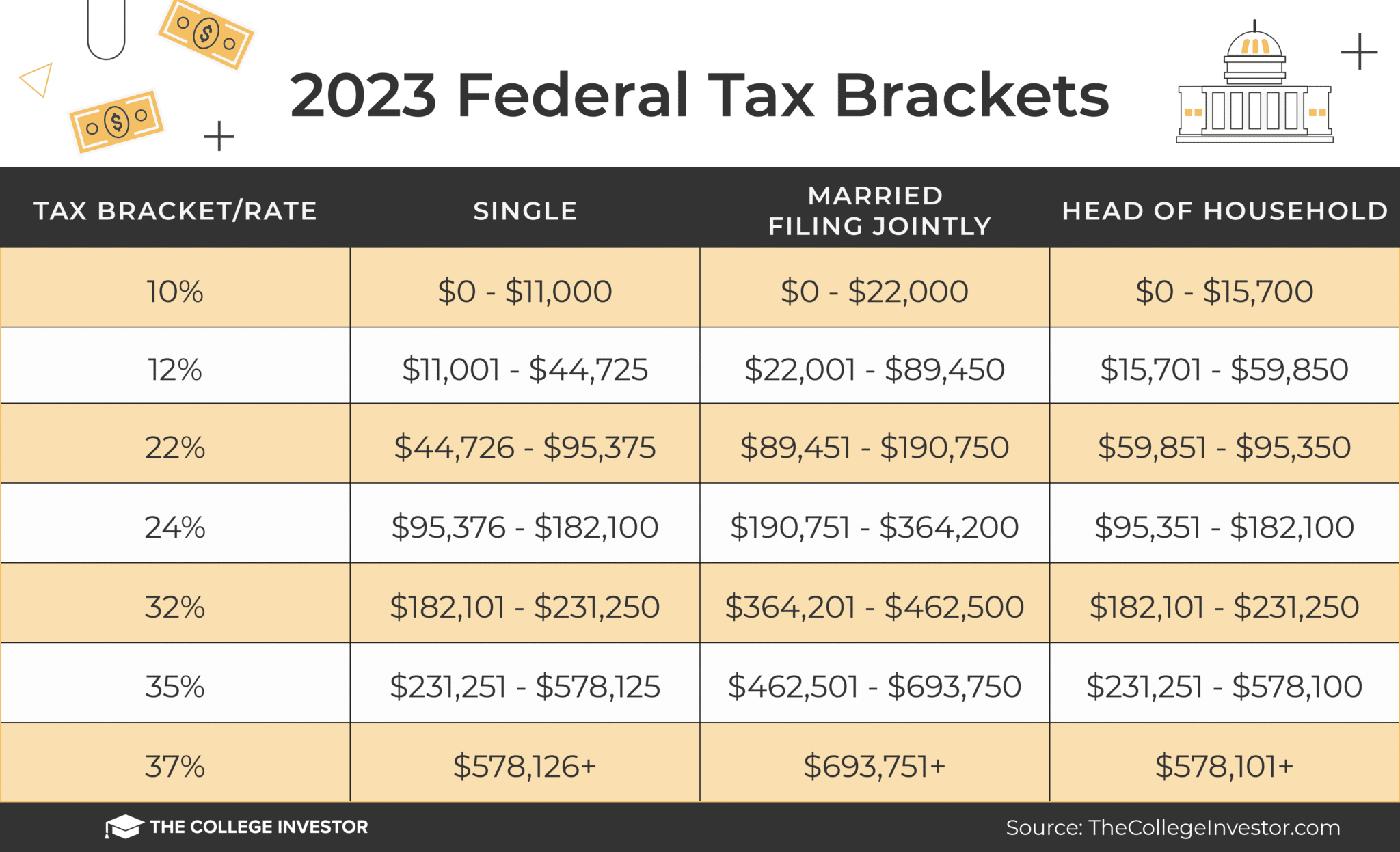

Tax Boomerang

Tax Boomerang

A divided housing market – and unintended consequences

What’s up guys, it’s Graham here :-) If it’s your first time here, hit the subscribe button below to join 38,300+ smart investors and never miss an update on the market again.

And now we have a PREMIUM plan with extra content every week: Part 2 of the course on “How to save up for a house” will be out tomorrow. Subscribe to access this and more!

Goodhart’s law: Every measure which becomes a target becomes a bad measure.

