The Fed changes course

Oil shocks, a strange housing market, and Bitcoin as a hedge

We need to talk.

The dream of a soft landing just hit a wall of reality. A few days ago, the Federal Reserve officially announced that they will not be lowering interest rates for the foreseeable future. But just a few months ago, almost every analyst was predicting the exact opposite – in fact, the question was how fast rates would be cut, not whether they would be cut. The impending rate cuts made the market bullish, and investors were expecting the S&P 500 to skyrocket.

But we’ve seen this in 2001, and we’ve seen this in 2008 – when every expert agrees that things can only go up, that is usually when they start to fall.

Jerome Powell has been walking more tightropes than a professional trapeze artist over the last few years. In 2022, I wrote about the tight balancing act he needed to perform to save the economy from stagflation:

It looked like he pulled that off creditably. But with just months to go before his replacement steps in, he needs to do the impossible again.

We are currently entering what I call the Deadlock of 2026. The Fed is essentially trapped. On one hand, the job market is starting to soften and personal savings are declining, which usually means the economy needs lower rates to keep moving. But on the other hand, we have a major problem that is making rate cuts impossible right now. That problem is the boogeyman of the economy: gas prices.

Let’s understand how gas prices are setting off a domino effect impacting everything else, and then let’s see what options you have as an investor.

Before we move on – 39,000+ investors get these market updates in their inbox for free. Join them by clicking this button:

The Chain Reaction of 100 Dollar Oil

Oil is the lifeblood of the economy. It might sound dramatic to put it like that, but the more oil costs, the more expensive everything else becomes. Your groceries, your Amazon packages, the fertilizer used to grow your food, and the planes you fly on all rely on oil. Trucks run on diesel, ships run on fuel, and manufacturing uses massive amounts of energy. When a commodity is used at that scale, even a small tipping of the needle can affect everything else.

According to Federal Reserve research, a 10 percent increase in the price of oil raises the energy CPI by about 1.5 percent almost immediately. This creates a nasty chain reaction:

Businesses see their margins squeezed, so they raise prices to stay profitable.

Consumers then have to spend more on essentials, leaving them with less money for everything else.

As this cycle continues, inflation returns and the Fed loses control of the narrative.

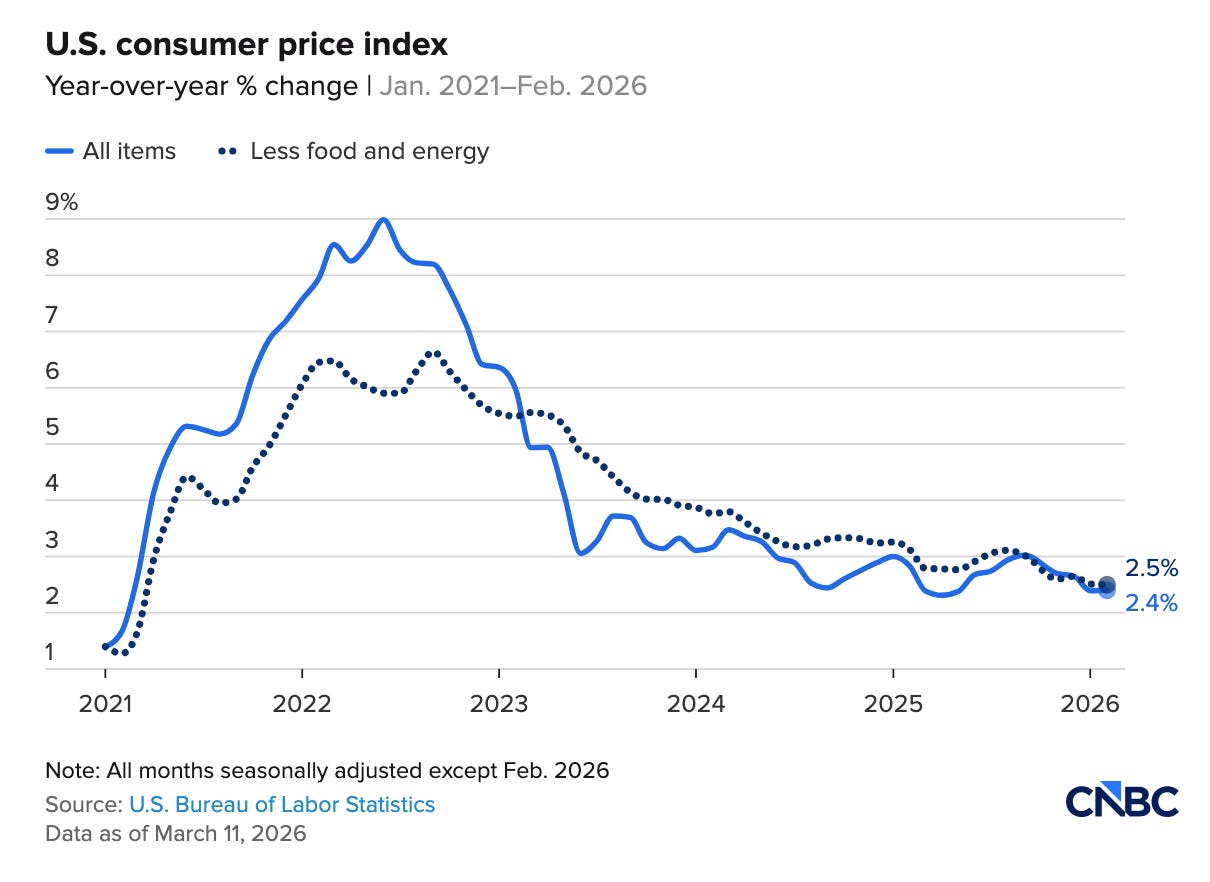

The biggest concern right now is that the inflation report for February came in at 2.4 percent. On the surface, that looks fine. But that number measured a time before oil prices saw their largest increase since 2022. If oil stays above 100 dollars a barrel, we could see inflation hit 3.5 percent much faster than people expect.

