6.5 Ways To Invest $10,000 in 2022

Getting more bang for your buck

How many millionaires do you know who have become wealthy by investing in savings accounts? I rest my case.” — Robert G. Allen

I recently found out that the average American household has nearly $10k saved in their bank account. This gave me the idea for covering the best ways to invest this money that are quick, reliable, and most importantly - profitable.

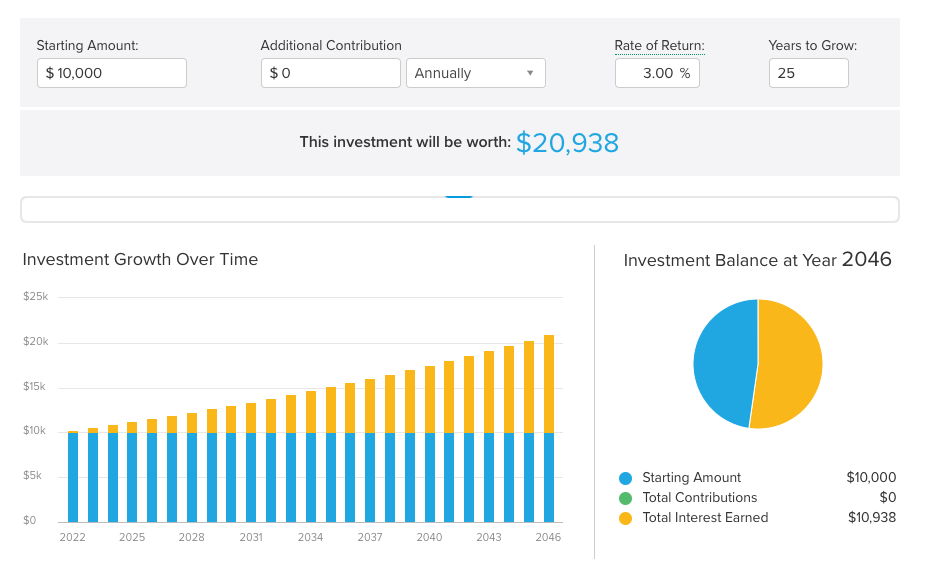

After all, keeping money in your savings account barely earns you any interest, and investing it correctly can end up making a significant difference long term. E.g, just getting a 3% return on your initial investment of $10k can double your portfolio in 25 years - without putting in any additional contribution.

I am pretty sure that if you read this article to the end, you can find at least one way to maximize your returns to get that extra 3% on your money. So, strap in while I cover the best possible ways to invest your money in 2022!

1. Start an emergency fund

First, we have to start with the most boring, basic, and safe option for your money - creating an emergency fund. For those unaware, an emergency fund is simply the money that you have to set aside to be used in the case of an emergency. Ideally, the size of the fund should be equal to 3-6 months of your living expenses and should be easily accessible, in cash, just in the small chance of you falling on hard times.

Obviously, you will be asking now, “But Graham, you just said you shouldn’t keep your money in cash or a checking account where it loses value to inflation every day.” My perspective is that having an emergency fund could actually end up saving you money and act as an insurance policy. E.g, in case you have an emergency, you wouldn’t have to sell your investments at a time when they have declined in value (Imagine selling stocks during the Mar’20 Covid crisis only for it to bounce back up 50% in the next few months) or even take on credit card debt to get over the hard times.

Personally, I have been using Ally Bank for my emergency fund because they pay a 0.5% interest rate and also have easy-to-reach customer service. There are a ton of other options that you can check out and see what fits your bill.

1.5 Short term savings fund

I will include step 1.5 here as well - Beyond your emergency fund, you could open up a short-term savings fund for the money that you plan to use in the next 1-4 years. Goals like saving up for a house, car, vacation, or business could fit in here because it is generally not a good idea to invest money that you know you will need in the next few years. There is always a chance that the market goes through a correction or even hits a recession right before you need the money.

As we can see from the above chart, your chances of making money in the market go up considerably with the holding period. That’s why holding cash isn’t always a bad thing and the small hit you take through inflation losses is well worth the peace of mind it provides!

2. Pay down high-interest debt

Another somewhat unexciting but really profitable way to invest $10k is to pay down high-interest debt. Even though this sounds boring, doing this could save you a lot of money in reality.

If you have any debt, whether it’s a credit card, mortgage, auto loan, or personal loan - that debt will cost you money. Of course, some debt is good to have like the mortgage I have which is tax-deductible.

