The bill is due

A wake up call for credit card users

What’s up Graham, it’s guys here :-) If it’s your first time here, hit the subscribe button below to join 33,500+ smart investors and never miss an update on the market again. It only takes a second and is completely free.

Sometimes two unrelated events can combine to change the course of history forever.

When the phone rang in South Dakotan Mayor Janklow’s office in 1981, he couldn’t have anticipated that he would shape the American consumer’s future for decades. He ignored the phone call at first, but South Dakota’s economy was in a dire state – and he finally picked up the phone.

On the other end of the line was Walter Wriston, the chairman of Citibank. Citibank was in a worse situation than South Dakota. The bank had entered the credit card market with high hopes in the market in the 1960s when the interest rate was below 5%. But as the 70s got progressively worse, interest rates had shot up to nearly 20% – and there was no way to lend to consumers and make a profit. The credit card division was going down, and Citibank was going down with it.

But South Dakota saved Citibank. The bank could not charge higher interest rates in New York or other states, but there was no such upper limit in South Dakota – Citibank could charge more in late fees and they turned their business profitable. In return, Citibank brought more than 2,900 jobs to South Dakota and parked their assets in the state giving a boost to the economy. Other states and banks followed the example, and by the 90s the number of credit cards in circulation had doubled. Late fees were bringing in $2 billion annually to the industry!

But this soon started affecting customers who were being charged a hefty payment of $5 to $10 for a single day’s late payment. The profit gouging took its toll and in 1996, a Californian woman named Smiley Banks sued Citibank for violating California law with its late fees. The case led to a landmark judgment – in Citibank’s favor, and removed the cap on late fees. By 2020, credit card issuers had charged customers $12 Billion in late fees. The monster was out of the cage.

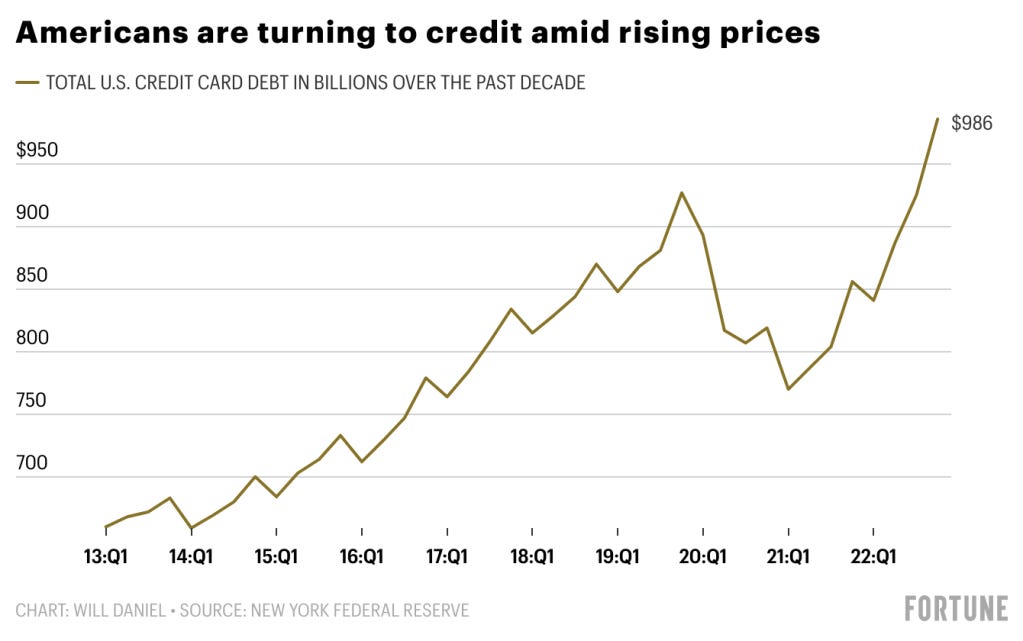

Now, things are coming to a head. Americans are using more credit than ever, and on the flip side, they are saving lesser than they used to – less than 3.4% of what they earn! US Credit Card Debt has reached almost $1 Trillion, and auto payments are falling behind at the fastest pace since 2010. Let’s take a look at how we got here, what the government is doing to fight it – and how you can make the most of this situation.