We have already seen the national average for a gallon of gas jump 10 percent in just seven days. If this trend holds, analysts warn we could face an energy crunch three times as severe as the 1970s oil embargo. You can read more about those gas price pressures here. Meanwhile, sustained inflation would affect something else that affects all of us…

The housing market is flatlining

Since inflation is refusing to go away, interest rates have to stay high. And when rates stay high, the housing market enters a stalemate.

Something very strange is happening right now. Affordability is at its worst level ever on record, yet prices are not crashing. Instead, they are just stopping. JP Morgan recently released a report suggesting that home price appreciation will stall at 0 percent for the rest of 2026.

Basically, here’s what’s happening. More inventory is finally hitting the market, but demand has dropped so much that prices have nowhere to go but sideways. Since 2022, the number of single family homes on the market has more than doubled. This gives buyers a lot more room to negotiate, but most people are still priced out because mortgage rates are sitting above 6 percent.

We are now in the most balanced housing market in almost a decade. This means neither the buyer nor the seller has the upper hand. Sellers who locked in a 3 percent rate in 2021 are refusing to sell unless they get a high price, while buyers are refusing to pay those prices because their monthly payments would be astronomical. Zillow is even forecasting less than a 1 percent price increase through 2027.

For most people, renting is actually the cheaper option in the short term. Unless we see a wave of forced selling, do not expect a massive drop anytime soon. We are likely looking at a long, slow flatline.

Bitcoin as the New Chaos Hedge

While the traditional markets are struggling with this deadlock, Bitcoin is doing something very unexpected. It is starting to act as a hedge against the very uncertainty that is killing the stock market. Even though Bitcoin has fallen 50 percent from its peak, it has actually outperformed gold and the S&P 500 over the last month.

Let’s look at the technical data: Bitcoin futures have been negative for 14 consecutive days, which is the longest streak since 2022. Historically, when sentiment gets this negative, it usually coincides with a market bottom. We are also seeing long term holders stop selling, which suggests that the people who have been around for years are not panicking. Long term HODLers see the instability in the dollar and the energy markets, and they are choosing to diversify into an asset that the Fed cannot print.

Bitcoin is starting to decouple from the Nasdaq. It is becoming a tool for people who want to protect themselves from a global economy that feels increasingly fragile. While I always say to be careful with volatile assets, the fact that Bitcoin is showing stability while oil is surging is a signal we cannot ignore.

Do you invest in Bitcoin? What other alternative assets are you using to hedge your portfolio?

The Drama Inside the Federal Reserve

To make matters even more complicated, the Fed is currently dealing with a ton of political drama.

Jerome Powell has been under fire from President Trump, being called “stupid” and a “numbskull” for going against his mandate. Recently, a Federal judge had to step in and quash criminal subpoenas against Powell. The judge basically said the government was trying to harass Powell into lowering rates or resigning so they could replace him with someone more compliant.

This resistance is a huge signal because it confirms that the Fed is trying to remain independent despite massive political pressure. Powell is scheduled to be replaced in May by Kevin Warsh, but that confirmation is currently being blocked in the Senate. This leadership vacuum means we are probably not going to see any rate cuts until the new chair is settled (or the economy completely collapses, which fingers crossed, doesn’t happen). The Fed’s own projections now only show one rate cut for the entirety of 2026, which is a far cry from the three or four cuts people were betting on earlier this year. You can see the summary of economic projections here.

The Game Plan for the Next Few Months

So, what does all of this mean for you? It is easy to look at the rising gas prices, the stagnant housing market, and the Fed drama and want to pull all your money out. But historically, that is the worst thing you can do. Uncertainty is part of the game. Eventually, the overseas conflicts will resolve, oil prices will stabilize, and the market will catch up to the new reality.

I am personally not changing my strategy. If anything, I am being a little more aggressive as the market falls. I have been investing more into international index funds and Bitcoin ETFs lately because they have been beaten down by this uncertainty.

History shows that the best days in the market often come right after the worst ones. If you try to time the bottom, you usually just end up missing the recovery.

The goal is not to bet everything on one outcome, but rather to build flexibility. I am still a huge believer in the boring, long term approach of dollar cost averaging into total market index funds. Consistency is the only thing that works through every cycle, whether it is COVID, interest rate hikes, or energy crises. Stick to the plan, keep your expenses low, and remember that in a few decades, these few weeks of uncertainty will just be a tiny blip on a chart.

If you found this breakdown helpful, it would mean a lot if you shared this with someone who is worried about the economy. I will keep an eye on the data as it comes in and keep you updated.

If you found this breakdown helpful, please like this post and restack it. It helps the newsletter grow tremendously. Share it with a friend who needs to see this:

I will be monitoring the situation daily and giving you updates. See you next week!

–– Graham

Thanks Graham… the stability in your outlook and investment approach is comforting at times like this…