But if you have high-interest debt that isn’t making you any money whatsoever (think credit card, auto loan, etc.), this debt needs to be paid down as soon as possible. My reasoning for this is simple - when you invest your money, on average, you expect around 6-12% return per year over a 10 to 20-year period. To get this return, you are taking a big risk by investing in the market. But, if you pay off a high interest (20%) credit card debt, you are guaranteed a 20% return on your money without taking any additional risk.

My thumb rule is that if you are paying above 5% interest on debt that isn’t attached to an income-generating asset, consider paying that off! You can view this as a guaranteed return on your money. Once you have done these two steps, let’s get into ways in which you can get exposure to the market.

3. Retirement Accounts

This is where the magic of compounding really begins. When it comes to retirement accounts, I will be going over three main options.

a. Roth IRA

Undoubtedly, my favorite retirement account is the Roth IRA. This is because all the profit you make in this account is tax-free by the time you retire (59.5 Years). It means that if you invest $1k when you were 20 and it’s worth $20k when you are cashing it out at 65, you would end up paying zero in taxes to Uncle Sam.

As of today, you are able to contribute up to $6k per year to Roth IRA if you are under the age of 50 or up to $7k per year if you are above 50. If you are eligible to do this, I would 1000% recommend you to do this like right now!! I personally regret not starting at 18 and you can learn from my mistakes. It could easily save you tens of thousands of dollars over the long run.

If you have $10k to invest, you can max out your Roth IRA (highly recommended) and still have money left over to invest in

b. 401K

This is kind of the opposite of a Roth IRA. Here you invest pre-tax money into the investment account and it’s only taxed once you begin withdrawing the money after the age of 59.5.

For example, if you invest $10k into a 401K, you will be taxed as though you made $10k less (In a 22% tax bracket, you will save a quick $2,200). This means that you can make more money work for you rather than paying it to Uncle Sam. Also, the contribution limit is currently $19.5k - so you can contribute more than $10k if you wish to.

Unfortunately, the catch here is that you will be taxed when you take the money out of your account down the line. So 401K only makes sense in a few scenarios.

401K match - This is when your employer matches whatever you are putting into the 401K account. Essentially this means that you are doubling your money immediately with zero risk whatsoever. The rule of thumb here is to always do this, no matter what.

Lower tax bracket in the future - Second, a 401K also makes sense if you are in a high tax bracket now but expect to be in a lower tax bracket in your retirement. You can profit from the difference in the tax brackets.

c. Health Savings Account (HSA)

HSA is one of the best options when it comes to investing your money. There are some qualifications to invest in HSA (which you can find from a quick Google search) but if you are qualified, you can contribute up to $3.5k per year, tax-free, into this account. The money in this account is used to pay for any out-of-pocket medical expenses you incur. If you don’t use it in one year, you can roll it over the next year and the year after that, and so on.

A lot of people believe that this is the best tax-advantaged account in the world. You don’t pay any tax on the money that you contribute into the account while also not paying tax when you take it out for any medical expense.

4. Index Funds

Assuming that you have already got your emergency fund covered, you don’t have any high-interest debts, and you have maxed out your retirement accounts - you can take a slightly more ambitious approach by investing it in Index Funds (Bet you didn’t see that coming, did ya :P).

For those who don’t know, an index fund is just an investment that encompasses the overall market, and by paying a small fee, you will get the benefits and diversification of owning a small amount of all the stocks in the market. Historically, an investment in a well-diversified index fund like the total stock market index fund, or an S&P 500 index fund has returned about 8-10% annually when you re-invest the dividends.

Even after being a full-time YouTuber who is well versed in the finance space, I acknowledge that I am not a stock market expert. I cannot buy and sell stocks that will consistently beat the market long term, nor do I have an interest in spending so much time watching stock charts and reading the news so I can make the proper decisions. So for me, I just prefer investing in an index fund - and this has been my go-to strategy since the very beginning.

For anyone who is looking for information on which specific index funds to invest in, you can start off with the famous Three-fund portfolio.

5. Individual Stocks

If you don’t mind taking a little more risk for a little more reward, you can use some of that $10k for investing in individual stocks. This is by far the riskiest strategy out of all the ones we have discussed till now. Here the risks are significantly higher but the payout could also be much larger. It’s because you are putting a significant portion of your money within a few specific companies and your portfolio performance depends on how those few companies perform.

