How to save for a home: Part 2

Debt, mortgages, and what you can afford

Welcome to the premium edition of Graham’s newsletter! These courses are just one of the perks you will get as part of being a paid subscriber.

Let me know what you think about the course in the comments below, and what other topics you would like me to cover.

This is a longer article than usual. Click here to read it on Substack and bookmark it.

In Part 1 of the course, we covered the reasons for buying a home as opposed to renting, and why it could probably be a better decision over the long term. Depending on where you are in life and what the next ten years of your life look like, maybe you’ve made the decision to start saving up for a home. But housing is probably the biggest line item on your budget and a home will be the biggest expense out of your pocket for a long time – that’s one of the reasons that a lot of households take on debt to become first-time homebuyers.

According to Ramsey Solutions, mortgages account for 70% of all American debt, and over 42% of Americans (more than 51 million people) have a mortgage. The average mortgage debt is more than $200,000. The total mortgage debt in the US is more than $10.44 Trillion! A mortgage is a commitment for 15 to 30 years of your life. It’s something that will have an impact on your monthly spending, financial planning, and career choices for decades. And yet, owning a mortgage is not just about lacking the cash to buy a house – I could have the money to buy a property with cash down, and I still wouldn’t do it. That’s because a mortgage lets you use the future value of money.

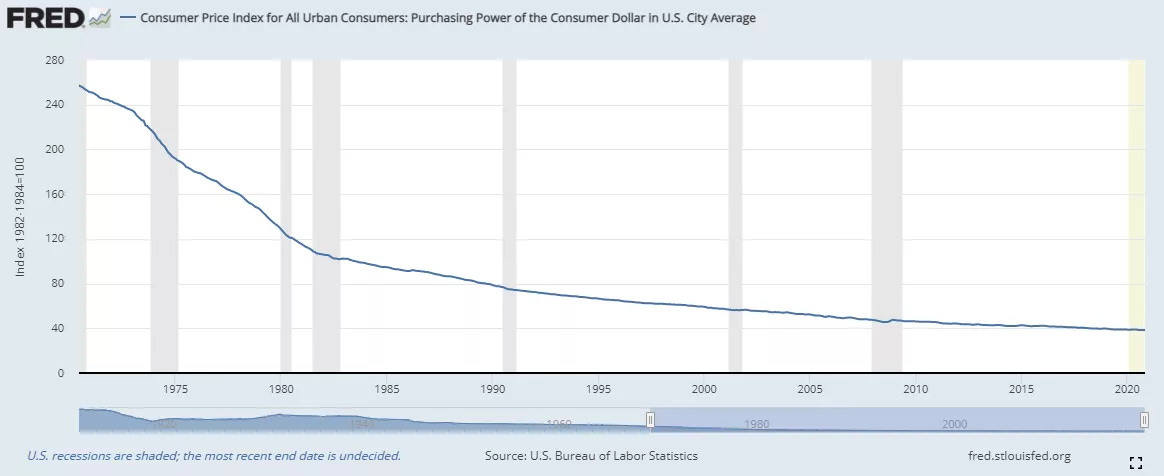

The decaying dollar

If you’ve ever invested in a stock, have you wondered how the market decides on the stock’s price? How do people decide if a stock is “overvalued” or “undervalued”? The price of a stock is supposed to be (roughly) correlated with its value – and that is calculated by estimating how much one dollar invested in the company today is likely to earn in the coming years. But while calculating this, the earnings ten years into the future are always given less weightage compared to say next year. Why? That’s because money loses value with time.

You can run a quick thought experiment to understand the time value of money: If someone were to offer you $1 Million right away vs $2 Million after a year, which one would you take? Most people choose the $1 Million, despite the fact that the $2 Million is the “better” choice. There isn’t even any reliable way to double the $1 Million in a year, yet people choose the quicker option because of the uncertainty associated with the future.

And that’s not the only reason. If you’ve been following the news, you know that there is something very real corroding the value of your money: Inflation. Right now, a dollar is worth less than half of what it was worth thirty years ago. Cash decays with time. The good news is that you can take advantage of this – and get paid for doing so.

Two types of debt

Debt seems like our biggest national problem – Consumer debt recently crossed $16.9 Trillion and 18.3 million Americans were behind on their credit card payments in 2022. But clubbing together all kinds of debt does not give the full picture. Debt, like any other technology, is neutral. The way debt is used decides the impact it has on your life. Consumer debt and debt taken for investment are completely different. The first has the potential to turn addictive and feed off your need for instant gratification. The second can be a powerful tool to build wealth.

The thumb rule for taking on debt is as follows:

If holding on to debt does not make you more money, then avoid it. But if it does make you money, then hold on to it sometimes.

If buying something does not make you more money, buy it outright. But if it does make you money, then finance it sometimes.

The question still remains: Why take on debt, and when? Here’s a thought experiment for you – If I gave you a loan of $100,000 for 10 years without charging interest, would you take it? Obviously, yes – because you could keep the money in a savings or money market account and profit off it without any risk. If I charge you an interest rate up to 3%, it might still be worth it, because you could invest the money in the stock market and have a decent chance of positive returns. Leverage could be a useful tool if the investment is relatively safe, and you can profit off the difference between the interest rate and the investment appreciation. But if the interest rate exceeds 7 to 8%, it gets tricky. There are very few investments that can safely guarantee that level of return without risk, so it would be speculation at that point.

But here’s where taking a mortgage has a special place: The housing market has appreciated in value by 5 to 7% a year historically (though it takes at least 7 years to break even on transaction costs, and market conditions can vary depending on the year). By taking a loan to buy a house and locking in a mortgage at a reasonable rate, you get see your investment appreciate and you profit off the difference between the interest rate and the appreciation.

One argument against this could be that a “home” is technically not an investment as you might never sell it, or you would only upgrade and not downgrade. But as we discussed in the previous part, housing is an inevitable cost, and even considering the mortgage interest and other expenses, buying a house generally overtakes renting in the long term. There are a few other reasons in favor of a mortgage:

We saw above that the dollar is decaying due to inflation. By buying a house on a loan, you are locking in a house at today’s dollar value and paying for it with the money of the future. Considering the dollar’s real value has dropped by more than half, your mortgage payments could be worth 50% lesser in real terms 30 years down the line.

The government encourages people to buy real estate by giving you tax write-offs on your mortgage. This reduces the effective interest on your mortgage further.

You stabilize the cost of your housing by taking on a mortgage – you know exactly how much it will cost 15 to 30 years into the future, and that lets you plan ahead.

Now that we’ve made a case for taking a mortgage, what are the options out there, and how would you choose one?