Second-order thinking

Always one step ahead

What’s up guys, it’s Graham here :-) If you want to join 31,900+ smart investors and never miss an update on the market, hit the subscribe button below. It only takes a second and is completely free.

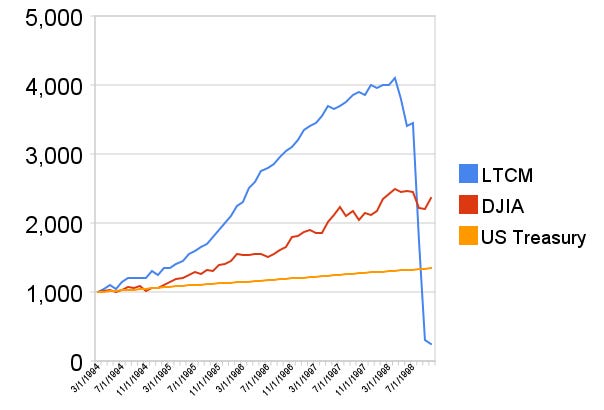

Long Term Capital Management was the hottest name on Wall Street in the late 90s. Started by the former head of bond trading at Salomon Brothers and two future Nobel Prize Winners, the Hedge Fund had a universal stamp of approval. LTCM was able to raise hundreds of millions of dollars from high-net-worth individuals, banks, and private university endowments based on the caliber of its top brass, and amassed over $1 billion by the time it began trading in 1994.

LTCM did not disappoint in its first few years. They returned more than 40% when the S&P 500 was averaging 21%. The problem with high expectations is that they are extremely difficult to exceed. LTCM was using two dangerous weapons: High leverage, and a model of risk called Value-at-Risk (VaR). VaR estimated the maximum risk faced by each investment, and because they knew the exact risk faced by each investment, LTCM’s executives thought they could afford to take on a lot more risk. By 1997, LTCM’s returns were dropping and to compensate, they turned to the Asian and Russian markets armed with their VaR models.

There was a problem: The VaR models estimated the risk of each investment individually, but they did not foresee a situation where all the investments would fall together. In 1998, LTCM started posting losses for the first time. Since they were leveraged 250-to-1 (!), they started getting margin-called and had to start selling off their assets at very unfavorable prices. This reduced their value further, and when they turned to institutions for funds, nobody was ready to risk the long-shot. As LTCM’s value dropped, it became less credit-worthy, and its value dropped further. Here’s how 1000 dollars invested in LTCM would have fared:

By the end of 1998, it was worth almost nothing. But LTCM was “too-big-to-fail”. Many huge financial institutions were invested in it. Its failure would have sent the economic system into shock, and finally, the Federal Reserve organized a bailout with $3.6 Billion worth of funds from various institutions. How did some of the smartest minds in finance and economics orchestrate a disaster like this?

The math was definitely off, but there was a more fundamental reason: They were only thinking one step into the future. They estimated the risks one at a time, but they didn’t think about the panic that would ensue if all the risks materialized together. They didn’t consider how a loss in their value combined with leverage would trigger a chain reaction and cause the fund to implode.

This is where second-order thinking is required. According to Nassim Taleb, every action has a consequence, and every consequence has another consequence, and it’s necessary to always think about these second-order consequences. The stock market, the real estate market, the labor market are all at a turning point. There’s even a possibility that recession might never materialize – Let’s see how you can think two steps ahead and see what others are missing, to prepare for the times ahead.

No recession?

There’s one topic that everyone from market analysts to Twitterati have been talking about since last year – the slowdown of the economy, the “Federal Reserve Tightening” and the US Government scaling back on stimulus – ultimately leading to the possibility of a recession. The stock market for one has definitely reflected these fears.

On June 13th 2022, the stock market dropped by 20% from its peak and entered a bear market. Tech stocks were hurt even more, falling by more than 35%, and homes in the Bay Area were selling for 30% less than a year ago. Michael Burry even posted a warning drawing a parallel between the current market rally and the dead-cat bounce in 2001.

But despite all the warnings, there’s a possibility that the recession might not happen after all. The technical definition of a recession is two quarters of negative GDP growth, which already came to pass in mid-2022. But the GDP isn’t always a true indicator of the overall economy. The National Bureau of Economic Research updated the definition of a recession to include “a significant decline in economic activity that can last a few months to more than a year”, and that’s usually accompanied with lower employment, production, and sales, tracked on a monthly basis rather than quarterly.

The committee also gives more weightage to payroll employment and personal income less transfers. In the last 44 years, the committee have never once had to reverse or rescind their declaration regarding any recession, so they only announce one when they are sure. The catch is that there is an average lag time of 7.3 months between the time a recession takes place and the time it’s actually announced…

Tech Layoffs

Let’s do some independent research here: To back the committee’s point, GDP growth in the last quarter of 2022 actually bounced back to 2.9%, breaking the trend earlier. Why was there a decline in the previous two quarters? Well, due to supply chain issues and tax reasons, businesses stockpiled resources in advance making their revenue look bad on paper – but the job market is still strong.

Now, that claim might seem strange, given that Google, Amazon, and Meta have laid off more than 40,000 people recently. But exploring the possible reason for this, it could just be that they hired more than required at a time when cash was cheap and now they are cutting costs. An alternative measure of unemployment that gives a clearer picture is – how many people are out of work currently but likely to be called back or find jobs quickly? It turns out, it’s a healthy number. So the industry might be just restructuring itself and the jobless rate isn’t signalling an impending recession.

In addition, the layoffs in other sectors isn’t as much, and it’s only the Tech industry that might have been adversely affected by the Fed reeling in the free money hose. But the other factor in determing a recession is: Consumer personal income. That’s looking a little worrisome.

