The U.S Debt Crisis

A ticking time bomb

What’s up you guys, it’s Graham here! If you want to join 12,900+ smart investors and never miss an update on the market, hit the subscribe button below. It only takes a second and it’s completely free.

“Blessed are the young, for they shall inherit the national debt.” - Herbert Hoover

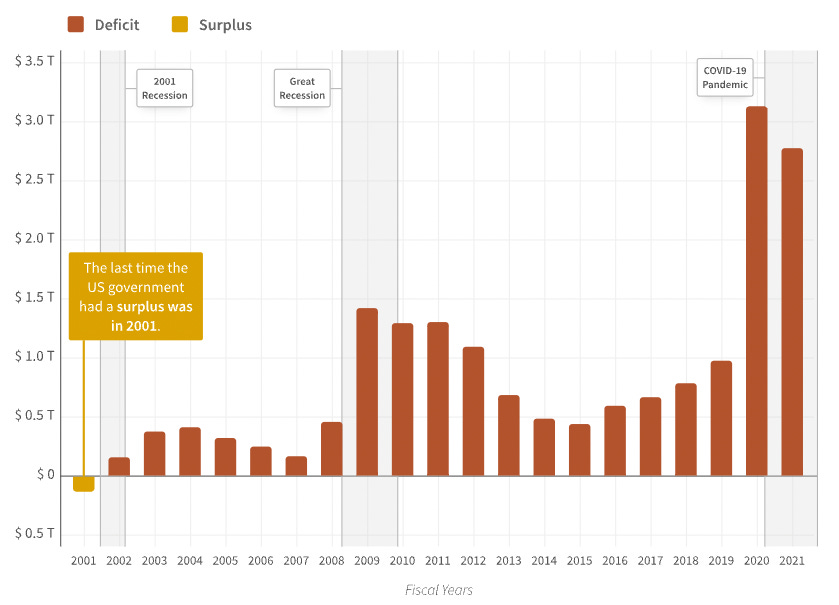

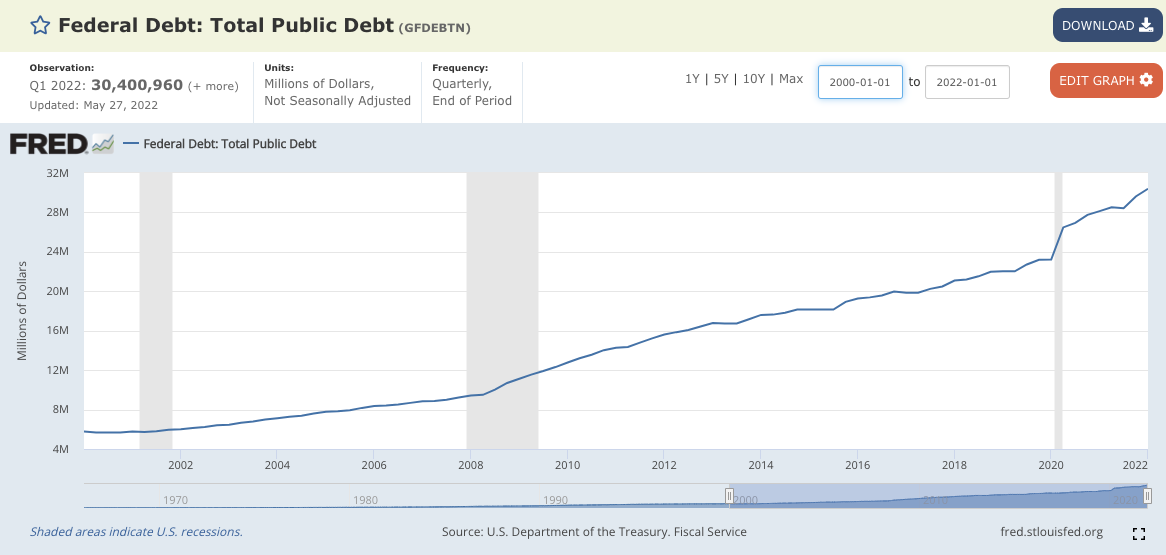

The United States has now amassed a staggering $30 Trillion of national debt. After all, for the last 20 years, the Federal Govt has been operating at a perpetual deficit where they spend more money than they take in.

I am shocked that more people aren’t talking about this because we are about to face the worst U.S debt crisis in history. So, in this week’s deep dive, let’s talk about the severity of what’s happening, why the U.S dollar continues to get expensive, the impact this is about to have on everyone, and most importantly, how you can protect your money and make more!

The National Debt

National debt refers to the total amount owed by the U.S - In the last 3 years alone, it has increased by a staggering 35%. If you are wondering why the world’s wealthiest country needs to have debt and whether we can’t just buy things with the money that we can afford, that’s not how the Govt and the modern financial system work.

See, the U.S at its core is kind of like a business - As with most growing businesses, you can afford to spend a little bit more than what you are bringing in by taking debt. This is in the hope that down the line, our growth will be so high that whatever loan we have taken now would become inconsequential.

Typically, these loans are taken by issuing bonds and treasury bills - which is just a fancy way of saying: The government will pay interest on the amount that they borrow, and it’s practically guaranteed to be repaid since the United States is seen as a really, really safe investment.

As to who owns this debt, the majority of the national debt is owned by the public itself which includes U.S banks, Pension Funds, Insurance Companies, individual investors, etc. (and no, contrary to popular belief, China only owns a minuscule amount of our debt)

The Problem

Up until now, the cost of maintaining the national debt was fairly affordable. When the interest rates were at record lows (Close to Zero for 2 years), the U.S was essentially able to borrow money for free and then let the power of inflation slowly reduce that amount over time.

