What’s up guys, it’s Graham here :-) If you want to join 32,200+ smart investors and never miss an update on the market, hit the subscribe button below. It only takes a second and is completely free.

There’s a parable I like a lot about interpreting impactful events.

A farmer lived in a village with his only son, and all they had was a horse. One day, the farmer woke up to find that the horse had run away. The villagers rued the farmer’s bad luck, but he shrugged and said “Good luck, bad luck, who knows?”A few days later, the farmer’s horse returned – but it brought a herd of wild horses along with it, multiplying the farmer’s wealth multiple times in just a few days! When his neighbors congratulated him, he again shrugged and said “Good luck, bad luck, who knows?”

The next day, the farmer’s son was trying to tame one of the wild horses, when it bucked him off and fractured his leg. It looked like he would be bedridden for a long time, just as harvest season was around the corner. The neighbors offered their condolences, but sure enough, you know what the farmer replied with: “Good luck, bad luck, who knows?”

As the village was preparing for the harvest, a horde of barbarians plundered the city in a surprise attack. All the young men in the city took to arms in an attempt to drive away the bandits. But being untrained villagers, nine out of ten men who fought were killed. The old farmer and his injured son were spared. The villagers marveled at the timing of the son’s injury and the farmer just said “Good luck, bad luck, who knows?”

I love this story because it shows the futility of trying to predict how things will turn out in advance. As humans, we have a hunger for stories and we fixate on events and opinions and interpretations – but events just play a small part in the systems that they are a part of. The consequences of an event might appear damaging in the present, but they might set things right. And short-term fixes might undermine structures that provide lasting stability.

A perfect example of this is the Fed’s attempt to curb inflation with rate hikes. Let’s see what the turnaround in inflation means, where the Fed is likely to go from here, and what it means for your money.

Ceasefire

After months of consistent raise hikes, the Fed reduced its rate hike to 25 basis points last week – signaling that even higher increases could soon be coming to an end. Of course, this was no surprise, because the market already seems to have priced it in. But there are mixed opinions on where things go from here.

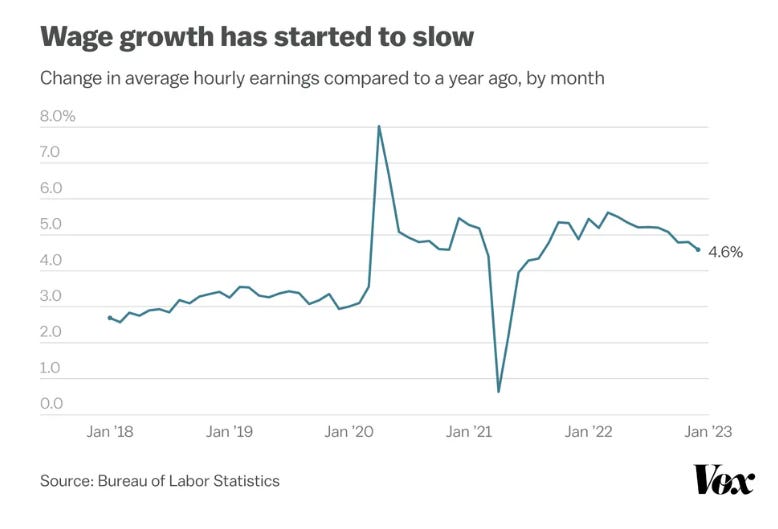

On the surface, these seem like really hard times. Mass layoffs are already putting downward pressure on the employment rate, and Wall Street is bracing for the largest downsizing since 2008. But this is music to Jerome Powell’s ears – because wage gains are slowing and this would mean that people have less discretionary income to spend, and if they spend less, inflation drops. The numbers are bearing this out as well – retail sales fell in December (the busiest shopping time of the year) and wholesale prices dropped by 0.5%.

So, it’s bad news that people are losing their jobs. But a weaker labor market leads to lesser spending and lower inflation, so that’s good news…?

There’s another camp that thinks that the job is not done yet. The Fed is showing signs of slowing down, pausing, or even reversing rate hikes – and experts like Larry Summers think that stopping now could lead to a 1970s-style stagflation scenario. This is despite us seeing the largest interest rates in almost 20 years! So, how has the Fed’s plan fared so far?

Tough task

I don’t envy Jerome Powell for his mission to bring down inflation rates while avoiding a recession – I had written about how the Fed is walking a tightrope like Kobayashi Maru from Star Trek – but despite that, the Fed doesn’t have a great track record of being accurate.

At the start of 2022, the target Federal Fund Rate was 1.9%.

In April, that was moved to 2.75%.

In June, the target was set as 3.5%.

In August, it moved to 4%.

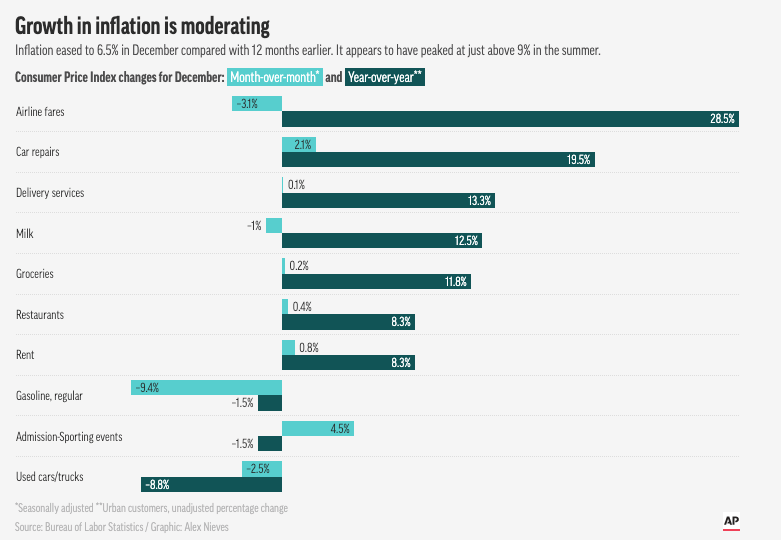

And now, the supposed target is 5%. But what’s different about this time is that for the first time, the rate hikes actually seem to be working. For the last 6 months, inflation has been steadily declining from its peak of more than 9% in June of 2022, to 6.5% now. That’s still high, but it’s gradually trending downwards.

