What’s up you guys, it’s Graham here! If you want to join 13,500+ smart investors and never miss an update on the market, hit the subscribe button below. It only takes a second and it’s completely free.

If you’ve been following my journey as a content creator for a while, there’s one thing you know about me… I don’t really spend much. So much so that some of my initial videos were about how cutting down on buying expensive coffee and investing that amount would net you millions by your retirement age. Some would call it “extremely thrifty” but I prefer to be called… ahem… “fiscally conservative.”

Anyway, getting to the point - the road to wealth building consists of two parts: Saving money and growing it. While investing is what enables me to stay financially independent and build wealth, the habit of living well below my means in my 20s is what let me enter the game in the first place. I kept my expenses at $1,500 a month, and I lived off only the extra cash-flow that my rental properties generated. Within some time, I had decided that I would only pay for assets that gave me lasting value, or paid for themselves. The more wealthy people I met, the more I realized that they were all doing exactly the same thing.

But cutting down on spending isn’t just about how much you can save. It’s also about priming your brain for how to think about your money when you make it. Let’s see why that’s important.

Making it big

Getting rich can be the biggest impediment to staying rich.

- Morgan Housel

Winning the lottery is synonymous with “making it”. After all, a million-dollar prize out of nowhere can change your life overnight, right? Yes. But probably not in the way you think. Jack Whittaker won a lottery for $315 million at the age of 56 in 2003, but it didn’t quite go the way he expected. He was robbed outside a strip club, his marriage broke up, his grand-daughter died of a drug overdose, his home caught fire… and he eventually went broke. “Poor guy, he didn’t know how to handle money. I’ve heard hundreds of stories like this”, you think. But here’s the kicker to the story… Jack was already a millionaire before getting this windfall prize!

Jack’s story is not unique - A study in 2001 found that lottery winners saved only 16 cents on the dollar on average, and that they were more likely to go bankrupt within three to five years than the average American. Forget lotteries, even heirs of wealthy families who were 20 to 40 years old squandered or lost more than half of the money they received as an inheritance!

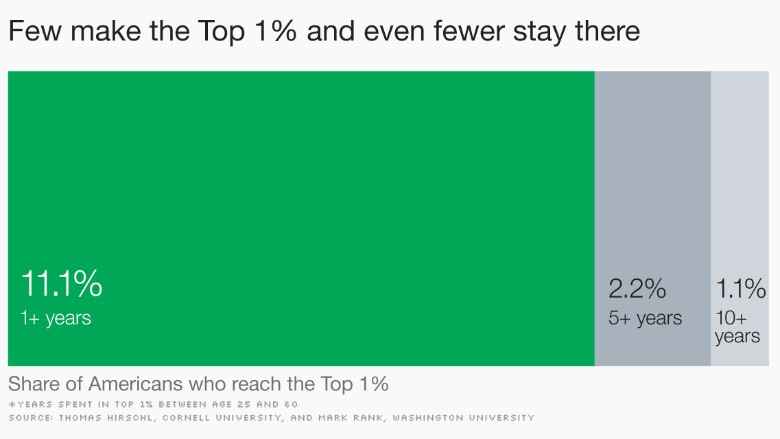

This goes to show how hard it is to keep money that you aren’t ready for. If you’re in the United States, statistically, you have an 11% chance of making it to the Top 1% of Earners for at least one year. However, your chances of staying there for more than 5 years is just 1 in 45. And your chances of staying there for more than 10 years? The answer is 1 in 100!

Only 1% of the top 1% will stay at that level for 10 years or longer.

Now, all of this is not to discourage you from making a million dollars. It also doesn’t mean that having a million-dollar windfall is going to destroy your life - On the contrary, developing the right mindset can help you both make and retain money.

Millionaire mindset

The unprepared mind cannot see the outstretched hand of opportunity

- Alexander Fleming

If the lottery-winning millionaires went broke, where does the wealth of all the other millionaires come from? That’s right: From saving and investing. In a study of more than 1000 millionaire households, it was found that 86% of them were self-made. What’s more, a large number of these were born into poor or middle-class households, and 26% of them struggled financially while growing up.