In 1991, a new tax was introduced in the United States: The “Luxury Tax.” The idea was simple. The wealthy could afford to pay more tax than the others, and hence they would pay a 10% tax on cars valued above $30,000, boats above $100,000, jewelry and furs above $10,000, and private planes above $250,000. Senators Ted Kennedy and George Mitchell were visibly hopeful about the tax revenue that this would bring in.

There was just one problem – The tax didn’t work. The tax revenue that year missed its mark by $97 Million. There was no incentive for the wealthy to buy luxury goods when they were being heavily taxed. On top of that, the people who actually suffered were the ones who manufactured the luxury goods, i.e small businesses and working-class people. The hardest hit were Maine and Massachusetts, the home states of Senators Kennedy and Mitchell, with a 77% drop in Yacht sales. Boat builders estimated layoffs at 25,000. By 1993, almost all the tax laws had been repealed.

The road to hell is paved with good intentions. One of the reasons it’s so hard to fix pervasive problems in our society is that policy discussions start with the intention in mind, with little attempt to understand the human incentives and second-order consequences of the decisions that people will make in response to the policy. On paper, taxing the rich seems like an honorable idea. But it assumes that the behavior of the players will remain the same once the policy is brought into action – but people react to changing rules, and the policy hurts the people it was supposed to help.

What’s happening now in the Californian housing market is a direct result of misguided policy – and the effects are rippling across the country, dividing the housing market into two. Here’s what you need to know about the new tax laws, which markets are up, which markets are down, and what you can do to save money.

The California Exodus

Beginning April 1st, Los Angeles residents will be subject to a 4.5-5% mansion tax that applies to all properties sold over $5 million, as opposed to the 0.45% transfer tax already in place. This tax is expected to completely destroy the high-end property market throughout the entire state, potentially resulting in even more people leaving. As usual, the intention behind the tax is noble – Measure ULA was established to fund affordable housing and provide resources to the homeless. But what it could end up doing is completely different.

Now, for those who are unaware – homelessness is a serious issue throughout California. More than half of all unsheltered people in the country live in the state, and more than $10 Billion has been spent from 2018 to 2021 trying to solve the issue. But while California is set to become the 4th largest economy in the world, the number of those living on the streets is rising.

The expectation is that a 4 to 5.5% transfer tax will raise $672 Million for affordable housing. This isn’t restricted to Los Angeles: San Francisco has a tax rate of 6% over $25 Million, San Jose imposed a 1.5% tax on transfers over $10 Million, and Culver City now has a tax of 4% above that amount. The problem is that like in the case of the luxury tax, the impact of this tax is not being considered – the wealthy are being considered static players, while the reality is that if it’s unfavorable to live in the state any more due to high taxes, they have the highest incentive to move.

California’s top 1% currently pay more than half of the state’s income tax. Lately, a lot of them are leaving. In San Francisco, for instance, 39,000 people left, taking $10.6 Billion of income with them. That’s a huge problem, even according to the CEO of the California Taxpayers Association who said that “The top 5 percent of income earners pay 70 percent of the personal income tax. Even if a few of those taxpayers rethink California as a place to live, that does have an impact on the (state) budget.”

The naming of this tax as the “Mansion Tax” is a misnomer that is likely to make you think of A-list athletes, actors, and hedge fund managers — in reality, this is mainly going to affect construction of multi-family and commercial buildings. A 5% tax equates to more than half of a builder’s profit margin. This now takes away incentive for investors to add housing supply, and businesses will be less inclined to expand. This gives a reason for people to leave and turns into a chain reaction.

On top of this, the new tax would apply to the entirety of the sale consideration, not just the excess amount beyond the $5 million threshold, regardless of whether the property is sold at a gain or a loss. No tax system works like this – this is equivalent to the IRS taxing anyone above a certain income level on their whole income.

The impact of this is that it’s addressing the symptoms of the homelessness crisis, without actually addressing the root cause, which is a lack of accountability in government spending and neglect of real issues like addiction and mental health care. Now that this has triggered an exodus of people out of California, we’re seeing something that hasn’t been ever recorded in the history of the American Housing Market…