Debt in America

Let’s get a quick overview of where we stand. Over 80% of middle-income households cut down on their savings or dug into savings to make ends meet in the last three months of 2022. The more time goes by, the worse these numbers are looking.

46% of credit cardholders now carry credit card debt compared to 39% a year ago. Consumers spent roughly 30% and sometimes as much as 50% of the $2.7 trillion in excess savings they had built up during the pandemic, according to Morgan Stanley. Americans are burning through their savings at an alarming rate, and this could spark a recession. After all, 70% of the US GDP is supported by consumer spending, and with less disposable income, the economy is slowing down.

Unpaid balances recently increased by 6.6%, bringing the total amount owed to $1 Trillion dollars, the largest increase on record since 1999. On top of that, Credit Card users are facing what’s called “Triple Trouble” – More people are carrying debt, balances are up, and all this is at a time when rates are higher. This led to 18.3 million people falling behind on their payments in 2022, compared to 15.8 million in 2019.

So, what is the government planning to ease this situation? The unthinkable – they are looking to clamp down on credit card late fees.

Welcome relief

Here’s the thing: Since the Smiley vs Citibank case, Credit Card companies have had a field day with charging late fees anytime you fail to meet the minimum payment by the bill’s due date. It’s like rubbing salt on a wound to make a bad situation sting even worse.

Things are a little better now – The CARD act of 2009 capped the late fee. But even if you have a pending balance of $10, you could be charged up to $29 for your first default, and up to $40 for every subsequent late payment, on top of the interest that you would already be charged. As the economy slows down, this is becoming a real problem, and the White House wants to step in and fix this.

As they explain, when someone misses a due date even by a few hours, they’re hit with fees that far exceed the credit card company’s “cost to collect”. The amount collected from late fees is five times greater than the collection costs. If the intention of the late fee is to deter late payments, this is overkill – and it might not even be justified considering that late payments lead to higher interest and credit card companies make a profit every time you don’t pay by the deadline.

So, to give American consumers a little more time and leeway, the CFPB proposes a rule to limit late fees to a maximum of $8, and ban fees that are above 25% of the consumer’s required payment. Under these new rules, you would no longer get a $29 late fee when you miss a $10 payment, and a credit card issuer cannot charge more than $8 unless they can reasonably prove that their collection would cost more.

Now, in terms of how large that collection could actually be, it was found that the average credit card user carried a balance of $5,805 over the last three months of 2022 – which means that Americans are wasting $1,253 per year in interest alone at the average interest rate of 21.6%. As the Fed continues raising rates, this would only shoot up. Before we look at how you can rein in this debt and not fall into this category, we need to take a look at another critical problem…

The Auto Loan Crisis

It’s no surprise that there’s a substantial bubble because of used car prices. It was the perfect storm of a shortage of auto manufacturing, a limited supply of parts, record-low interest rates, and a surge of demand all combining to elevate the average automobile’s “value” by 22%. Cars outperformed the stock market, real estate, precious metals, luxury watches, collectable art, Legos, fine wine – you name it.

But now that all the factors that led to the inflation in value are reversing, used car prices are beginning to come down – everyone saw that one coming, that’s no surprise – but the entire used car financing market is thinly balanced like a house on stilts caught in a cyclone. It’s a disaster waiting to happen.

An Iowa Law Review found that over the last 10 years, car dealerships have begun making more profits from the financing of cars than the car sale itself. This transitioning from auto sales to loan sales has resulted in a loosely regulated, gray market industry, where lenders can easily issue sub-prime loans. And these are probably not in the best interest of the customer…

Regulation puts brakes on runaway markets – but unlike mortgages, student loans, credit cards and even payday loans, there is almost zero Federal oversight for automotive loans. It’s very easy to approve a loan that probably should not have been accepted, given that there’s incentive to sell as many loans as you can.

