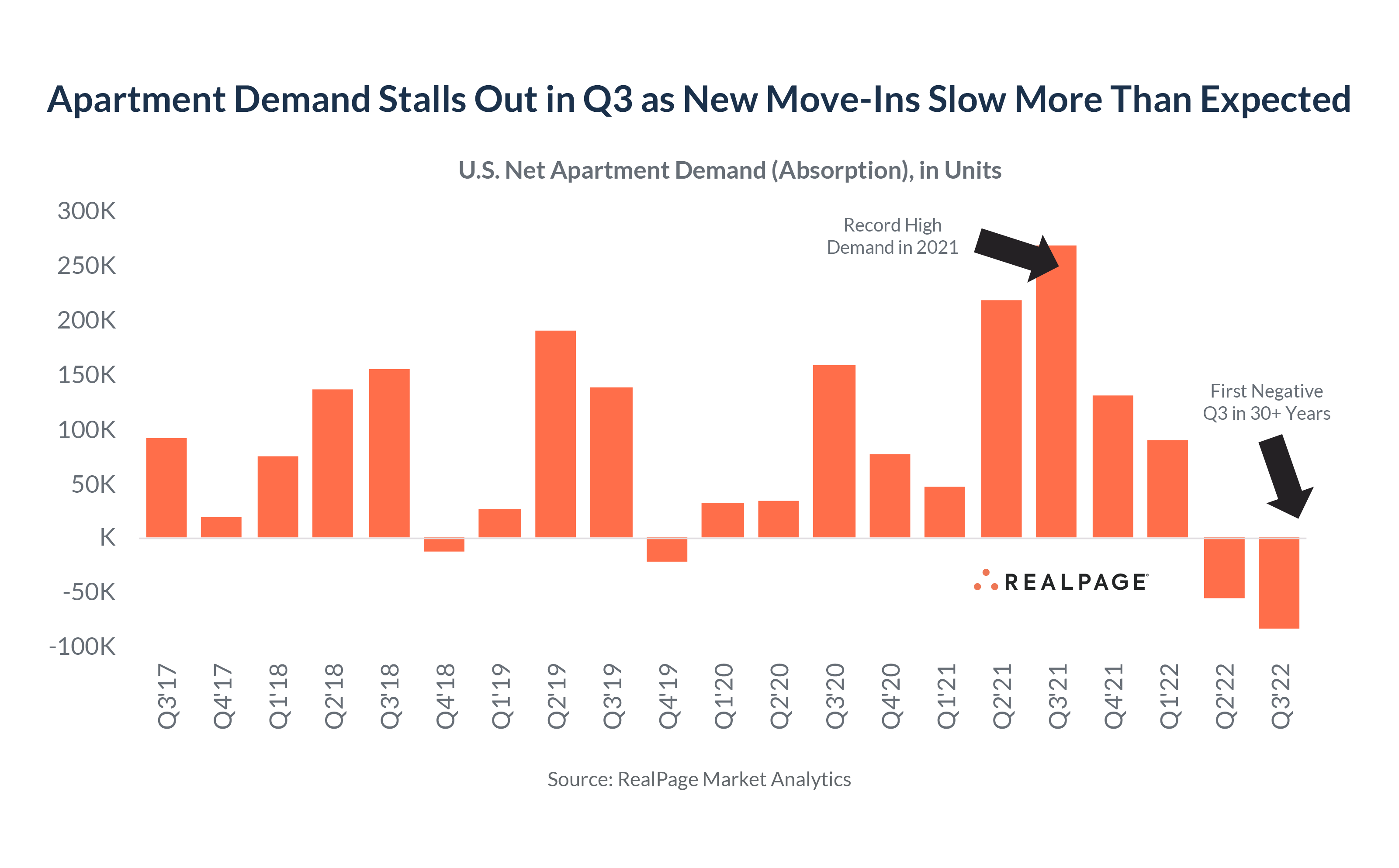

In fact, across the United States, less than 50% of landlords raised rent by more than 3%. The other half raised rent by less, or even nothing. RealPage found that national asking rents fell 0.59% in November.

Why is there a sudden reversal? The answer is again changing social structure.