A divided market

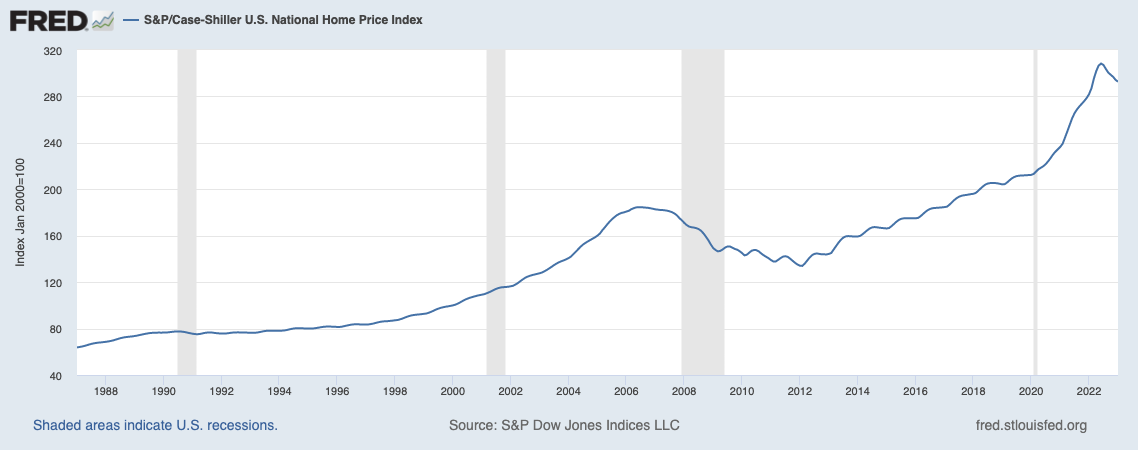

For the first time ever, the housing market is going through a split: National home prices are both crashing and surging at the exact same time, depending on where you live. On a broad scale, prices are indeed coming down – The Case-Shiller index found that prices are already 5% lower than they were back in June 2022, and this marks something very rare: Prices are officially lower Year-over-Year.

The last time this occurred was in 2012, just after the Great Financial Crisis. But before you panic, the reason for the fall this time isn’t a broken housing market or even higher interest rates which seem like the obvious culprit, but instead: More inventory. Fewer sellers are listing their homes, but the ones who do are facing more competition because the old listings are still on the market. These are piling up and creating an increase in supply, and the only place for prices to go is down. Even though new listings in March were nearly 30% below pre-pandemic levels, inventory has increased 59.9% compared to last year. But that’s still dramatically lower than what we’ve seen in the past – and some areas might continue to go higher in price.

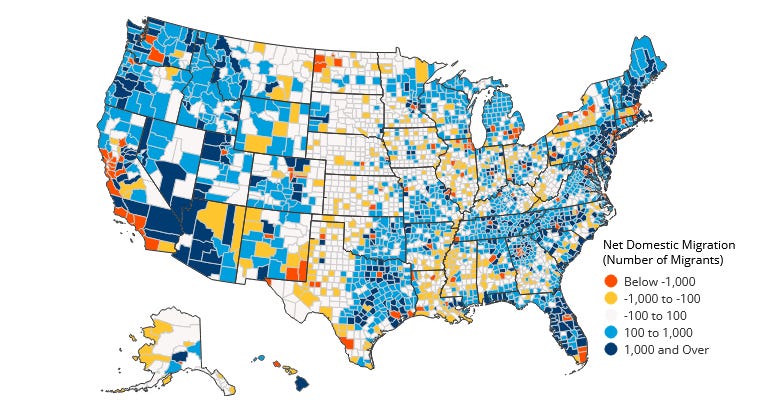

This has cut the housing market right down the middle, as Black Knight Research pointed out, with the West Coast seeing a 10% drop and the East Coast seeing a 10% gain. In terms of specific states, home prices:

Fell 7.5% in Seattle.

Fell 10.3% in San Francisco.

Rose by 12% in Miami.

Rose by 9.3% in Orlando.

Why is this happening? The rate hikes might have had a part to play here, but the main reason is the extraordinary increase in home values in the West Coast last year. The areas with the highest prices have more room to fall and the rate hikes affected the employment of tech professionals in the West – this led to migration towards better prospects and more affordable housing in the East, which is causing prices to rise in those areas

{kind=link}

And of course, as we saw, the taxes in California are even more of a reason to leave: But speaking of taxes, there are some new proposed measures that could have a direct implication for you…

Taxes, taxes, taxes

And that’s the brand new proposal to raise income taxes. With the National debt approaching nearly $32 Trillion and rates at a new high, the US is beginning to pay a lot more in interest – $1 Trillion per year, to be precise – and that’s a problem. Well, the good news is that there’s a plan to cut the deficit by over $3 Trillion in the next 10 years. The bad news is, the money is probably coming from you.

