I am 4 Million Dollars in debt

And that's a good thing

One of the choices I get criticized for more than anything else is my use of debt and leverage - My loans on cars, rental properties, and my house add up to more than $4 Million. This is a number that I never thought I’d end up at! How did someone like me who advocates frugal living and careful spending reach this point? Am I in trouble?

No. In fact, debt is the key to my wealth. Though I do get some valid criticism for the way I handle debt, I still wouldn’t pay off any of my loans early and today you’ll see why. Let’s do a deep-dive to understand the types of debt, when it makes sense to take on debt and how you can use debt to make money. Let’s get started.

All debts are not equal

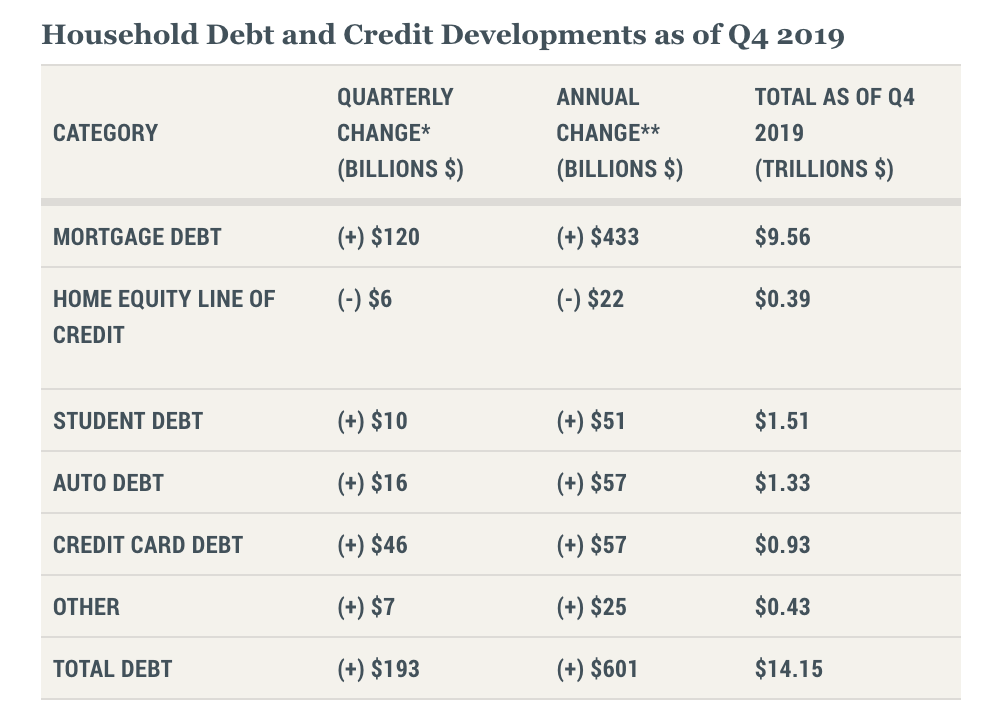

Debt has got a bad rap of late: Credit card balances increased to $860 billion in the last quarter of 2021, the largest increase in the 22-year history of the data. In fact, household debt of all types has been increasing, from auto loans to mortgages to student debt. To add to this, the rise of buy-now-pay-later services is seeing youngsters buying things that they cannot afford - 82% of users are in the age bracket of 25 to 34, but over 30% of users struggle with the monthly payments.

Credit card debt, student loans, and car loans are all high. With Fed rates increasing this becomes more of a problem. With such a gloomy picture, it does seem like debt is to be avoided at all costs. Right? Not really.

This is where we need to understand that debt is of two types: Consumer debt and debt taken on for acquiring assets. While the former is an expense, the latter is an investment, and managing it correctly will make you money! I have a rule of thumb for taking on debt:

If holding on to debt does not make you more money, then avoid it. But if it does make you money, then hold on to it sometimes.

If buying something does not make you more money, buy it outright. But if it does make you money, then finance it sometimes.

The important question here is: How do you identify the “sometimes”? To understand this, let’s see how loans are used to make money.

Profit off the margins

Options traders would be no strangers to the concept of leverage - Borrowing money to invest so that they can multiply their gains. The legends of Wallstreetbets are famous for YOLOing their life savings on borrowed money. But before you jump into the world of options, remember that investing with leverage is a double-edged sword: If your investment goes down, there is no cap on the downside. For this reason, leverage is safer with conservative investment options like real estate.

