How to save for a home: Part 1

Why buy a house?

Welcome to the premium edition of Graham’s newsletter. Thank you so much for the overwhelming support. If you haven’t subscribed yet, today is the last day of the launch offer which gives you 25% off for life – make sure to check it out!

These courses are just one of the perks you will get as part of being a paid subscriber. Let me know what you think about the course in the comments below, and what other topics you would like me to cover.

This is a longer article than usual. Click here to read it on Substack and bookmark it.

I have always been an advocate of doing your research before going for any kind of purchase: be it a coffee or a car or a computer. It’s only a logical extension then to give a lot more thought to the most expensive purchase you will likely make. Buying a home is an integral part of the American dream, and there are some very good reasons for that. There are also arguments about why you should not buy a house, and rent instead – or that you should only buy it at the right time.

Either way, the decision to buy a house is not a simple one. Even if you decide to buy, the process of saving for a house can be a daunting task. There is a systematic way to go about it which maximizes the chances of you being able to afford your dream home instead of deciding driven by panic. 2023 is truly a turbulent time for the real estate market, and locking in a house now could be a risky choice – but that also makes it one of the best times to start saving up for a downpayment as you will be ready with cash on the sidelines when the market turns in your favor.

In this course, I’ll be sharing my research and insights obtained through years of experience as a real estate agent.

In part one, you will learn about the pros and cons of buying a house, when you should start saving for a house, and the decision between buying and renting.

In part two, you will learn about when taking on debt to buy a house makes sense, how to think about mortgages, and figuring out what house you can afford.

In part three, you will learn about what lenders look for, and the strategies you can use to save up for a downpayment.

Let’s get started with a first principles approach to understanding why buying a house is such a big recommendation on the path to building wealth.

The wealth equation

The way most people think about wealth is that it’s about hustling and grinding till you rake in a windfall amount that sets you up for life. Though that makes for an exciting story, statistically speaking, that’s not the most realistic situation. The odds of having a quantum leap in your income are very slim, and the sad part is that even if you do hit the jackpot, the chances of keeping it are very small if you are not mentally prepared for it.

But that doesn’t mean there isn’t a reliable way to build wealth. The shift you need to make in your mindset is that wealth is more of a process than a one-time goal, and the way to approach it is by understanding this equation:

Wealth = Income + Investment returns – Expenses

The equation itself is nothing profound. But depending on where you are in life, your focus will shift between different aspects:

At the start of your journey, income will have the most impact.

As you build more wealth, your focus will shift to maximizing investment returns.

But at every stage, your goal will be to earn more than your expenses.

The most sustainable way of building wealth is by building income streams or investments that automatically take care of your expenses. When I first started building a passive stream of income on YouTube, the mindset I had was “If I make x amount of money, that will take care of my power bill. This takes care of my rent,” and so on. Another way to flip this around is to just eliminate expenses if possible.

Of course, that’s easier said than done – You can replace your Starbucks coffee with a 20-cent Bankroll coffee. You can cancel your Netflix subscription. But necessities like power, gas, and food can neither be replaced nor eliminated. This is where housing is a curious case where you can structure expenses in a better way even if you can’t do away with them. Buying a house might not be a great deal in the short term, but over the long run, it could save you a lot of money compared to renting. Let’s see when it makes sense to buy vs rent, and how you should judge the deal.

The housing solution: Why buy a house

Assuming that AI doesn’t take over and upload all of us into computers, you’ll always have to live somewhere. Housing is by far the biggest expense on anyone’s budget. Nothing comes close. Here are some stats:

The lowest rent in the United States is in Springfield, Missouri, at $662/month.

The highest rent in the United States is in New York costing $3,260/month!

On average, American households spend $21,409 per year on housing costs, which makes up 25.8% of total average earnings.

40% of renters pay rent which is 35% or more of their monthly income.

Rents have been going up over the last 80 years (without adjusting for inflation).

Housing is one of those essential requirements that can guzzle away your income. That’s one of the biggest arguments for buying a house. In the long run, not owning a house and renting forever can cost a bomb in terms of the amount you spend – not to mention the uncertainty it brings to your living costs. So it’s more a question of when to buy a house rather than if you should buy a house at all.

Another argument in favor of owning a house is that it forces you to build equity in an asset: For the majority of Americans – not just the wealthy ones – a house was the biggest component of their net worth. And as people get older, this percentage increases. 70% of US homeowners were 45 years or older in 2023, and they had a net worth 40x higher than that of renters – at $225k to $6,300. So investing smartly in a home could make all the difference.

There is also the potential for profit when the value of your house appreciates, because historically speaking house values have steadily appreciated over time, especially over the last decade or so. But this is not a certainty, and there are reasons why your house isn’t an investment quite in the same way as other assets. The situation is different if you are buying a house for rental income or to flip it, but this course is specifically about buying a home to live in (though I might talk about other scenarios in future courses). But there are other, intangible reasons that make buying a house worth it.

