The Trump IRA: Free $1,000 vs your 401k

Should you take it or stick to your 401k?

It’s official.

President Trump recently signed an executive order that’s going to change how Americans save and think about investing for retirement. Seven months from now, this new policy, called the Trump IRA, will go into effect.

Depending on whom you ask, this is either one of the greatest investing opportunities in decades, or a financial disaster waiting to happen. Why?

Because it introduces a powerful alternative to the backbone of American retirements, the trusty 401k. It even features a $1,000 investment match if you qualify. That’s basically free money! But in the background, the conditions that safeguard the 401k are also being tweaked. To understand the impact of this shift, you need to look past the headlines.

Let’s break down the executive order, income thresholds, and whether you should take it. But before we dive in, join 40,000+ investors who get these updates directly in their inbox by subscribing for free:

You’ll never miss a notification, and you’ll be the first to know when something moves the market. Alright, let’s get started.

Why is the 401k broken now?

If you want to understand what the Trump IRA is trying to fix, you need to understand the ways in which it’s broken now. Everything in the American retirement landscape currently revolves around the traditional 401k. This is an employer-sponsored account, where a portion of every paycheck is contributed before taxes are taken out.

The math is simple: if you earn 100,000 dollars a year and contribute 10,000 dollars to your 401k, the IRS only taxes you on the remaining 90,000 dollars. This allows more of your money to stay invested and compound over decades. You eventually pay taxes only when you withdraw the funds in retirement. Many employers sweeten the deal by offering a match, where you get free money just for participating.

However, the 401k system is built on a massive assumption: that you have a traditional, full-time job. But in 2026, the reality is that 56 million people, including gig workers, freelancers, and employees at small businesses, do not have access to an employer-sponsored plan. These workers are effectively locked out of the primary wealth-building tool in the United States. While preparing for retirement is important, what’s even more vital is staying relevant in a market that’s changing faster than you can imagine.

If you spend any time on the Internet at all, you must have heard about Claude. It’s one of the most talked about tools on the internet right now, and I’ve dabbled with it myself. The tool offers incredible possibilities, and new models and features like Claude Cowork, Claude Design, Skills, and Connectors are launching literally every week.

But maybe you’re wondering where to start, and I get it, it can be a bit overwhelming.

Which is why you need to join the World’s first Claude-a-thon hosted by Outskill.

It’s a 2-day deep dive into Claude, its use-cases, and 10+ other AI tools. It’s this weekend from 10 am-7 pm EST — and they have just 1000 free seats for a limited time.

In the workshop, you’ll do deep research on Claude and use it to:

Build your own artifacts and dashboards

Create full presentations

Set up Claude Connectors like Indeed to automate your job search

And much more. Register now! (free for the next 48 hours)

Now let’s get back to securing your retirement.

What is TrumpIRA.gov?

On April 30, 2026, the administration signed the order to establish TrumpIRA.gov. The stated goal is to connect American workers who lack employer-sponsored plans with high-quality, low-cost IRAs offered by the private sector.

The website is intended to be a one-stop-shop where workers can compare funds, without being ripped off by the high fees tacked onto so many corporate plans. I’ll be honest, most employer-sponsored retirement plans are subpar. They often charge exorbitant management fees and offer generic funds, just because most people in charge do not take the 30 minutes of searching it needs to find better investments. High brokerage is the number one reason that people get low returns in the long run.

The Trump IRA standards are quite strict.

To be listed on the government site, financial institutions must cap their total fees at 0.15% or less per year. While this is still slightly higher than a standard Vanguard S&P 500 ETF, which might charge 0.03%, it is much lower than the 0.2% to 5% fees seen in many traditional 401k plans.

The $1,000 Savers Match: How it works

The most talked-about feature of this order though, is the Savers Match.

Starting in 2027, the federal government will deposit up to $1,000 per year directly into qualifying retirement accounts. This is a 50% match on the first $2,000 you contribute. (For married couples, it’s a $2,000 match for your first $4,000)

This is a guaranteed 50% return on your investment before your money even hits the market. However, the qualifications are very specific:

The full $1,000 match is available to single filers earning $20,500 or less.

The match phases out entirely once you cross the $35,500 threshold.

For married couples filing jointly, the full match is available up to $41,000 in household income, phasing out completely above $71,000.