Camping at home

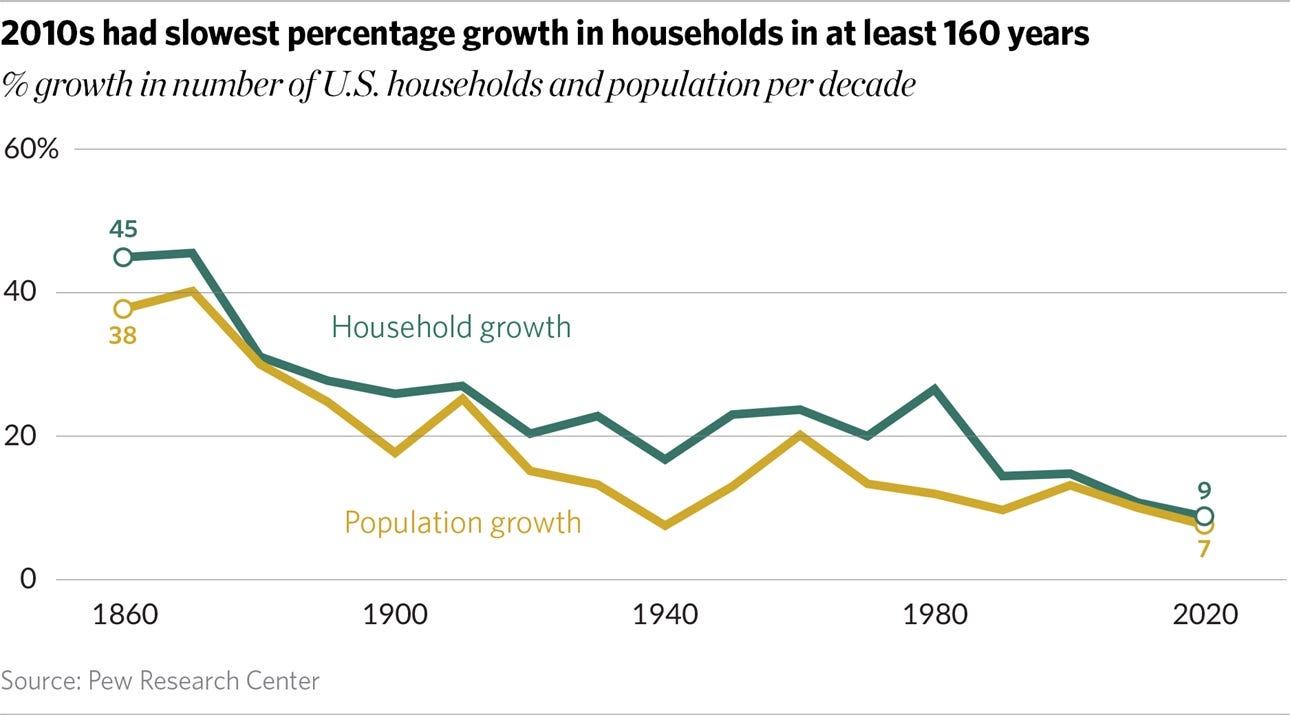

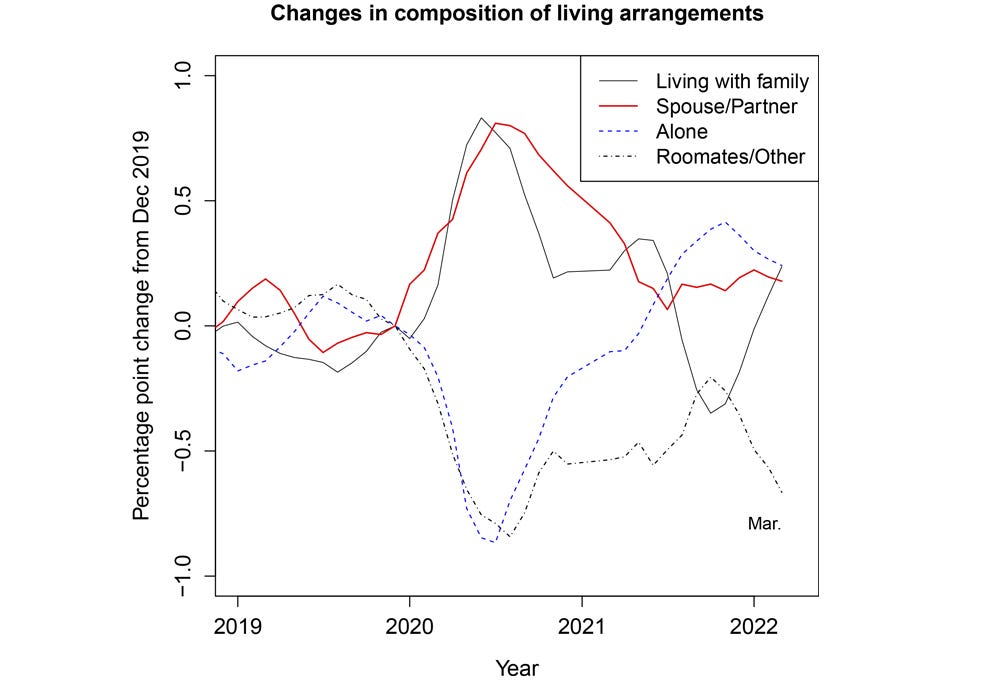

There has been a decline in the rate at which young workers strike out on their own and establish their own households since the Great Financial Crisis. The pandemic just aggravated this problem, with more people living with their parents or sharing a house with other roommates rather than committing to a house of their own. This is the exact opposite of what happened after World War II – An expansion of American families and creation of new households led to a housing boom. Now, families are shrinking, and demand is dropping.