According to the new proposal, the corporate tax would go from 21% to 28%, raising $1.3 Trillion. This is still lower than the 35% tax established before the 2017 Tax Cuts and Jobs Act, but it would ensure that companies “pay their fair share”. But a Tax Foundation Analysis estimated that at this rate, the GDP would potentially reduce by 0.7% (about $160 Billion), and stock and wages would marginally decline. Approximately 138,000 full time jobs would be lost. Thankfully, this loss would be gradual but the GDP decline of $720 Billion over the next 10 years would be larger than the tax revenue generated. As a result, they believe that over the long term, a higher corporate tax would result in incomes dropping by 1.5%-2% and would be harmful for growth.

The alternative suggestion is to tax “consumption” and a “recurring tax on immovable property”, i.e higher real estate taxes. As far as I’m concerned, a 28% corporate tax is not the best way to raise revenue, but hey, it could be a lot worse, like this next idea:

Which is: A minimum income tax on the top 0.01% that would generate $436.61 billion. This would encompass a 25% tax on American Households worth more than $100 Million, which is more than triple the 8% tax rate paid by the wealthiest right now. The problem is – this would tax unrealized capital gains for the first time ever, and that opens a Pandora’s box of troubles.

Imagine you invest $1000 and it grows to $5000 over time. As long as you don’t lock in the profits, you technically don’t have it as cash on hand – but by taxing unrealized gains, you would have to pay a tax on the $4000 profit. And to do so, you would have to sell some of your stock. Everyone reading this article probably has unrealized gains, either in stocks, a home that has appreciated in value, or a stake in a business. Right now, that value is just on paper, and you don’t have to pay tax on it till you lock in your profits. But if this law comes into effect, then it would be chaos.

Right now, this is being proposed only for the ultra-wealthy, but it sets a precedent that could be expanded to every citizen down the line. This whole plan is based on the idea that the top 0.01% are paying “only 8% tax” which is true only if you look at their net worth on paper – though they actually pay 50% of their $200,000 income in cash to the IRS. On a practical level, taxing unrealized capital gains is going to be an impossible task. The Supreme Court ruled earlier that there must be some actual transfer of rights before the Congress can tax appreciation as income, according to the 16th Amendment. On top of that, it would be a massive waste of resources for everyone involved.

But there are a few other plans that do stand a chance of passing:

Increasing the 3.8% Affordable Care Act Tax to 5% on Americans earning more than $400,000. They would close the loophole which allows individuals to bypass this tax using an LLC.

The top tax bracket would be increased from 37% to 39.6% (where it was pre-2017). This is the most likely to pass.

The stock buyback tax would be quadrupled from 1% to 4%. Stock buybacks are controversial, but in the absence of other good investment opportunities, I think they can be a good use of capital.

What is your take on these taxes? Which taxes do you think are unfair, and what would you propose instead?

The Fair Tax

On top of all this, there’s a really weird idea that stretches the idea of “fair” – this proposal suggests that income taxes slow economic growth and hamper productivity. So their solution would be to tax consumption rather than income.

Instead of paying 20-50% on all your income, you would pay a “flat” 30% sales tax on all items that you purchase. Of course, if you’re living paycheck to paycheck, this would be a nightmare – this is the equivalent of 30% inflation overnight. Well, they thought of that, and their solution is to send out “rebates” that can cover the additional sales tax for lower-income individuals. What might end up happening is that high-income individuals who spend less get rewarded, and everyone else ends up paying a lot more… Discouraging consumption, reducing economic activity, and impacting the very people it was meant to help. Oh well.

But even for this tax to be effective, a 2004 study found that the rate would have to be at least 60% if the current income tax was replaced with a sales tax. Any lower, and the national debt would climb higher, and the whole point of enacting this tax would be moot. As much as I’m open to the idea of something like this, I’m perplexed: The chances of this passing are almost zero, so why would anyone even consider this an option?

As far as all this is concerned, I think that this emphasizes something that has been echoed for centuries, that the only certainties in life are death and taxes. The stress of trying to manage your wealth in a way to minimize taxes and optimize the right number is a hassle. In my opinion, you could focus on minimizing taxes on the biggest line items on your budget – like housing – and make life decisions based only on those key factors. Trying to plan for every other uncertainty is stressful.

Regardless of that, one of the best ways to save on taxes is to invest regularly, build appreciating assets, and think long-term.

Stay safe, stay invested, and I’ll see you next time – Graham Stephan.

Hours of effort and research went into making this ten-minute read. If you found it insightful, please help me out by clicking the like button and sharing this article.