Where do you think the Federal Funds rate will stabilize? Why? Let me know in the comments.

In fact, the most recent consumer spending report showed a decline of 0.2%, month-over-month, while, personal savings increased from 2.9% to 3.4%, during a month when people historically spend more money than usual. This is giving the Fed even more reason to believe that the economy is indeed cooling down.

How does that impact the market?

Cause and effect

The stock market is hungry for any optimistic news right now, but it’s as susceptible to disappointments. The 25 basis point hike had been priced into the market for the last few weeks, and there’s been no surprise with slowing inflation. The surprise was that jobs data showed that non-farm payrolls exceeded expectations and expert estimates were wildly off, causing the market to dip again.

The real question is: When will the rate hikes stop entirely? We don’t have any confirmed direction as of now, but 80% of traders are pricing in one more 25 bp rate hike on March 22nd, and then there’s going to be a pause while they wait and watch to gauge where it’s going to go. As long as the job market is still strong, the Fed is going to be wary of calling the top in terms of interest rates, and with every move of theirs being watched closely, they can’t give us any direct confirmation of their plans too far in advance.

As of now, the expectation is a peak Federal Funds rate of 4.75-5%, but hey, that figure has been revised multiple times over the last two years! The only difference is that consumer estimates of near-term inflation have also fallen to their lowest level in two years, at 3.9% for the next year – so this time might be different.

Homes

The other sector impacted by rate hikes is real estate. But this one isn’t as straightforward as stocks. The country has been seeing a downward trajectory for real estate over the last few months, with luxury home sales in San Francisco crashing by 70% over the last year and total housing inventory falling below 1 million units. But it isn’t uniform throughout the country. Minneapolis, Oklahoma City, Phoenix, and Houston saw the largest decreases nationally, while Salt Lake City, Raleigh, Indianapolis, and Cleveland saw the largest increases.

It’s a bit of a deadlock – would-be sellers are steering clear, and buyers don’t want to get something that they can’t afford or will regret a few months down the line once rates ease up. Once rates stabilize, a new normal will start appearing once more. But the best indicator to keep track of whether the housing market is stabilizing is not to look at sales but rather at the Pending Home Sale Index which looks at current for-sale contracts rather than what it was like last month. In those terms, there was actually a slight increase in December!

What to watch out for

It’s hard to predict what current events mean for the future. But keeping track of the important factors will give you a better pulse on the market.

First, the labor market is going to play an important role. The key mission of the Fed right now is to fight inflation and till wage growth normalizes, the Fed will not ease up soon. While it is shocking to see just how many jobs have been cut in the last few months, so many companies went on a hiring spree in the last few years that even after the cuts, it leaves them with more workers than prior to the pandemic. This might just be a time of scaling back on those decisions and cutting costs.

Another factor to watch out for is that China has just reopened after a long time – Supply chain constraints should smooth out, demand should rise, and international trade should also bolster the economy. But it could also drive excess growth and inflation as the demand for oil, materials, and goods rises. In fact, the president of the Swiss-Chinese Chamber of Congress said: “Chinese energy and raw material needs will compete with the European needs and the global needs, so I see inflation relaxation right now, [but] we will see more pressure on inflation in Q3.” So that could put some pressure on the Fed…

And finally, there’s the fact that we don’t really know if we have a grasp on how inflation works. While the reduction in inflation might be in response to the Fed’s rate hikes, Michael Burry posted that this sort of increase and decrease in inflation rates has been cyclical ever since the 1940s as good times and bad times alternate, and that the Fed really can’t take credit for it.

Overall, the next few months could prove to be a turning point in the battle against inflation with the worst already behind us, and the most important thing to watch out for is how the labor market reacts. In fact, the Fed might have acted proactively and done the hard job, taking us in the right direction, while Europe, Canada and especially the UK are just now beginning to deal with the specter of inflation even as they scale back their own rate hikes.

What about your own funds? While the stock market and real estate market are stuck in uncertainty, the money market is turning out to be a sweet alternative with cash inflows being higher than ever as yields surpass 4%. With a risk-free premium like that, cash might really be a good alternative to park some funds in, with investors like Ray Dalio even saying that “Cash is no longer trash”. Might as well check out a money market account instead of letting your money sit idle in a savings account!

Stay safe, stay invested and I will see you next week – Graham Stephan.

A lot of effort and research went into making this article, so if you found it insightful, please help me out by clicking the like button and sharing this article.

Thanks for the news letter. The only thing I can add to the conversation is on the topic of logistics. I deal with truckloads and container loads domestically and internationally. And know that china is open and has been working hard to "catch up" with demand, along with demand slowing in the US, the rates to get good in from other countries has eased considerably. We had clients that were paying as high as $28,000 to move a container from Shanghai to Utah. That is insane, as just a couple years before it was as low as $4000-5000. I know everything is connected, but the demand from covid and the shortages in containers and freighter ships, in my mind, really seemed to be a huge factor. So I worry about the fed going to crazy on rate hikes, as I feel that the with shipping rates going almost back to normal we will see inflation slow down since businesses arent paying 5x for products anymore.

Really appreciate these Newsletters Graham! Some of the stories I've already heard, but they are all interesting nonetheless.