Creation of new households is measured by the Headship rate, or the number of households divided by the size of the population. If the Headship rate decreases, it means that new household formation is shrinking. In 2020, there was a severe decline in the headship rate as people moved in with their families, and a brief recovery after interest rates dropped. But now, the headship rate has started dropping again in tandem with the rate hikes. As this phenomenon becomes more normalized, landlords lose their bargaining power. There is a fallback option for tenants that didn’t exist before, but the only option homeowners have is to reduce rents.

75% of landlords said that they intend to raise rent at least by something, but, they also point out that “smaller landlords are less likely to raise rents during the renewal period, since a vacancy would have a larger financial impact to them – than an institution, where rent is spread throughout hundreds or thousands of units.” Of course, rent decreases are not uniform. While rents in New York are down 10%, and Milwaukee and Minneapolis are seeing large declines, Oklahoma is up 24%!

Most headline rent increases are reported from tenant turnover, not increases on existing tenants, and most of the rent increases we do see were landlords wanting to have rental rates closer to the current market value. Apartment construction has reached 40-year highs, with more than 917,000 units under way, estimated to be completed in the second half of 2023 – meaning, there’s about to be a lot more units on the market, and not enough rental demand.

So what does the market look like in 2023?

The road ahead

There are a lot of predictions for 2023, and frankly, they’re not all in agreement. The National Association of Realtors believes that home values will be completely unchanged from where we are. Half the country may experience small price gains, and the other half could see small declines. They also believe that mortgage rates will stabilize around 5.7% by the end of the year. Realtor.com is more optimistic, predicting that home prices will increase by 5.4% throughout this year.

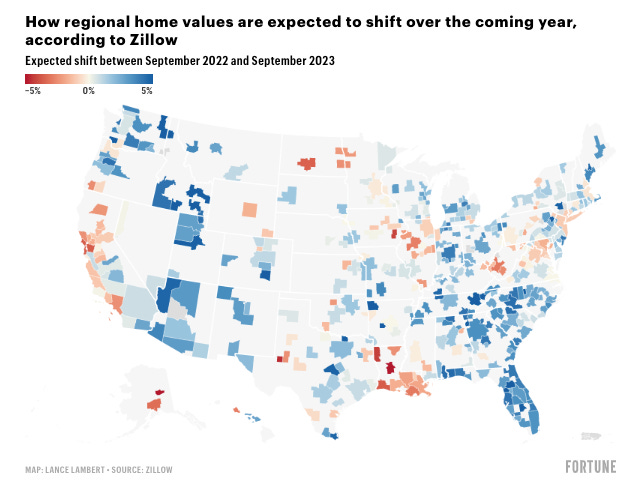

Let’s also look at some data-driven approaches. Zillow aggregates data to arrive at a consensus of market conditions. For 2023, their projection is that price declines will be moderate across the US with vacation destinations taking the biggest hit. This will also be the year that conditions begin to favor the buyer, although the areas in blue might continue to get more expensive.

The analytics company CoreLogic forecasts that housing prices will rise by another 4.1% through October 2023 (though they tend to “correct” their numbers on a monthly basis – so take it with a grain of salt). Anyway, in terms of overall housing values, the general consensus seems to be that: appreciation is local, and even though coastal markets are likely to see a 5-15% drop, other parts of the country could stay the same, or even get more expensive.

You can't connect the dots looking forward; you can only connect them looking backward.

– Steve Jobs

I’m pretty sure Steve Jobs was not talking about the housing market when he addressed Stanford graduates, but what he said holds for any kind of paradigm shift – it’s tough to see how things will pan out in advance. On the other hand, there are a few basic takeaways that I can spot as a landlord and real estate investor myself.

I see 2023 as a year where we’re finally going to see the delayed effects from a slowing economy. Higher interest rates, weaker consumer spending, and continued layoffs will put a lot of pressure on landlords to hang on to their current tenants and delay rent increases as inventory piles up. As landlords begin to compete for a fixed pool of tenants, rents might drop further. If you are renting, this could give you the upper hand!

As far as home values are concerned – they will take a much longer time to adjust, like turning up the heat in a swimming pool which has a delayed effect. Only new buyers would be directly affected with payments going up, while a mild drop is the most-likely scenario with some hard-hit areas going down by around 25%. As all of our data shows, absolutely no one can predict the true impact of rising rates on the housing market. So, it’s best to only buy what you can afford, with a fixed rate mortgage, that you intend on holding for at least 7-10 years.

Which part of the US (or world) are you from, and how is the housing market reacting there? Let me know in the comments.

Stay safe, stay invested and I will see you next week – Graham Stephan.

A lot of effort and research went into making this article, so if you found it insightful, please help me out by clicking the like button and sharing this article.

Tampa Fl market is holding fairly strong. I flipped one house for a 50% gain last year and sitting on another one still up 40% in 15 months. I think most of Florida will see a more mild pullback this year due to the steady demand to live here.

Germany, Munich. Prices for houses stay on,last year level or even dropped a bit, the mortgage is around 5-6%. Rent prices is around 2200usd for a 2 bedroom apartment in New house.