Yet, they were able to hit a million dollars through hard-work, diligence, and long term investing... On average, it took 32 years to become a millionaire. They knew how hard it was to make and keep money, and they preserved it when they did make it. Looking into this data, it’s clear that wealthy people are often the most frugal.

Most of these people got rich because they didn’t waste their money unnecessarily. But how did they put this into practice?

Every little bit counts. If you thought that coupons were only used by penny-pinchers, think again - Those pennies add up to a lot. A survey found that people earning over $100,000 per year are twice as likely to use a coupon than those earning under $35,000. Another survey by Millionaire Corner found that 1 in 3 people who have a net worth of $5 Million or greater shop at Walmart. What’s more, 50% shop at Costco, and 25% shop at Target.

People who earn faster tend to spend faster. Sportsmen like NBA and NFL players are textbook examples of people who get rich so fast that they have no idea about how to preserve it. Most of your wealth-building will happen in your 20s and 30s, so it’s important to build a saving habit right from youth.

Millionaires intuitively understand that wealth isn’t permanent - They are worried about unquantified risk, and save so much that they end up making much more than they require!Finally, saving money becomes a habit that’s hard to break. Even though they might be worth millions, it’s not surprising to see a millionaire bargain over a $10 overcharge on their account. That’s what got them there in the first place, and it keeps them there.

These tips are crucial to building the financial discipline to handle the wealth you are creating - At the same time, there’s something that I have added to this approach apart from cutting back on spending…

The secret ingredient

Coming back to my story, there’s a reason that being frugal is baked into my bones. I started working a part-time job when I was in high-school - and understood how hard it was to keep the money I earned. I was making $20 an hour. If a new pair of shoes cost $100, I was literally trading 5 hours of my life! I understood very early that time was the most precious asset and what it really cost to buy things.

Things got slightly better after I got my real-estate license. I would drive to Beverly Hills every day, and I was blown away by the fascinating properties that I saw there… At the same time, I didn’t let the new wealth change my spending levels. I retained my high-school mindset towards money and lived well below my means. Every penny counted, every dollar mattered. But where was the money going?

I was still spending it, but with a catch - I was spending it on my future self.

No, not like that.

I started investing the money in such a way that it would generate income for me that I could live off of without working. This is at the core of the “Financial Independence Retire Early” (FIRE) movement - If I have $20,000 that can give me a 4% annual return, that’s not $20,000… That’s an extra $800 for the rest of my life!

This started at $2,000 per month in 2012 from rental properties I had bought after 4 years of working full-time as a real estate agent. Today, it encompasses rental income, dividend income, capital gains, and distributions from the projects I’m passively involved in. I always make sure that I keep my spending well below what my investments make, so I can reinvest the difference and continue growing it!

But I was lying. There is one other thing I spend on.

The only exception

Over the last two years, there’s one more thing I spend on: buying back my time. As I’ve gotten older, and busier, I’ve recognized that there’s only so much that I can do in a day, and as a result, I’ve begun to outsource the tasks that allow me more time to focus on higher-yielding ventures.

For instance, I’ve hired a cleaning crew once a month to clean the house. I’ll order DoorDash on nights when I’ll be working late. I’ve also hired a full-time editor, Alex, along with help on the Podcast, The Iced Coffee, to make sure everything is running as smoothly as possible.

Even though these were things I used to do myself, taking a step back has allowed me to focus on the bigger picture, and, as a result, I’ve made more money than I’ve spent. At the end of the day, money is just about giving you more options. Options to pursue what you enjoy the most. Options to outsource the tasks you no longer enjoy. Options to focus your time on what means the most to you.

Money can buy you $5,000 Gucci clothing, but the real enjoyment comes not from buying things, but from having the option to buy them if you want to.

So, internalize the attitude of cutting down on spending, only spend on your future self, and keep building your cash flow till you make enough to buy back your own time… Soon, you’ll have built wealth of your own. And at that point, you’ll be ready to handle that million-dollar lottery. 😛

See you next week with another deep-dive!

And force of habit - Smash that like button to help others find this newsletter. Hit that subscribe button if you haven’t done so already!