What’s up you guys, it’s Graham here! If you want to join 17,800+ smart investors and never miss an update on the market, hit the subscribe button below. It only takes a second and it’s completely free.

Some time ago, I came across a very interesting study conducted by Stanford University, popularly known as the ‘Marshmallow Test’. The premise is simple, a child is put alone in a room with a single marshmallow and then told that they are free to eat the marshmallow, but if they waited 15 minutes without eating it, they would get a second marshmallow as a reward. 40 years later, the children who waited the whole 15 minutes had significantly better life outcomes such as better SAT scores, better social skills, and higher income.

The Marshmallow test is the first thing that came to my mind when I read the headline that 30% of Americans who earn more than $250,000 a year are living paycheck to paycheck. Despite how inflation has raised the price of pretty much everything, $250,000 a year is simply too much money to live paycheck to paycheck, pretty much anywhere in the United States. A compounding factor here is many of us did not receive any sort of financial education from the schooling system, which resulted in nearly 43% of Americans being financially illiterate.

Now I also understand that for some of us, the numbers simply do not add up. Wage growth has not held up with consumer prices for quite some time now and rent and college expenses have gone through the roof recently. Despite all this, receiving some form of financial education can help pretty much everyone. Saving and investing money early in life will substantially improve your chances of early retirement and this week, I take a look at how you can avoid impulsive and unnecessary purchases and instead direct that towards your savings account.

Before we jump in,

The Largest Wealth Transfer | How to Prepare

Let’s face it, spending is a psychologically gratifying activity; there is a reason ‘retail therapy’ is a buzzword in pop culture. A key factor of unnecessary spending is impulse purchases; the average American spends an extra $314 per month on spur-of-the-moment expenses.

In this video, I detail a few techniques you can use to avoid impulse purchases.

Buy it tomorrow - If you have decided to pull the trigger on an impulse buy, wait for a few days. Research shows that the dopamine hit comes from the anticipation of purchase and not the purchase itself.

Not spending is earning - When you are considering an expensive purchase, ask yourself this: would you rather have the item or its cash value paid to you, tax-free, right now? If that changes your mind regarding the purchase, immediately transfer that amount to a savings account.

Hourly rate - For every purchase, do this mental calculation. How many hours will it take me to pay for this? For example, you’d see a $100 dinner bill a lot differently, when you realize that it would take nearly half a day of work to pay it off on a $30 hourly rate (~$24 after taxes).

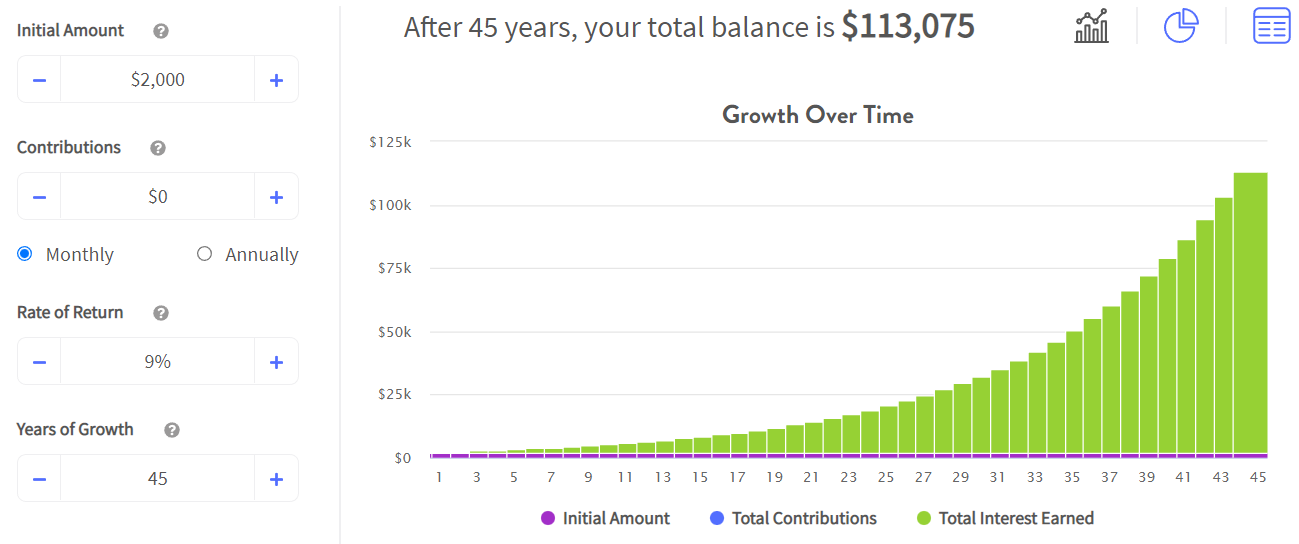

Compound interest - Finally, to avoid impulse expenses, visualize how much money it will become in the future, if you invest it. You might be hesitant to skip that $2000 vacation when you are 20, but if you invest that in the S&P 500 (~9% returns), it would grow to nearly $100,000 by the time you retire at 65!

I also go into more detail about the psychology of spending and how you can take control of your expenses, so make sure you watch this one!

China is About to Cause a Global Recession

Right now, we are dependent on the globalized economy more than ever. In 2021, the United States imported goods amounting to nearly $2.83 Trillion; nearly 1.5 times the GDP of Texas. An increasingly globalized world has allowed companies to generate a competitive advantage by splitting the manufacturing process across countries, thus making products cheaper and creating more profit. For example, it is estimated that an iPhone made completely here in the United States would cost around ~$2000. However, the flip side of globalized trade is that we are more susceptible to global issues than ever and an economic downturn in one country can cause ripple effects throughout the world.

As of now, the global situation is incredibly complex with the Russia-Ukraine war affecting gas prices, and inflation wreaking havoc in Europe. Further, China, which manufactures 20% of the items we use on a day-to-day basis is going through an economic slowdown. In particular, I focus on the issues in China, where their zero covid policy and crumbling real estate market are slowing production. I also detail the effects these global issues can cause back home and how you can prepare for this, so let me know if you liked this!

Sidenote

The S&P 500 is nearly 20 percent down from its all-time high and at the cusp of a bear market. Even stocks like Google and Microsoft are trading at >25% off their peaks. What stock are you eyeing right now? Let me know in the comments!

I have a recommendation…

Check out the GRIT Capital newsletter.

GRIT is the #1 FREE finance newsletter on Substack – talking stocks, crypto and investing. Run by a former $100MM portfolio manager Genevieve Roch-Decter. Her mission is to democratize access to stock market insights to the masses through her platform GRIT. She has +400,000 followers on social media and writes a daily newsletter to +65,000 investors - including hedge funds, billionaires, investment advisors and retail investors.

This week, Genevieve writes about quantitative tightening which hit full stride this week. What does it mean and how does it affect markets? Is it a big deal or no problem? Subscribe to read more!

So that’s it for my Sunday round-up. For the new folks here, in this newsletter, I give a quick recap of whatever you may have missed over the week on Sunday, and on Wednesday, I will be doing my deep-dive article on one of these topics.

See you next week with another bunch of exciting videos!

And force of habit - Smash that like button to help others find this newsletter.

Financials… specifically PNC bank. The stock is currently ($157), significantly below its true value of (180~200) during last spring when it had acquired BBVA, making PNC the fifth largest bank in the US with coast-to-coast locations with a reinforced balance sheet. I believe at least a small position in this stock should yield a good return in the long run when interest rates normalize and financials regain some lost ground. Fingers crossed 🤞🏻

GRWG