A home provides stability – if you’re looking to settle down and/or raise a family, this is a boon as it saves you the stress of having to renegotiate rent every year. Locking in a mortgage at a fixed rate gives you a clear understanding of how much housing will cost, and it lets you plan ahead. If you are relatively settled in your career and are unlikely to change jobs, finding a place close to your office will also sort out the commute situation. This is more likely to happen as your career trajectory progresses, which is one of the reasons that 70% of US homeowners are 45 years or older.

It’s also psychologically much easier to “buy and hold” a house as compared to many other assets. Unlike stocks, bonds, and cryptocurrency, the value of your house isn’t quoted to you every day and it’s a “real” asset which has some intrinsic value. The memories and emotional investment that go into a home also give it sentimental value and make it easier to hold on to.

But before you make up your mind about buying a house, let’s hear the other side out. There are some people who had a radically different take on the matter.

The opportunity cost: Why not to buy

Buying a house is a big life decision because it involves committing a sizeable amount of money and many years of your life to it – some choose not to make it till they’re ready. One curious case of this is Warren Buffett, of all people. Buffett moved back to Omaha at the age of 25 with his wife and kids in 1955, with $127,000 to his name. The median home prices at that time were quite low and he could have bought a house fully in cash, with less than 10-20% of his net worth for the guarantee of stability. Rather, he chose to rent a house for $175, telling his wife: “I’d be glad to buy a house, but that’s like a carpenter selling his toolkit.” This was even before he decided to start his first partnership – Buffett considered himself retired and counted solely on compound interest to do his job for him.

Three years later, he did buy a house. But the kicker is that even this decision to buy a house was not optimal from a financial standpoint. He bought the house for $32,000 in 1958 and it is currently worth $650,000. But if he had just invested the same amount in the S&P 500, it would have grown to $18 Million – and if he had invested it in his own portfolio, hold your breath, it would be worth more than $6.6 Billion.

Of course, Warren Buffett is not the best example. This is not a recommendation for Warren Buffet to have rented into his nineties – but it does highlight an important point: Capital that is allocated to one cause cannot be invested elsewhere. Committing to buying a house has a huge opportunity cost.

This has much more relevance if you are younger. Earnings growth is decided in the first ten years of your career to a large extent – it takes a lot of effort to be in the top 5% or top 1% of your field, but if you get there, the rewards are disproportionately more. When you are young, one of the best ways to build wealth is to increase your income and that means investing in yourself. That could be in the form of learning new skills, travelling to network, investing in your business, or otherwise. Locking away capital in a house severely restricts your ability to do that.

On the contrary, if you rent in your younger years, you can downsize – or move to a different city to chase opportunities. The stability of income does matter, but it’s not as critical as when you have a family to take care of. Add a mortgage on top of that and it could get even more stressful if you don’t have a stable income. You should think about buying a house only when you are reasonably sure that you have the cash flow and buffer to back it up.

It’s also a good time now to talk about why your home is technically not an asset.

You cannot sell the home you live in without finding an alternative place. So you will have to transfer some of the wealth to the new house (and people mostly upgrade and lose profits), or you will have to start renting again.