This is a massive win for low-to-middle income earners, but even there, there is a logistical hurdle when it comes to actually receiving the money. The government match is expected to show up based on your tax return from the previous year. This means, to get your $1,000 in 2028, you must find the $2,000 to invest out-of-pocket in 2027. For someone living on $30,000 a year, saving $2,000 is a huge challenge.

The privatization of the 401k

Apart from this, there is another executive order in play that is causing concern among economists. Trump intends to expand 401k plans to incorporate alternative assets, including private equity, private credit, real estate, and cryptocurrency. Why?

The logic is that wealthy institutions and pension funds have used these assets for decades to generate massive returns, while retail investors have been limited to public index funds that historically earn less. By opening 401ks to invest in these other assets, the administration hopes to democratize wealth building.

But there’s a slight hitch. The existing options are “safe” and investors can mostly sleep easy. But for companies to invest in these more offbeat options, they have to tread with care. The Department of Labor has been directed to clarify how employers can offer these options without being sued for violating their fiduciary duty. In the past, workers have successfully sued employers for failing to do due diligence or offering high-fee, high-risk investments. Critics argue that this deregulation is essentially a payday for Wall Street, and they need to first prove that they can handle this safely.

Also, private investments aren’t as transparent as public ones.

Unlike the S&P 500, private investments are illiquid and difficult to value. Private equity often uses a 2 and 20 fee model: a 2% management fee and 20% of the profits. Over 30 years, those fees can destroy a retirement nest egg compared to a low-cost index fund. It’s true, sometimes the upside can be legendary, like Peter Thiel growing his IRA to 5 billion dollars. But the risk for the average worker is that these funds might be packaged into target-date products that look safe on the surface but carry high underlying risks.

What do you think? Should the 401k be expanded to include other investments, and what would you include in your own retirement portfolio?

The Math: Roth IRA vs. The Trump IRA

If you do not have a 401k, the Trump IRA is an excellent option to capture the $1,000 match. But there’s another option to consider: The Roth IRA.

In a Roth IRA, you contribute after-tax dollars. While you do not get a deduction today, your money grows tax-free, and your withdrawals in retirement are also tax-free.

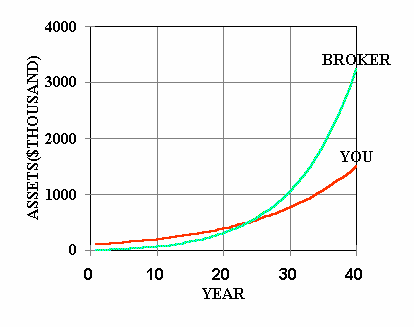

Consider this example: if you contribute $7,500 per year to a Roth IRA starting at age 20 and retire at age 65, assuming a standard 7% return, you would have approximately 2.5 million dollars tax-free!

Of that total, over 2 million dollars is pure profit that you owe nothing on. In a traditional 401k or Trump IRA, a similar balance might look higher on paper, perhaps 3 million dollars, but you would owe ordinary income taxes on the majority of that amount. If you are in a lower tax bracket today, the Roth IRA is arguably the better long-term play because you are locking in your tax rate now.

Final Verdict: Take the deal?

On paper, the Trump IRA is a net positive for the 50 million Americans who have been ignored by the current retirement system. Having a government-vetted portal that simplifies the process and caps fees at 0.15% removes the friction that prevents people from starting.

However, the income limits for the match are quite low. If you make more than $35,500 as a single person, you should probably focus on a Roth IRA or an ordinary brokerage account. If you make anything under that limit, the 50% match is free money that you should take.

The biggest win is not the match, but the simplification. Anything that makes it easier to open an account and start compounding is a win for the country. But if you’re practicing DIY investing, just be wary of the new alternative assets appearing in your 401k. While the promise of private equity returns and other assets is tempting, the fees and lack of transparency can be a trap for the unwary. Stay safe!

If you enjoyed this, hit that like button, restack this post, and share it with a friend to help them secure their retirement funds. It also really helps the newsletter grow.

See you next week!

— Graham

Are you sure about the income limit?

From Trumpaccounts.gov: “Get $1,000 for every American child born between January 1, 2025 and December 31, 2028.”

Sounds like Roth IRA is overall less of a headache than Trump account. Just my initial thoughts.