It might seem daunting to take on a loan of $4 Million at an interest rate of 3%. Over a span of 30 years, you would be repaying an amount of $6 Million. On the surface level, it might seem like a loss, but paying that extra 2 million over 30 years lets you invest the 4 million now to make a profit.

How do you figure out when it makes sense to take on debt? Let me give you an example: If I gave you a loan of $100k at an interest rate of 0%, would you take it? It’s a no-brainer. You could invest the money in any asset, repay the loan, and keep the profit. If the loan was offered at an interest rate of 1%, you could still invest it in the stock market to make a return of 4% - A profit of 3%.

But what if the interest rate was 4% instead? This is where it gets tricky. If you have some experience with real estate, you could invest in a property that would appreciate at 7% over time, and the 3% difference is your profit. But what if it gets higher? If the interest rate is 10% instead, then it doesn’t make sense to take the loan. There are almost no investment options that will safely guarantee a return of more than 10% and taking on that debt is playing with fire.

With that said, let’s take a look at my strategy for handling debt.

My debt strategy

I mentioned that I’m $4 Million in debt - But what if I told you that this debt is what is building me wealth?

First, I always pay my credit card debt in full every month so that I don’t have to pay any interest on it. This lets me get the best interest rates when I want to take a loan (check out my post on “How to get a perfect credit score” for more). Second, my loans are all towards investments rather than expenditures, as I mentioned above.

My current loans include:

A $30k loan on my Tesla Model 3

4 mortgages on 4 rental properties at 3% interest

1 mortgage on the house I live in, at a 2.875% interest rate

The cool thing is that while the properties are appreciating in value and also generating rental income, I get an additional tax write-off on them: The money that I earn goes towards paying off my loans and can be deducted as an expense, and I only have to pay a tax on the difference!

I fall in the 37% tax bracket and California has a state tax of 10%. The tax write-off is 3%. This means that though my interest rate is around 3%, the effective interest rate would be just 1.6% after writeoffs! And it doesn’t stop there.

Inflation is my friend

The rate of inflation has historically been about 2%, but in the recent past, it has shot up to 7.5% driving up the prices of all commodities. But there’s one good outcome. You get to pay off the expensive debt of the past with the cheap money of the present. Let me explain.

Every $1 Million of debt that I take on is reduced by $75k when the inflation is 7.5%. The rates at which I locked in my debt are much lower than what they would be due to inflation, so though my money has less purchasing power considering the current prices, my past debt is easier to pay off. This is also why it’s wiser to not pay off your loans when inflation is rising: If inflation is 7.5% and your interest rate is 1.6%, you make 5.9% returns by just not paying off your loan!

Another strategy you can use here is to get a Cash-out Refinance: This is when you close out your current mortgage to get a new mortgage for a higher amount. The difference between the two amounts is cash that you can invest for higher returns! This would also help you renegotiate your monthly mortgage payments to reduce the stress on your paycheck, so if you have a steady monthly income, using debt to beat inflation is a great option.

Debt in a nutshell

Even though debt is a great tool to have in your repertoire, there are a few things that you need to keep in mind:

Don’t borrow too much, and don’t take on more than you can handle.

Safe and predictable investments like real estate are better to hold debt against instead of lucrative investments that promise insane returns.

The interest rate should not be too high. The difference between the interest rate and returns from investing is what you get as profit.

Of course, there’s a reason that most people don’t take on debt. There’s the psychological factor that comes into play with loan repayments looming over your head, and it always feels safer to own something outright. But debt is like electricity - As long as you know how to control it, and don’t stick your finger in a socket, it just becomes another tool that you can use to build wealth.

Rationally speaking, if you are self-aware, persistent, and have the control to use debt wisely, it’s a superpower. But if you abuse it and take on more than you can handle, and get caught in the cycle of consumer debt, that’s when you get into trouble. Play it safe, start slow, and you’ll start seeing the advantages of using debt!

See you next week with another deep-dive!

If you enjoyed this piece, smash that like button and share it! Thank you.

I don't understand the statement "Every $1 Million of debt that I take on is reduced by $75k when the inflation is 7.5%.". Can you elaborate on this and maybe give an example?

how are you getting loans at such a low interest rate? Also would you recommend using a HELOC to start investing in real estate ( rental properties)