Don’t believe me? Well, a Jalopnik investigation in late 2021 found that 25%-50% of loans were given to customers who might not be able to afford them, and Lenders rarely verified income and employment of borrowers to confirm they had sufficient income to repay their loan. As many as 1 in 5 auto-loan borrowers admitted in a survey that their applications for debt contained inaccuracies, meaning fraud could be more pervasive than lenders planned for.

The bill is coming due – Almost 10% of auto loans extended to people with low credit scores were 30 or more days behind on payments at the end of last year. On top of that, it’s incredibly hard to get out of these payments now – with JP Morgan expecting used car prices to fall by as much as 20% in 2023. If the borrower can no longer afford payments as the loans increase to much higher than the car is worth, and this is repeated over and over for multiple borrowers, it’s a catastrophe waiting to happen.

Do you know anyone who’s paying unreasonably high car payments? Are you seeing the bubble pop around you? Let me know in the comments.

Here’s what you need to do to not get caught in this storm.

A six step plan to fight debt

Debt is a tough situation to be in. But it’s not undefeatable. Here’s a systematic plan to understand and get out of debt.

Find out exactly what kind of debt you have. Most people don’t have a clear idea of all the debts they have, and are surprised when it’s time to pay. Write down all your debts, including the balance and interest rate.

Track all of your spending over the next 30 days. Money that isn’t going towards paying off your debts better have a good reason behind it, and you won’t know it unless you consciously track the cumulative effects of your spending.

Cut everything you don’t absolutely have to spend money on. Delaying gratification is painful and it might sound extreme, but getting free of your debt will set a baseline level of happiness and calm that is absolutely worth it. That means – no TGI Fridays with buddies and no rewarding yourself with a Doordash delivery when you could pick it up yourself. Till the debt is done.

Consolidate your debts and lower your interest rate. If you have $20,000 in debt spread between 4 credit cards, with an average of a 20% interest rate – consolidate everything into one loan at a lower interest rate that you pay separately. Also, consider negotiating with your creditors for a lower payment or a different payment plan. They’d rather get something than nothing.

You could also look into a 0% interest credit card and transfer the balance to that card to save on the interest. If the transfer fee is small compared to your debts, it’s way cheaper than paying off a high interest debt.Use the “Dave Ramsey Debt Snowball” or Avalanche method – In the first case, you pay off your smallest balance first, and then slowly work your way up to the largest balance. This gives you a psychological boost and leaves more money to pay off larger debts later.

In the avalanche method, you arrange the debts by interest rate from highest to lowest, and pay off high interest rate loans first. The money that you save on high interest loans is put to better use in the long term to pay off other loans.Increase your income. Alright, that might sound obvious, but if all the other steps aren’t improving your situation, restructuring your finances will only help so much, and you’ll need to pick up a part time job or increase your income to bring in more money. It doesn’t matter how much you save if you don’t make enough.

Armed with that plan, and a systematic approach, I hope you are better equipped to deal with debt – and if someone you know is struggling with debt, share this with them and help them out! Getting rid of debt is the best gift you can give.

Even though household debt skyrocketed to the highest level since 2008, with an average balance of -$142,000, the good news is that most of that is simply from a historically low, fixed-rate mortgage. So it makes sense that debt is higher today than it has been, at almost any other point in history. However, credit card balances are getting higher to compensate for steeper prices. That is something to be concerned about, with many Americans flat out running out of money.

That’s why we should be incredibly cautious about our spending throughout this next year, evaluate whether or not you actually need to make each purchase, and determine if there’s a cheaper alternative that might save you more money. These are all just good habits to practice at any point but, with the market as volatile as it is, it’s worth it to cut back as needed, keep a consistent income and don’t take on more debt than you can reasonably pay off.

Stay safe, stay invested and I will see you next week – Graham Stephan.

Days of effort and research went into making this ten-minute read. If you found it insightful, please help me out by clicking the like button and sharing this article.

Great article with great benefits. For some it may seem that "A six step plan to fight debt" is a pack of already obvious steps, but most people continue to take loans, don’t think about interest at all and when the time comes, everyone shouts in one voice that they were deceived.

Really interesting and worth reading carefully