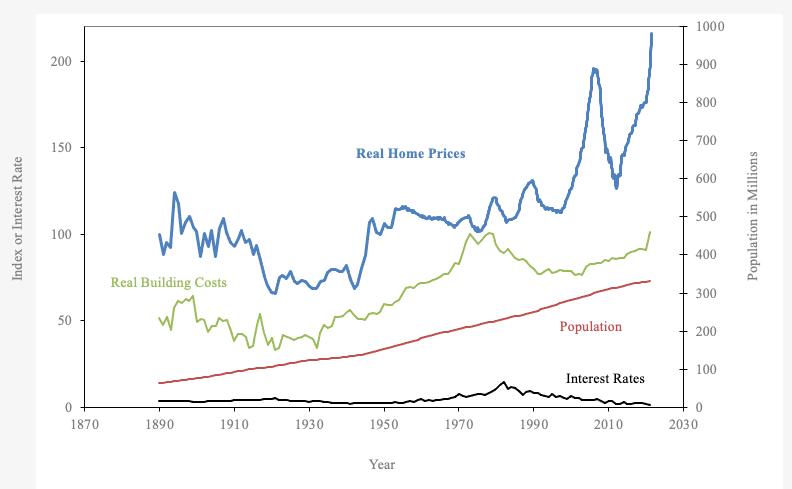

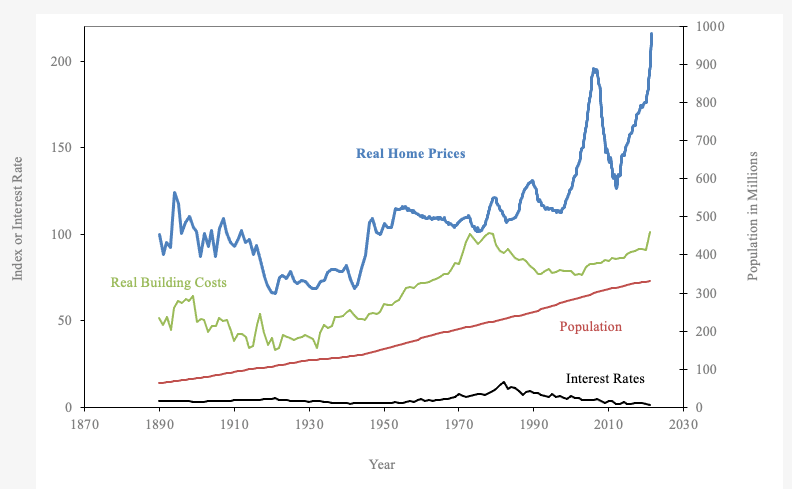

Homes appreciate in value generally but this trend has been quite recent. Home prices have been appreciating consistently for maybe the last 40 to 50 years, but according to Shiller and Case who have collected housing data since 1890, housing prices stayed nearly flat for about 100 years till they began to grow. Across the same period, the stock market has had phenomenal returns (reinvesting dividends).

Source: US Home Prices from 1890 to 2015, Robert Shiller It’s easier to hold a house through a market crash compared to stocks, but that doesn’t mean it’s free of stressful periods. There have been a number of crashes as is evident from the chart above, most noticeably in 2008-10.

{kind=link}

Yes, it does provide stability and you can fall back on it during tough times, but the lock-in period for a house is much longer to break even than other assets. Buying a house is probably not something to do for short-term profit. It’s not a reliable strategy and a huge portion of your net worth would susceptible to the whims of the market. If you can foresee big expenses coming up soon or don’t have an emergency fund that can last you 6 months, committing to a house is probably not wise.

Finally, there’s the elephant in the room: Buying vs renting. Which is better?

Buying vs Renting

You might have heard of houses taking a minimum of seven to ten years to break even. Have you wondered why? Why can’t you just buy a house with a loan and sell it before the term of the loan ends, as opposed to renting a house, even over the short term? Well, there’s a very good reason. As Morgan Housel says,

The price of a thing is not the same as the cost of a thing.

Nowhere is this more applicable than when it comes to buying a house. On the face of it, every house has a price that you need to pay to acquire it – but the cost of the house includes everything that comes with owning the house. This includes property taxes, escrow charges, maintenance costs, utilities, and a bunch of other things that a tenant will never have to take care of. These costs are the reason that you can never break even immediately after buying a house.

Buying and renting both have pros and cons:

Buying a house is a long-term solution that gives you more stability and control – and also more work. Renting a house gives you more freedom and mobility – but also uncertainty about the future. That’s the trade-off you have to make. It’s a highly personal choice.

But if we were to look at it purely in terms of the numbers, buying a house probably wins in the long-term. Buying a house has the opportunity cost of not investing the down-payment and real cost of maintenance, etc. but you also get tax write-offs and appreciation. It takes approximately 7 years for this bargain to be realized (depending on market conditions).

If you’re interested in the detailed calculations, here is my complete breakdown of the cost of renting vs the cost of buying.

One thing to note here is that buying a house isn’t a magical solution to eliminate housing costs from your balance sheet. Shelter is going to cost money no matter what, and your decision will depend on your career and life situation and the timeline you have in mind.

In the long run though, if you do plan to settle down in one spot for at least 7-10 years, buying a house could be the better option, and it makes sense in the long run as well. Having said all that, here’s a checklist you can use for handy reference:

Checklist – When to buy a house?

Answer each of these with a yes or no:

You have a solid portfolio with a lot of cash, and are looking to diversify your assets into something that has intrinsic value.

You have stable income for the foreseeable future and a buffer for uncertain times.

You know where you are going to settle down, for a reasonable amount of time.

You are looking to start a family and/or want some stability.

You are planning to get into real estate as a serious investment opportunity and want to learn more about the process by buying your first home as a launchpad.

You have paid off all high-interest debt.

You have a good credit score and prospects of getting a good loan, and know what kind of house you can afford.

You have saved up a sizeable amount for a down-payment.

If you have a positive answer for most of these, you can start thinking about buying a house. If you can only tick a few off this list, you have some work to do. Don’t worry! That’s what this course is all about. We will be diving deeper into how you can save for a house and better your prospects.

Points 7 and 8 in the checklist are especially important. In the upcoming part 2 of the course, we will talk about using debt properly and improving your financial health. In the final part, we will cover what lenders look for and strategies you can use to systematically save for your dream home.

See you next week! – Graham Stephan

Are you saving up for a house? Have you saved up for a house in the past? What questions/insights do you have about the process? Let me know in the comments and I will address them in upcoming issues.

Disclaimer: This is not financial advice. This information is intended to supplement your knowledge in the field of investing and personal finance. Please do your own research carefully.