It would be no different than borrowing money at 1% interest - and if inflation is 3%, by not paying off the debt you make a 2% profit. I explained this logic in detail in another article that’s a must-read.

With the Fed now trying to achieve a ‘Neutral Rate’ that matches the level of inflation, we could run into a bit of a problem. An economic downturn followed almost every instance of the fed matching interest rates with inflation. The only exception was in 1994 when we were in the middle of a productivity boom. All of this means that the only way to tame inflation now is with a severe recession shock.

IMF Managing Director Kristalina Georgieva has also warned us of a complete Global Debt Crisis as banks raise rates, debts cost more and all of sudden, other countries can’t afford to pay the cost of goods and services that we produce. This situation is known as

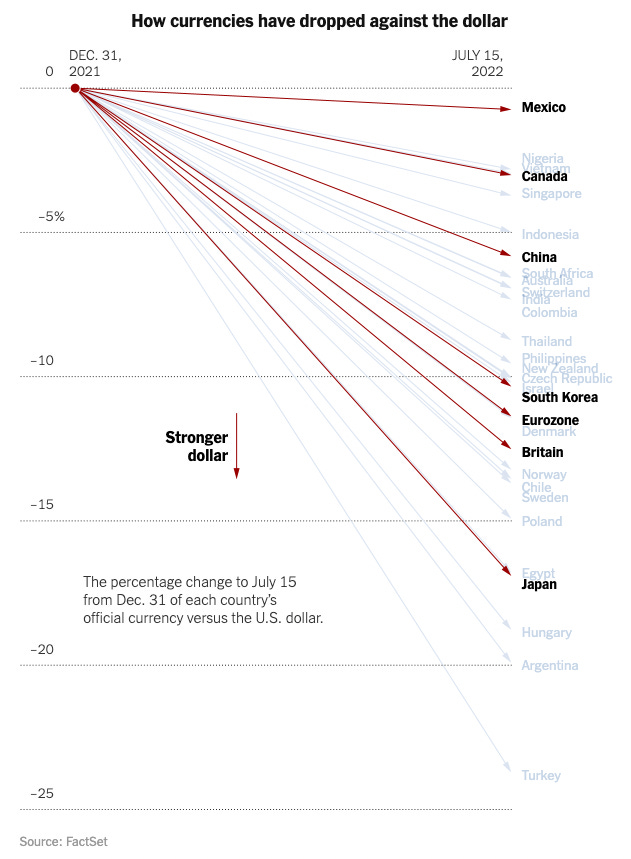

The Dollar Milkshake Theory

This is based on the fact that the US dollar serves as the reserve currency for the entire world. The gist of it is that every country trades in US dollars because of its stability, resiliency, and global acceptance - after all, imagine getting paid back in colorful Somalian coins and then having to figure out how to convert that back to your native currency!

However as other countries begin to slow down, their currencies decline in value relative to the U.S. This makes it more expensive to pay for goods and services in US dollars - Right at a time when they can least afford it. As the demand for the US dollar increases, other countries need to print more money to pay for those dollars. It’s called a “Milkshake Theory” because - in this scenario - the US would “suck up” more dollars from around the world, resulting in cascading defaults throughout every other large economy.

Since the beginning of 2022, this has been occurring and we can see that almost all the major currencies have fallen in value relative to the US dollar as more money is being converted from their native currency to USD.

The dollar is getting stronger while our economy is contracting and we are staring at a recession. This is happening now because we are increasing our interest rates faster than the rest of the world. When one country is paying more money, demand goes up, and thus our dollar becomes more valuable relative to everything else. Add to this the status of the U.S dollar as the ‘safe haven’ asset and everyone suddenly wants to park their cash in USD.

What all of this would mean to the average investor

If you are wondering what all of this would mean to an average investor like you, here is how it would affect you. Right now, both the U.S national debt and the public debt are at an all-time high.

Monthly car payments have just recently crossed an average of $700 per month.

55% of Credit card users are stuck paying an average interest rate of 17.3%.

The average student loan balance is sitting at just over $37,000.

People are borrowing more to pay for products and services that cost more due to inflation and if the economy enters a sharp and sudden recession, people might have a more difficult time paying down their debts.

This means, in the big picture, that there’s less money to spend and save for the average American, where a higher percentage of their income is spent towards paying off higher interest rate debt, accumulated during a time when everything was good.

As an armchair economist who talks in front of a camera all day, I will admit that the current situation is a very difficult one that’s not going to be solved anytime soon. Realistically, we are probably going to see an inflation reduction while the demand slows down and we are also going to see some marginal tax increase to bridge the gap between how much the United States bring in and how much they spend.

So, in terms of what to do practically, it’s best to stay away from any and all consumer debt, avoid variable interest rate loans like the plague, and always do your best to save at least 20% of your income. This should put you in a better position to weather any economic uncertainty and continue investing at a time when prices are lower.

Also, this would be the perfect time to diversify and spread out your investments as much as possible through index funds, international ETFs, Real Estate, Cash, Gold, etc. This way, no matter what happens, you will have something to fall back on and when you invest in the entire world’s economy, you are most likely to be in the best position to see stable and consistent returns, long term!

And force of habit - Smash that like button to help others find this newsletter. Hit that subscribe button if you haven’t done so already!

Love this insight. I’m an realtor and former financial advisor. It’s hard to always say what I think is going to happen when asked, and which way folks should turn, but you’ve summarized this nicely in this piece.

Seems somewhat inevitable that we are setting up our grandkids for a dystopia. Passing on the buck to the future it's never a great idea it could spell the decline of America. In many ways history will show this is the last decent generation of the American Empire.