Cash crunch

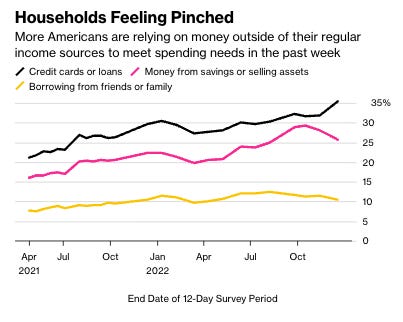

At a time when inflation is still relatively high, credit card usage is still very high. If consumers are able to draw on credit for discretionary expenses, is the economy as dire as it looks? Well, the reason for the credit is a little worrying: 35% of American households are drawing upon their credit line to meet household expenses. Close to 40% of households are struggling to meet usual expenses and 82% of all households think that the situation is going to get worse!

What’s even more concerning is the timing of it all – Credit card rates are averaging around 19.1% and the last time they were so high was in July 1991. The trend shows that rates are still on the ascendant. This could be the beginning of a credit crisis where consumers borrow to pay off the expenses of the previous month, but the interest keeps piling on at progressively increasing rates till the lifeline turns toxic. It’s very difficult to spot this when you’re in the middle of one, because it escalates slowly – but if you can relate to this, there are a few ways to think ahead and stop the problem in its tracks:

Try to pay off your credit card debt in full rather than pay the minimum amount as escalating rates keep adding interest to your due amount.

Prioritize paying off high-interest debt in the beginning.

Deposit spare cash into a high-yield savings account or money market account to offset some of the leakage.

Restructure your spending and focus on solving the root of the problem rather than resorting to more credit which is a band-aid fix.

These steps are easier said than done, but it’s all about directional thinking. Focusing on minimizing debt would lead to low stress in the future, whereas depending on a credit line is a temporary solution that can cascade very fast.

Killing the golden goose

Despite the consumer credit situation, consumers’ net worth is now $145 trillion, up from a pre-pandemic $115 trillion, while average housing prices are still $70,000 higher than they used to be. Therefore, the risk of a recession doesn’t seem immediate and the Fed can safely continue raising rates longer than the market expects until inflation subsides. But there is another area where short-term thinking is threatening to have long-term implications.

While real-estate values have been turbulent, it’s no surprise that rent values have been going up, with median prices crossing $2,000 a few months back – which was their highest level in history. The response? A new proposal from the White House is gaining momentum called “The Renters’ Bill of Rights.” Under this, The Federal Housing Finance Agency would examine limits on rent increases, enforce actions aginst price-gouging, and prevent tenants from being unfairly denied access to housing.

Essentially, this would aim to place a ceiling on how much rent could be raised and many cities are already following suit. Colorado, for example, issued a bill that would allow cities to implement their own rent control, if they desire. California expanded a state-wide rent control in 2020, and members of congress have also expressed interest in extending this throughout the rest of the country. But, the real question is: does it work?

While the intention seems benevolent, this is a classic case of first order thinking. There are very few things that economists can agree on, but a 1992 poll found that 93% of economists agreed on one thing – A ceiling on rents reduces the quality and quantity of housing. The reason is simple. The rise in rental prices is not a sudden inflation in greed, it’s a reflection of low inventory, causing high demand. If there is a ceiling on rentals, the incentive to provide quality housing and raise inventory reduces even further! On top of this:

Rent-controlled tenants are 20% more likely to stay in their unit, reducing inventory further.

Landlords repurpose buildings to avoid rent-control or sell them, reducing housing inventory by 15%. In San Fransisco, for instance… it was found that most older rent-controlled properties were converted into condominiums, and were typically sold to wealthier residents – thereby continuing to make the housing shortage even worse.

Reduction in inventory drives up rental prices further – or, capping the prices reduces incentive to build any new houses, worsening the inventory issue.

The net result is that rent control ends up making the situation worse by restricting the supply of new units into the market. The renters for whom the law is intended rarely get access to rent-controlled prices, and the lack of new supply makes it more difficult for them to find affordable housing.

This is another classic example of a band-aid fix, without attacking the root cause of the problem.

Coming back to the recession question: What we’re seeing now isn’t a typical situation which we can slot into a bucket and neatly label as a recession or not, and by the time we know whether it’s a recession or not, it wouldn’t be a factor of interest any more! The more sensible approach is to look at the individual factors that are affected by a recession and pay closer attention to those.

Are you concerned about the market? Then you should study the market in isolation as recessions generally have very little correlation with the stock market. If the housing market is your concern, then pay closer attention to Fed rates and state regulations before making a long-term commitment. If you find yourself relying on credit more than usual, think about where this is headed long-term and correct course. Always think a step ahead and find a structural solution – and when the tide turns, you’ll be prepared for it.

What trend were you one step ahead of that others took time to catch on to? Let me know in the comments!

Stay safe, stay invested and I will see you next week – Graham Stephan.

A lot of effort and research went into making this article, so if you found it insightful, please help me out by clicking the like button and sharing this article.

One major problem is that if we *don't* have a recession that creates slack in the labor market, any uptick in the economy will spark renewed inflation. While economic activity has dropped off a bit the labor market is still VERY tight. The "balanced" rate of weekly unemployment claims needed to keep tightness from getting worse is 250-275k, we're recently been between 180K & 200K. 300K/week would be an ideal rate as It would gradually allow the unemployment rate to rise to 4% over a period of months. This rate, combined with a dropping inflation rate would even allow the Fed to *slowly* pivot (say 25bp every other meeting) next year.

Great story - I learned something new per usual. Wow - that is a lot of leverage.

If gov can control rent, second order thinking says they can make the case to control the price of eggs, and we know where price control of food leads us to....