I personally recommend doing this within a Roth IRA or 401K to avoid getting taxed on your profits, unless you are planning to hold on to it for a long time and make use of the sweet long-term capital gains rate. If your stock picking skills are on point, you can do significantly better than the market. For example, the S&P 500 is only up 8% YTD, but at the same time, Exxon Mobil is up 38%, and Lockheed Martin is up 30%.

However, just keep in mind that if you choose incorrectly, you could completely devastate your portfolio and that’s a risk you should be willing to take. Adding to this, the average investor is really really bad at doing this and can’t beat the market long term. So if you want to dabble in this, by all means, go for it- but just be realistic about your chances and the fact that you will have to put in serious work if you expect this to be successful.

6. Cryptocurrency

Finally, we come to the grandmaster of them all in terms of risk vs reward. Throughout the last decade, Bitcoin and Ethereum have broken records as some of the best-performing assets and they have surpassed just about every other investment in existence. There is always the potential that further adoption could drive the price up even higher.

Now in terms of investing $10k, it’s important not to throw the full amount to a random Discord pump and dump shitcoin and make your investment based on science and data. So here are some of the strategies that you can use to boost your chances of hitting it big in the crypto world.

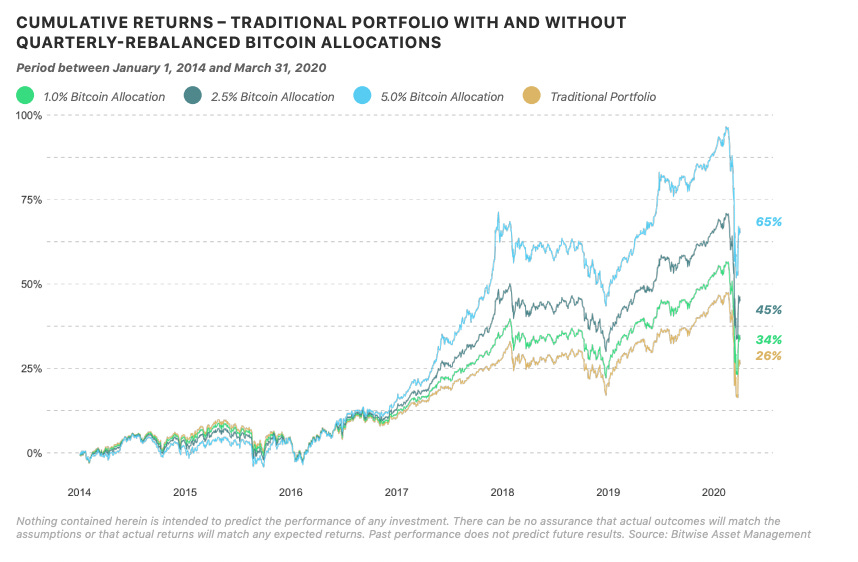

Based on previous data, the chances of you picking the next winning coin are very low (~2.5%). Instead of trying to pick the next winner, just allocating some part of your portfolio to Bitcoin and Ethereum would have easily given you market-beating returns. In fact, studies show that a 5% allocation to Bitcoin would have boosted the cumulative return of a traditional portfolio by a whopping 65% since 2014 despite the multiple sell-offs along the way. If you are more interested in having a consistent strategy, you can try following the Dollar Cost Averaging method for Crypto.

I personally invest around 8% of my entire net worth in a 50/50 split between Bitcoin and Ethereum - I am prepared for it to go to $0, but I am also optimistic enough to recognize that there’s enough potential in it to see what happens over the next 10-20 years.

So if you have $10k to invest and you have already built a solid financial foundation, you could throw some of that towards the top cryptocurrencies and see what happens.

So, those are my top ways to invest $10,000 in a way that’s realistic, easy to manage, and profitable. The final decision you should take totally depends on your risk tolerance, investment horizon, and your current financial situation. But, between these 6.5 options, you should be well on your way to turning that $10k into a lot more money in the future!

See you next week with another deep dive! Let me know in the comments section if I missed out on any big options - We are almost reaching 5,000 members in this community and we can provide each other a lot more value than I can do alone :)

If you enjoyed this piece, smash that like button and share it! Thank you.

Awesome Job Graham! Not sure if you're familiar with Canadian investment platforms and vehicles but would a TFSA be the equivalent to a ROTH IRA?

Also, what would you suggest if the company you work for doesn't do matched contributions?

What if you work for a fortune 200 company that offers an ESPP of 15%?